[ad_1]

Will the housing market enhance in 2022?

The 2021 housing market was a double-edged sword for dwelling customers.

Low charges and elevated flexibility with working from dwelling put many first-time patrons on the map. However restricted stock and skyrocketing costs made housing tougher to come back by.

However issues might quickly stage out to a extra ‘normalized’ market, in accordance with the consultants.

Though charges are rising and residential provide stays low, competitors may begin to taper off and value beneficial properties might average.

Briefly, 2022 ought to be a greater market for a lot of patrons.

Verify your home buying eligibility. Start here (Oct 19th, 2021)

On this article (Skip to…)

Housing market predictions for 2022: Overview

We spoke with seven actual property and mortgage consultants to get their housing market predictions for 2022.

Most agree that the market will stay sizzling, as it would take a very long time to regain stock. However they agree that competitors and costs ought to average considerably.

Housing demand and demographics

Ask Rick Sharga, govt vice chairman for RealtyTrac, and he’ll inform you that the housing market ought to proceed its sturdy efficiency by way of 2022.

“Demand will proceed to be pushed by low mortgage charges and demographics. Take into account that the biggest cohort of millennials is approaching prime age for first-time homeownership,” he says.

“The pandemic has additionally contributed to the current increase in dwelling shopping for, partially because of the skill many staff now need to do business from home and to well being issues, which inspires metropolis dwellers — largely renters — to search for extra spacious residences in areas with decrease inhabitants density.”

Potential for enchancment

Paul Buege, president and COO of Inlanta Mortgage, additionally thinks the market will stay sturdy. However he foresees costs and demand cooling off no less than a bit in 2022.

“Constructive indicators are hinting to a extra favorable housing market in 2022. The heated tempo of gross sales is starting to point out indicators of moderation, and that is serving to to extend the variety of houses for buy,” says Buege.

“With extra houses available on the market, costs ought to start to average. This means that the steadiness between sellers and patrons will shift towards a extra normalized market subsequent 12 months.”

Look out for rising charges

Chuck Biskobing, an actual property lawyer at Cook dinner & James, agrees that dwelling value beneficial properties ought to begin to stage off subsequent 12 months. However he additionally cautions that increased rates of interest might lead to much less shopping for energy for potential purchasers.

“If inflation doesn’t abate, the Fed and market could push charges increased extra shortly than anticipated, which may take a toll on affordability,” Biskobing explains.

If your private home shopping for plans hinge on in the present day’s low charges, that could be cause sufficient to proceed your search now slightly than ready till 2022.

Verify your home buying budget at today’s rates. Start here (Oct 19th, 2021)

House value predictions for 2022

House costs have been on a record-setting rise in 2021.

In response to CoreLogic, costs elevated by greater than 18% between August 2020 and August 2021.

This was “the biggest annual achieve in dwelling costs within the 45-year historical past of the CoreLogic House Value Index” — and it got here proper on the heels of enormous year-over-year will increase in July and June.

Sadly, dwelling values aren’t prone to cease rising or begin falling any time quickly.

However the excellent news is, dwelling costs beneficial properties may decelerate, which might take a few of the stress off potential patrons.

House value beneficial properties might gradual to round 5%

“I count on dwelling costs to proceed to rise, primarily attributable to restricted provide. Nonetheless, value will increase will average subsequent 12 months to accommodate family affordability,” says Albert Lord, founder and CEO of Lexerd Capital Administration.

He notes that the nationwide median itemizing value in August was $380,000 — 16% increased than in 2020. “For 2022, I predict a rise in dwelling costs by 5%,” says Lord.

Curiously, one skilled believes dwelling costs are solely simply catching up from the earlier decade.

“They’re simply now solely attending to the place they need to be on a 20-year arc,” believes John Hunt, founder and principal of MarketNsight.

“The increase and bust of the Nice Recession held costs down, particularly for resale, for a decade. Take into account that the typical value appreciation over the past 20 years is 4.5%. We can be heading again to that standard in 2022 and past.”

Excessive demand means value traits gained’t reverse

Nik Shah, CEO of House.LLC, anticipates dwelling value appreciation cooling barely subsequent 12 months.

“Nonetheless, we count on costs to proceed growing in 2022, fueled by millennial demand, low rates of interest, and low housing stock ranges,” Shah continues.

Sharga factors out that the work-from-home motion could proceed to allow folks to maneuver from costlier markets to smaller, inexpensive areas, which might dramatically inflate costs in a few of the smaller markets.

“Then again, we’d see some value corrections in just a few of the higher-price markets just like the Bay Space in California,” he provides.

House stock predictions for 2022

With the true property market drifting towards a extra normalized tempo, many trade consultants envision the variety of present houses on the market growing subsequent 12 months, particularly as present householders look to maneuver.

“Provide may even proceed to be supported by the rising stock of accessible new houses for buy coming on-line subsequent 12 months,” says explains Buege. He expects some traders to begin promoting off rental properties, too, to benefit from in the present day’s excessive costs.

