[ad_1]

Development within the common pharmacy college debt has accelerated vastly lately. Now, you’re uncommon should you graduate with out taking up six-figure pharmacist college debt to finance your schooling. Based mostly on the latest 2020 nationwide survey from the American Association of Colleges of Pharmacy, virtually 85% of graduating college students borrowed to pay for his or her Physician of Pharmacy (Pharm.D.) diploma.

Fortunately, pharmacists even have a few of the finest instruments at their disposal of any occupation to pay again their scholar loans. We’ve saved our common pharmacist consumer a projected $55,769 on their common scholar mortgage debt steadiness of $217,542. Right here is my prescription to treatment pharmacy college debt.

Work out your debt-to-income ratio

A debt-to-income ratio is a statistic I exploit in my scholar mortgage consulting enterprise to determine what choices a consumer may need to pay again their pharmacy school debt. To calculate it, you merely take the overall quantity of scholar debt and divide it by the consumer’s revenue. For instance, let’s say Sue had $150,000 of pharmacy college debt and an revenue of $115,000 as a retail pharmacist at CVS. Her debt-to-income ratio could be $150,000/$115,000 = 1.3.

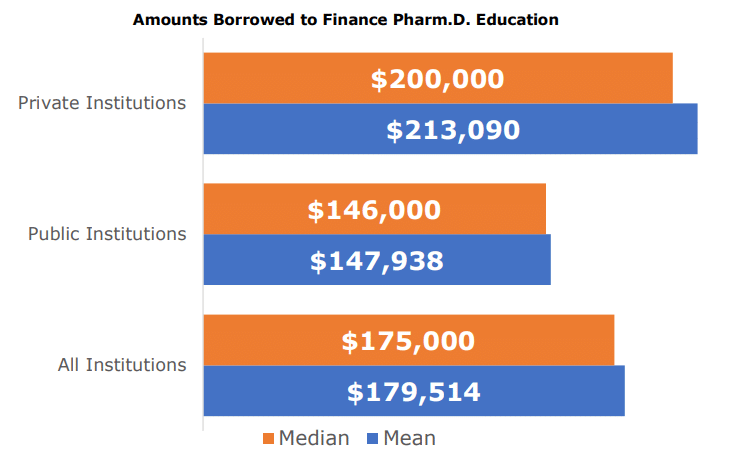

Pharmacy college debt is very variable between people. Public universities produce far decrease complete prices than personal universities. Right here’s a have a look at the pharmacy college debt profile for the category of 2020:

Median Pharmacy College Debt for the Class of 2020

Supply: 2020 AACP Graduating Scholar Survey

I haven’t checked out schooling statistics displaying the whole distribution of pharmacy college debt. However I might guess you’d see two huge clusters of oldsters relying on the place they went to highschool. The primary group would come with graduates from public establishments who would have $50,000 to $150,000 in loans. The second group could be the personal college graduates who owed between $150,000 to $300,000 in scholar loans.

The very best pharmacy college debt I’ve seen in a consumer seek the advice of was round $412,000. The everyday debt hundreds for pharmacy college graduates I’ve seen since I based Scholar Mortgage Planner in 2016 have continued to develop at an alarming charge. In reality, I now get advertisements served to me on many web sites from on-line distance-learning pharmacy applications that cost tens of 1000’s per 12 months in tuition. Many nonprofit colleges within the pharmacy house are responding to the declining applicant pool with aggressive advertising strategies.

Pharmacist beginning salaries are a bit extra predictable — if you may get one

The average pharmacist salary is $102,396 for these simply beginning out. Most people begin off making between $90,000 to $110,000, relying on in the event that they’re in a retail or hospital setting. Clearly, should you do a residency, the pay is far decrease.

There’s a troubling pattern growing the place employers will solely give part-time hours to pharmacists due to labor surplus in giant metropolitan areas the place pharmacists need to dwell. I hear tales of pharmacists in CVS- and Walgreens-type shops being required to work by lunch. While you’re grateful to have a job, it’s rather more troublesome to push again towards that form of expectation.

Whereas some employers pay higher salaries than others, pharmacists general have a comparatively tight band of potential compensation outcomes after commencement in comparison with different skilled diploma applications (should you get full-time hours). This works to pharmacists’ profit when managing federal and personal scholar loans. I’ve by no means seen a debt-to-income ratio above 5 for a full-time pharmacist incomes a non-resident wage. Sadly, I see this occur on a regular basis in different professions.

The commonest debt-to-income ratios make pharmacy scholar debt manageable

Most pharmacists will graduate with pharmacy college debt of round $50,000 to $250,000. And most pharmacists’ incomes will probably be between $80,000 and $120,000, until they do a residency program. Most graduates may have debt-to-income ratios of 1.5 to 2.5.

