[ad_1]

Right here’s your own home shopping for guidelines

Shopping for a house might be the largest buy most of us will make in our lifetimes. It’s completely pure to have questions and expertise each identified emotion throughout the residence shopping for course of.

There’s a number of work to do, however don’t fear — this residence shopping for guidelines will enable you to roll up your sleeves and get you prepared in your deadline in 10 straightforward steps.

Verify your home buying eligibility. Start here (Nov 27th, 2021)

On this article (Skip to…)

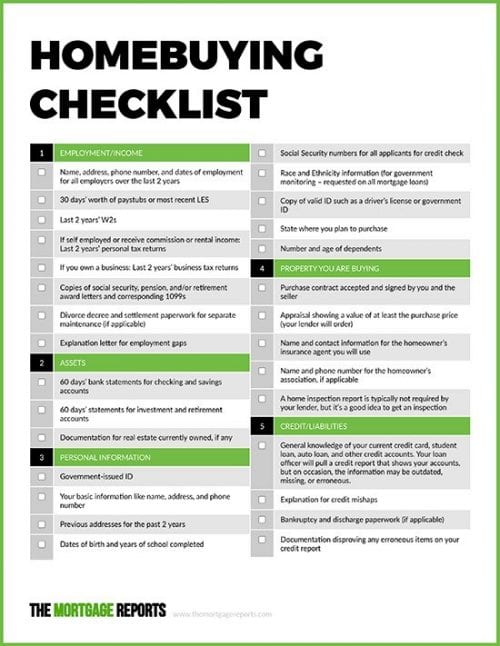

Full residence shopping for guidelines

Use this residence shopping for guidelines as a cheat sheet in your total residence shopping for course of: from gathering your paperwork to making use of for a mortgage and discovering your dream residence. We clarify every stage of the method intimately beneath.

Click on the picture to open a PDF model of the house shopping for guidelines.

1. Work out what you possibly can afford

Homeownership may be among the many greatest monetary selections that you just’ll make. Earlier than you start visiting open homes, ensure you possibly can afford the acquisition worth of your dream residence.

Most residence consumers will want a mortgage to purchase a brand new home, which requires discovering a lender. There’s nothing worse if you’re shopping for a house than having your mortgage software denied. So checking your private funds earlier than you start home looking is a crucial first step.

Use a mortgage calculator

A mortgage affordability calculator might help each first-time residence consumers and seasoned veterans perceive:

- How a lot home you possibly can afford

- Desired mortgage phrases and rates of interest

- Down fee quantity

- Desired month-to-month mortgage funds

- Estimated property taxes

Take a while to think about how your present month-to-month bills examine with the outcomes of your mortgage calculator estimates.

Test you credit score rating

Your credit score is an important factor in qualifying for a mortgage and figuring out the rate of interest on your own home mortgage.

Even you probably have good credit score, double verify your credit score report and contest any errors.

Paying down any high-interest bank card debt, private loans, or scholar loans earlier than making use of for a mortgage may also assist enhance your credit score rating and decrease your debt-to-income ratio.

Verify your mortgage eligibility. Start here (Nov 27th, 2021)

2. Organize the down fee

When you’ve found out how a lot residence you possibly can afford, the following step is figuring out how much of a down payment you’ll want.

The dimensions of your down fee is essentially decided by the kind of mortgage you get. Down funds on typical mortgages start round 3% to five% of the house’s buy worth.

Nevertheless, if you wish to keep away from private mortgage insurance, you’ll want 20% down.

FHA loans require 3.5% down, and a few forms of loans help you purchase a home with no down fee in any respect. Authorities-backed USDA and VA loans allow you to finance 100% of the house worth with no cash down.

Whatever the dimension of your down fee, it’s a good suggestion to place apart slightly additional to cowl closing prices and any repairs that your own home inspection may reveal.

3. Decide on a lender and get pre-approved

Most individuals take their time with the home looking section when shopping for their dream residence. In truth, the common residence shopping for course of within the U.S. takes about 4 months.

Through the purchasing interval, you’ll be taught what’s and isn’t vital to you for a brand new residence in your worth vary, which neighborhoods you favor, and what your deal-breakers are.

Nevertheless, few residence consumers benefit from the mortgage course of as a lot as home purchasing.

The bulk surveyed by the Consumer Financial Protection Bureau (CFPB) solely thought of a single mortgage lender when financing their property. As well as, a major share postpone contacting a lender in any respect till after they discovered the right residence.

Mortgage pre-approval

You actually shouldn’t start purchasing for a home till you understand how a lot home you possibly can afford. And if you would like sellers and their actual property brokers to take you critically, you want a pre-approval letter.