Ralph DiBugnara, founding father of House Certified, agrees that offer ought to enhance considerably in 2022. However he warns that the dearth of stock of houses on the market will proceed to be an issue.

Housing stock might enhance a bit in 2022, however will probably stay an issue for years to come back.

“In response to Fannie Mae, we are going to nonetheless see an virtually 50 % scarcity of houses out there to satisfy a standard demand of patrons,” he says. “I consider it would take two to 3 years for the stock scarcity to normalize once more.”

And don’t neglect that offer chains stay disrupted from COVID, and employee shortages proceed to current challenges to dwelling builders.

“I consider we can be in a state of housing scarcity for one more decade,” says Hunt. “We nonetheless have the issue of metropolis and county governments not allowing higher-density product, which permits for reasonably priced and workforce housing.

“Additionally,” he provides, “boomers who ought to be promoting their houses and including to stock will not be transferring — primarily as a result of they’ve nowhere to go attributable to lack of stock. It’s a vicious cycle that I count on will final for a really very long time.”

Mortgage price predictions for 2022

In all probability essentially the most urgent query posed to the professionals is a predictable one: The place will charges for the benchmark 30-year fixed-rate mortgage land subsequent 12 months?

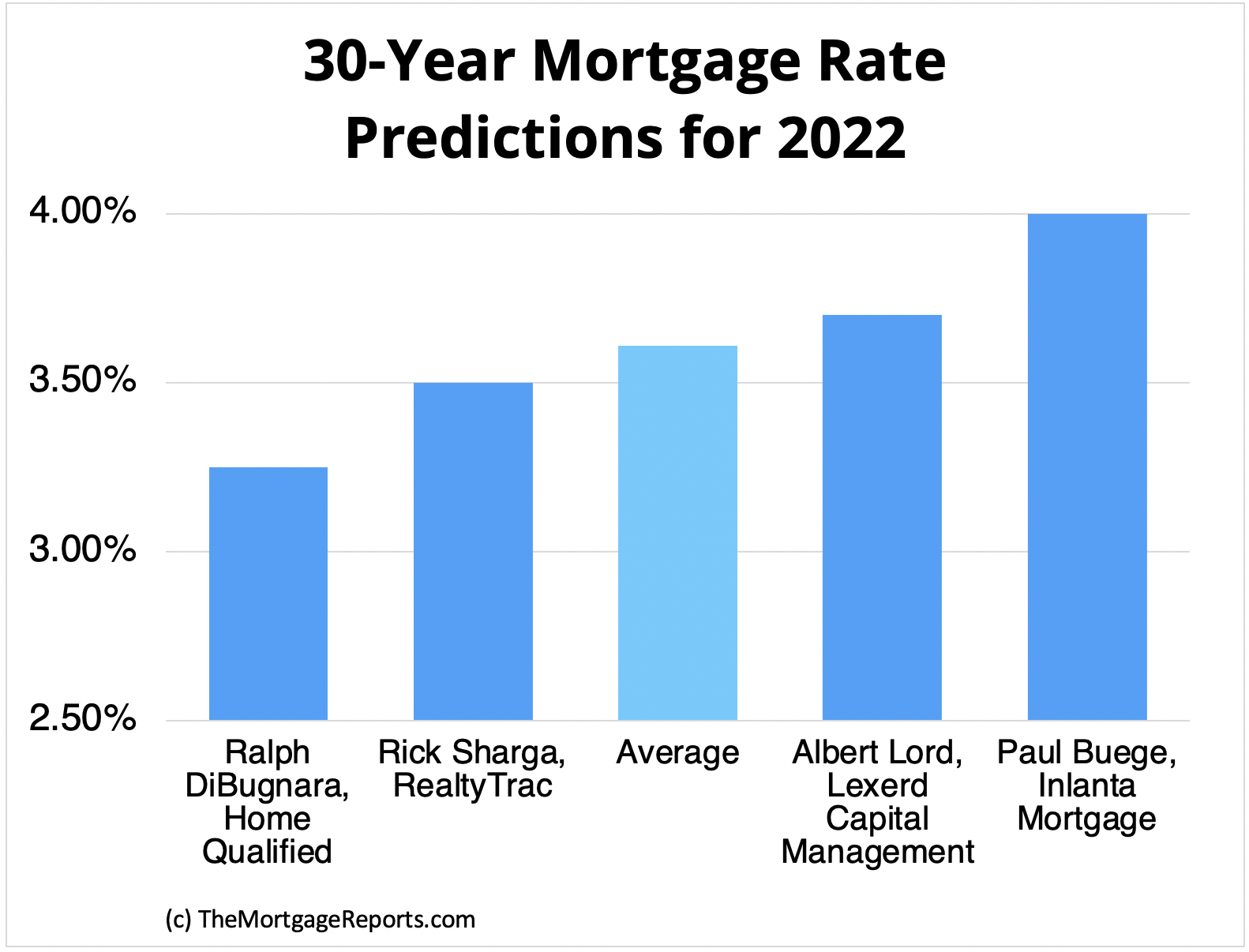

DiBugnara believes we will count on comparatively low charges to proceed, no less than for some time.