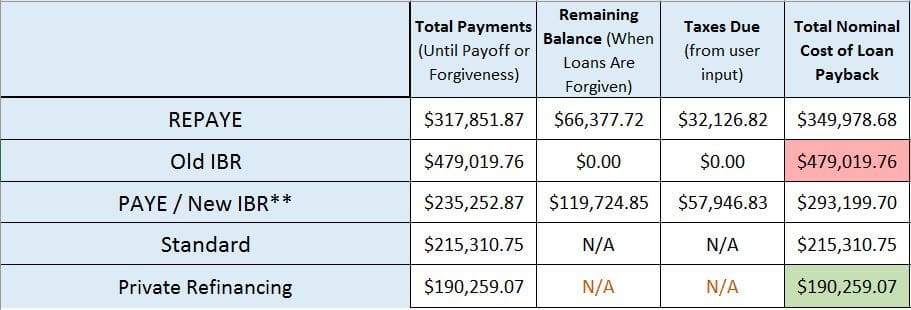

Some pharmacists will need to use personal sector mortgage forgiveness

Let’s run a simulation to see what I’m speaking about. Assume that Kim graduated in 2018 with a pharmacy college debt load of $150,000 at a 7% rate of interest. She makes a beginning wage of $105,000 working at a retail pharmacy.

For those who’re a pharmacist within the personal sector and utilizing one of many income-driven reimbursement choices for federal scholar loans, guarantee that’s the fitting path. The whole price in your schooling will doubtless be increased on one in all these applications should you owe lower than 1.5 instances your revenue. One cause is that pharmacist incomes are excessive sufficient that the month-to-month income-based funds aren’t low-cost. The opposite cause is that after years of excessive funds, you’ll must pay a tax penalty on the leftover pharmacy college debt steadiness.

That mentioned, should you went to personal pharmacy college and need to work in a saturated space, income-driven scholar mortgage forgiveness over 20 to 25 years really may make plenty of sense. It depends upon what the numbers present on a student loan spreadsheet.

Most personal sector pharmacists ought to refinance their debt with a non-public lender

Observe that the above personal refinancing instance was for a 10-year time period and an rate of interest of 4.5%. In case you have nice credit score, excessive revenue and little debt outdoors of what you borrowed in your schooling, you may get a charge even decrease than that. Thus, the financial savings could be increased.

Whereas I feel it could be well worth the flat payment to double-check whether or not you need to refinance as an alternative of going for mortgage forgiveness, it’s your name. I’ll embrace my referral links here so you may examine what your charge could be by a non-public refinancing firm. They provide each you and me a money bonus, and you could possibly get 1000’s of {dollars} a 12 months in curiosity financial savings.

So many pharmacists do not know they’re giving the federal government free cash by paying again their loans on the usual 10-year plan. Please attain out to me at [email protected] should you fall into this class. There are such a lot of higher choices accessible.

What should you work for a nonprofit employer?

That is one cause why getting a plan in your pharmacy college debt is so helpful. We don’t simply have a look at personal refinancing firms. We do a holistic analysis of your debt profile and attempt to discover each greenback of financial savings we probably can. For pharmacists working at a nonprofit group — similar to youngsters’s hospitals, group well being facilities, and so on. — you may be eligible to have most of your pharmacy college debt forgiven tax-free. For those who work for a nonprofit, then it is advisable to know concerning the Public Service Mortgage Forgiveness Program (PSLF).

PSLF permits for tax-free mortgage forgiveness after 120 month-to-month funds made on a qualifying federal reimbursement plan whereas working for a qualifying nonprofit employer. For those who’re not sure whether or not you qualify, we might help clear that confusion up. You can even see should you’re eligible by submitting the PSLF Employment Certification Form.

The pharmacists who may benefit probably the most from PSLF are those who undergo with a residency and/or fellowship. For those who full this coaching and go to work in a nonprofit hospital setting, you may be capable of pay as little as 20% of the price of your schooling over time. You’ll make regardless of the minimal month-to-month cost is on an income-based program and monitor your progress towards PSLF by submitting the employment kind yearly.

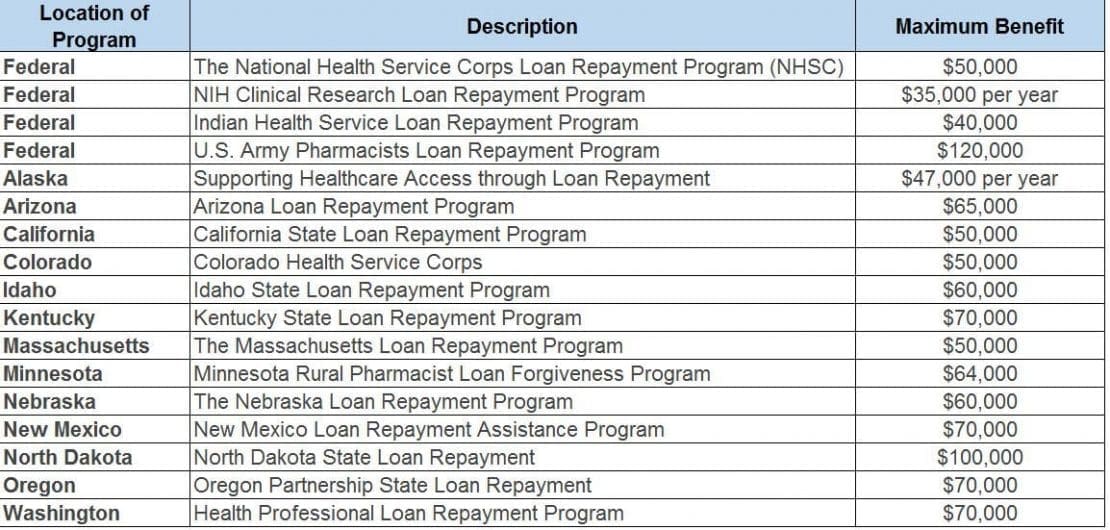

One other necessary useful resource is federal and state pharmacy college debt forgiveness applications. PSLF is the biggest and most extensive ranging. Nonetheless, take a look at this listing over at Credible on the varied applications accessible for pharmacy college debt.