Needless to say pre-approval isn’t the identical as pre-qualification. While you get pre-qualified by a lender, it’s an estimation of what they’ll lend you.

Pre-approval is a extra rigorous examination of your monetary state of affairs, and it lets you already know precisely the mortgage quantity a lender is keen to underwrite.

- You get pre-approved for a house mortgage by making use of to a number of mortgage lenders. Underwriters will doubtless have questions or lists of paperwork they need, and when you adjust to their requests, you get your pre-approval letter

- The CFPB survey discovered that nearly each borrower thought of the rate of interest or mortgage prices as major concerns when purchasing for mortgage lenders. It’s straightforward to request a fist stuffed with quotes on-line, so get them now. Then, you possibly can contact a number of of essentially the most aggressive lenders and consider them personally

- Word the mortgage lenders whose model of working meshes with your individual. If you happen to favor calls and get texts, or in case your mortgage officer is hard-to-find when you may have questions, select somebody who makes you extra snug

Connect with a lender to start your mortgage pre-approval (Nov 27th, 2021)

4. Discover a actual property agent

An actual property agent generally is a big assist when shopping for a house. Not solely can brokers discover properties on the market as quickly as they’re listed, brokers know the housing market in your space and might present distinctive insights that may enable you to discover the right residence.

When discovering an actual property agent, ask family and friends for suggestions, learn on-line evaluations, and be sure you converse with a number of choices earlier than deciding on the agent that’s best for you.

As well as, residence consumers shouldn’t fear about the price of an actual property agent.

Many first-time residence consumers don’t know this, however the vendor virtually at all times pays their very own agent and the client’s agent. So you possibly can normally get assist from a purchaser’s agent freed from cost.

5. Search for your dream residence

As soon as you already know precisely how a lot you possibly can spend, and that you just’ll be capable to purchase any property that meets your lender’s requirements, the enjoyable begins. Buy groceries. That is the enjoyable a part of the house shopping for guidelines, too.

This guidelines beneath was initially created by HUD, and it does an excellent job of reminding you to concentrate to the identical particulars for every home you see. As you full the kinds and see extra homes, you and your agent ought to rapidly be taught what areas and residential varieties are higher matches.

Use one for every home you tour, and match it up with any photos you are taking. Alternatively, there are a number of house-shopping apps that help you combine your notes and pics into on-line recordsdata. For each criterion, observe if the house function is an efficient, common or poor match for you.

Home looking guidelines:

House

- Sq. footage

- Variety of bedrooms

- Variety of baths

- Practicality of ground plan

- Inside partitions situation

- Closet/space for storing

- Basement

- Fire

- Cable TV

- Basement: dampness or odors

- Exterior look, situation

- Garden/yard area

- Fence Patio or deck

- Storage

- Power effectivity

- Screens, storm home windows

- Roof: age and situation

- Gutters and downspouts

Neighborhood

- Look/situation of close by properties/companies

- Site visitors

- Noise stage

- Security

- Safety

- Age mixture of inhabitants

- Variety of kids

- Pet restrictions

- Parking

- Zoning laws

- Neighborhood restrictions/ covenants

- Hearth safety

- Police

- Snow elimination

- Rubbish service

Colleges

- Age/situation

- Status

- High quality of academics

- Achievement take a look at scores

- Play areas

- Curriculum Class dimension

- Busing distance

Comfort

- Grocery store

- Colleges

- Work

- Purchasing

- Baby care

- Hospitals

- Physician/dentist

- Recreation/parks

- Eating places/leisure

- Church/synagogue

- Airport

- Highways

- Public transportation

6. Rent an actual property lawyer (if required)

Hiring an actual property lawyer isn’t at all times a necessity, however some states require an legal professional to characterize you. Your agent or realtor can let you know if one is required.

In case your state does require an actual property legal professional, keep away from selecting the most affordable service you could find. Deal with this course of much like the way you would choose a lender or an agent — get suggestions, learn evaluations, and converse with a number of choices earlier than deciding.

7. Make a suggestion and negotiate

While you’ve discovered the right residence, it’s time to make an offer. Your actual property agent or Realtor will information you thru the method, and in lots of instances, take the lead.

Your supply shall be primarily based on quite a few elements, together with

- How sizzling the actual property market is

- Asking worth

- Whether or not or not there are different provides

- How lengthy the property has been available on the market

The vendor will both settle for, decline, or counter your buy supply. If the vendor declines, you may have the choice to make a counter supply.

Your buy supply will embrace an earnest cash deposit — sometimes between 1% to three% of the acquisition worth — that shall be put into escrow. The earnest cash will stay in escrow till the vendor accepts your supply.