“The nationwide common rate of interest will probably keep someplace round 3.25% for 2022. There’s not sufficient stability out there to maintain a big enhance in rates of interest,” he says.

Rick Sharga of RealtyTrac, in contrast, is forecasting a mean price of three.5% by mid-year 2022 and an end-of-year price of three.75%.

“Mortgage rates of interest are prone to go up for a number of causes, together with continued financial progress and better yields on U.S. 10-year treasuries, which frequently instantly affect rates of interest on 30-year fixed-rate loans,” Sharga says.

“One other vital issue is the Federal Reserve’s current announcement that it could start to taper its purchases of $40 billion a month in mortgage-related securities, which alone ought to give mortgage charges a bump.”

Lord subscribes to that principle.

“Based mostly on my financial evaluation, I predict a modest price enhance to three.7% in 2022. Charges can not enhance drastically, given the present fiscal atmosphere,” provides Lord.

Others wouldn’t be stunned if charges creep even increased than these estimates.

“Search for 30-year fastened charges to maneuver after which maintain regular in a price vary of three.75% to 4.25% by late 2022. Even with that bounce, understand that mortgage rates of interest will stay at traditionally favorable ranges,” says Buege.

Find your lowest mortgage rate. Start here (Oct 19th, 2021)

Will the housing market crash in 2022?

There’s one factor the consultants all agree on: Don’t count on an actual property market crash, just like what occurred in 2008, anytime subsequent 12 months.

“The economic system has made a exceptional restoration from the pandemic-driven recession and can probably have regained just about 100% of the roles misplaced in the course of the downturn by the top of 2022,” says Sharga.

Plus, lots of the forces behind the 2008 crash merely don’t exist proper now.

“House value appreciation is being pushed by provide and demand — not hypothesis or unhealthy lending practices like years in the past — and family formation continues to extend as Gen Y and Gen Z come of age,” he explains.

DiBugnara reminds us that free credit score and earnings pointers to qualify for a mortgage in addition to an abundance of dwelling stock considerably contributed to the final housing market crash 13 years in the past.

“At this time, we have now a lot stricter lending guidelines and pointers for buying a house together with a scarcity of houses on the market,” says DiBugnara. “Resulting from lingering excessive demand and continued lack of houses to buy, it could be very laborious for a market crash to materialize.”

Biskobing concurs.

“I can think about a state of affairs the place the Fed is pressured to lift rates of interest sooner than anticipated, however even when they do I don’t count on a market crash,” he says.

Must you purchase a house now or wait?

In-depth predictions are all effectively and good, however the final query many need a solution to is straightforward: Ought to I buy a house now or wait issues out?

“That relies on a purchaser’s distinctive circumstances,” Lord says.

Who ought to wait till 2022 to purchase?

It may be greatest to attend in case your funds aren’t in the most effective place to afford a mortgage cost or safe a low rate of interest.

“You might wish to take into account renting till you’ll be able to fulfill the homebuying rule of thumb of 30/30/3,” continues Lord. This rule dictates that:

- Your month-to-month mortgage funds mustn’t exceed greater than 30 % of your family’s gross earnings

- You must get hold of a 30-year mortgage

- You must intention for round a 3% fastened rate of interest

For some folks, although, now is a superb time to purchase regardless of present challenges out there.

Who can buy a house now?

If you’re looking for to lift a household and/or keep put with out transferring over the subsequent 5 to 10 years, now is a superb time to assert a house and lock in a most well-liked mortgage price, insists Sharga.

“For many households, homeownership is an efficient long-term technique that ends in pressured financial savings and the creation of intergenerational wealth. It additionally gives a secure atmosphere for a household,” he explains.

“However homeownership comes with a variety of monetary duty. And there’s additionally some potential short-term threat, as dwelling values can fluctuate, generally taking place. I usually inform potential patrons to maneuver as quick as they will, however solely after they’re positive they’re prepared from a monetary perspective.”

Deal with your self slightly than timing the market

Above all, keep away from making an attempt to completely time the market.

“Individuals spend an excessive amount of effort in making an attempt to sport the housing system,” Biskobing says. “However guessing at market strikes, and particularly rate of interest strikes, is a idiot’s errand.”

He continues, “Shopping for a home ought to be a sensible determination based mostly on the place one is of their life financially and on their life path. Low charges argue for purchasing now in case you can afford it and have a secure job with wholesome earnings.”

Unsure whether or not you should purchase? A great subsequent step is to attach with a mortgage lender.

Your mortgage adviser can stroll you thru your mortgage choices, rates of interest, and residential shopping for funds. Then you can also make an knowledgeable determination about whether or not to purchase now or wait.

[ad_2]

Source link

{kind=link}