What do I do with my pharmacy college loans throughout a residency or a fellowship?

Pharmacists make plenty of errors with their scholar loans when going into postgraduate coaching. No matter you do, please don’t use forbearance or deferment should you plan on doing a residency or fellowship. The curiosity continues to accrue, and also you’ll lose out on federal mortgage advantages.

For instance, say a brand new Pharm.D. takes a postgraduate 12 months one (PGY-1) place and that she has $200,000 in pharmacy college debt. Assuming all the loans are unsubsidized at a 6% common rate of interest, they’ll accrue $12,000 of curiosity by the tip of their first 12 months. Think about they add on a PGY-2 12 months and a one-year fellowship. In the event that they do the income-based reimbursement paperwork completely and prevents any of the curiosity from capitalizing, they’d add one other $24,000 in curiosity for pharmacy college for a complete of $36,000.

If as an alternative the borrower used the Revised Pay As You Earn (REPAYE) plan, they’d pay about $185 a month on their loans throughout coaching. Along with having this quantity credited towards their complete steadiness, they’d obtain an curiosity subsidy of fifty% of the remaining curiosity not coated by her month-to-month cost.

The curiosity accrual is about $1,000 a month. The federal government would take $1000, subtract $185 and get a the rest of $815. Then, the federal government would pay 50% of that leftover curiosity. In different phrases, Uncle Sam pays about $407.50 a month in curiosity prices. In complete, our new Pharm.D. solely has to cope with $407.50 of curiosity every month as an alternative of $1,000 a month. That’s an enormous profit that almost all pharmacists doing postgraduate coaching have no idea about.

REPAYE just isn’t all the time the fitting reimbursement plan. It depends upon your loved ones measurement, spousal revenue, spousal scholar mortgage burden and money move accessible for scholar mortgage funds. Even so, the worst determination is electing to pay nothing throughout pharmacy residency or fellowship. I assist appropriate these errors throughout pharmacy college debt consults.

Make a plan to sort out your pharmacy college debt and save 1000’s of {dollars}

One among my pals from undergrad went to pharmacy college after faculty. We all the time do a fantasy soccer league yearly with a few of the guys from our faculty church group. I requested him some questions in preparation for writing this text, and he talked about he had some pharmacy college debt.

We took a have a look at his mortgage profile, and he mentioned he labored at a not-for-profit county hospital. I took a have a look at his loans, and he was making funds underneath the usual 10-year reimbursement plan. His rate of interest was north of 6%.

He had made funds for 3 years on this plan. Fortunately, funds made on the usual 10-year reimbursement plan nonetheless depend for PSLF. We switched him to REPAYE. Now his funds will probably be 10% of his discretionary revenue as an alternative of the far increased customary funds. Moreover, after one other seven years of funds, his steadiness will probably be forgiven by the federal government tax-free. I saved him about $100,000 in comparison with the technique he’d been utilizing that may have resulted in full payback.

If he had labored at a CVS or Walgreens, as an alternative, I might have made certain he bought a decrease charge than the lower than 6% he had been paying by personal refinancing. Both approach, he’d been paying 1000’s of {dollars} yearly in pointless scholar mortgage funds.

Have a well-thought-out technique to cope with your pharmacy college debt

Whether or not you study the mortgage guidelines and give you a technique your self or rent Scholar Mortgage Planner to assist for a one-time flat payment, most pharmacists lose out on 1000’s of {dollars} in financial savings on pharmacy college debt. Don’t be one in all them. In case you have ideas on pharmacy college debt, questions on handle it or simply need to vent concerning the excessive price of schooling, hit up the feedback part beneath, and I’ll reply.

Scholar Mortgage Planner might help work out your pharmacy college loans

Our enterprise mannequin helps pharmacists such as you conquer large scholar loans with flat-fee consultations.

The marketing consultant you’re employed with will carry out a holistic mortgage evaluation to see what your finest accessible reimbursement choices are. They’ll simulate what the long run seems to be like, together with plan for a probably huge tax penalty. We additionally have a look at married submitting separate eventualities, whether or not you need to consolidate and if you must fear about making an excessive amount of cash and getting kicked off your income-driven plan.

The worst factor you could possibly do is to disregard your pharmacy college loans, so get a plan, whether or not you employ the information you achieve from our website or determine you desire a skilled to determine it out for you. Take a look at our other articles for pharmacists when you’re at it.

[ad_2]

Source link

{kind=link}