If you happen to get chilly toes concerning the residence and rescind your supply, the earnest cash is forfeited to the vendor. In any other case, will probably be utilized to your down fee and mortgage closing prices.

8. Get last approval in your mortgage

As soon as the vendor has accepted your supply, you’ll start the formal mortgage software course of.

Though you’ve been pre-approved for a mortgage, count on to offer further documentation to your mortgage officer because the underwriting course of progresses.

Paperwork you’ll want for the mortgage software

Mortgage lenders merely wish to just remember to can afford your own home mortgage and that you’re more likely to repay it as agreed. They have to adjust to authorities laws requiring them to show that they’ve evaluated you lawfully.

Employment and earnings verification

- Pay stubs overlaying one month or most up-to-date Go away and Earnings Assertion from the navy

- Final two years’ W2s

- If self-employed, a commissioned worker (25% p.c or increased), an worker with unreimbursed enterprise bills or actual property earnings, you’ll provide at the least your final two tax returns. For earnings that’s extremely variable or uncommon, you might want further years

- If you happen to personal a enterprise, you want at the least two years’ enterprise tax returns

- Proof of receipt for Social Safety, pension, public help (if utilizing to qualify) or different earnings. This normally means an award letter, verify stub, or direct deposit

- Divorce decree and settlement paperwork for separate upkeep (if relevant)

- Rationalization letter for employment gaps

Belongings

- Two months’ financial institution statements for checking and financial savings accounts

- Two months’ statements for funding and retirement accounts

- Data for actual property already owned (use, earnings, if it’s available on the market, estimated worth, mortgages)

Private data

- Authorities-issued ID

- Earlier addresses for the previous two years

- Dates of beginning and years of faculty accomplished

- Social Safety numbers for all candidates

- Race and Ethnicity data (for presidency monitoring – requested on all mortgage loans)

- State and county wherein you intend to buy

- Quantity and age of any dependents

Property particulars

- Buy contract accepted and signed by you and the vendor (you probably have one picked out)

- Title and speak to data for the home-owner’s insurance coverage agent you’ll use

- Title and telephone quantity for the home-owner’s affiliation, if relevant

Credit score and liabilities

- Your mortgage officer will verify your credit score rating by pulling a credit score report that exhibits your accounts, however every now and then, the knowledge could also be outdated, lacking, or faulty. That data is integrated into your mortgage software, and also you’re chargeable for its evaluate and affirmation

- Rationalization for credit score rating mishaps

- Divorce decree and settlement paperwork for little one or spousal assist bills (if relevant)

- Chapter and discharge paperwork (if relevant)

- Documentation disproving any faulty gadgets in your credit score report

For a full breakdown of all paperwork, obtain our home buying checklist.

Don’t neglect householders insurance coverage

Your lender could require you to get householders insurance coverage as a part of the approval course of. Even when they don’t, it’s an excellent time to get quotes out of your insurance coverage firm, or store your householders insurance coverage coverage round with a couple of suppliers to get one of the best deal on protection.

9. Schedule a house inspection and appraisal

After you’ve reached an settlement with the vendor on the acquisition worth of the house, the following step is scheduling the house inspection and appraisal.

The house inspection will make sure the property is as much as code and that the inspiration and roof are structurally sound. Your house inspector will take a look at methods like plumbing and electrical and offer you an in depth report with the house inspection outcomes.

Along with a fundamental inspection, some residence consumers additionally take a look at for the presence of radon and mildew.

Whereas a house inspection isn’t required, it’s extremely beneficial and helps you keep away from any hidden issues that may have an effect on your own home worth in years to come back.

A house appraisal, then again, shall be required by your mortgage lender to verify that the house worth is according to the mortgage quantity.

Your appraiser will decide the market worth of the house by property values within the neighborhood and evaluating the house’s common situation.

10. Shut in your new residence

Congratulations, the closing course of is the ultimate step to homeownership! Your actual property agent and mortgage officer will care for many of the work, however you’ll have a couple of last duties — together with signing mountains of paperwork.

Right here’s a fast breakdown of what you possibly can expect on your closing date:

- Your lender supplies the closing disclosure at the least three days earlier than closing

- Remaining walk-through of the property on or earlier than closing

- You’ll deliver an authorized verify or scheduled wire switch to cowl your down fee and shutting prices

- You’ll additionally want proof of house owners insurance coverage

- Identification

Are you able to get began?

When you’ve studied the house shopping for guidelines, you’re able to get the ball rolling.

Begin with an outline of immediately’s mortgage charges to search out out what you possibly can afford.

[ad_2]

Source link

{kind=link}