[ad_1]

Earnings-driven compensation is a big advantage of the federal pupil mortgage system. Sadly, it’s complicated to know which plan to decide on. It may be much more complicated you probably have drastic revenue modifications throughout your profession.

Once you graduate, your federal loans are placed on the 10-year Commonplace Compensation Plan. This plan knocks out your loans within the shortest potential time. The issue is, should you’ve borrowed something bigger than a couple of greenback, your month-to-month cost quantity tends to be very excessive.

So beginning within the early Nineteen Nineties, the Division of Training launched income-driven repayment (IDR) plans, the primary of which was Earnings-Contingent Compensation or ICR, which wasn’t the best. In the present day, there are 4 IDR plans to select from, together with Pay As You Earn (PAYE), Revised Pay As You Earn (REPAYE), Earnings-Primarily based Compensation (IBR), and ICR.

We’ll stroll you thru some actual examples of how to decide on the fitting compensation plan. You’ll additionally learn the way your cost will change as your revenue modifications utilizing Pupil Mortgage Planner’s free repayment calculator. It’s one of the best round. We’ll begin with some fundamentals you could know earlier than you enter numbers into the calculator.

Your revenue

Some debtors consider “revenue” as their complete wage, whereas some debtors consider “revenue” as what hits their checking account. On the planet of pupil loans, there’s just one definition of revenue that issues — your Adjusted Gross Income or AGI.

It is a particular quantity in your tax return. In truth, should you dig out your 2020 tax return, it’s line 11 in your Kind 1040.

The AGI calculation is mostly your gross (or complete) wage minus:

- Pre-tax 401(okay), 403(b), or 457 retirement financial savings (your portion, not your employer match).

- Pre-tax or conventional IRA contributions (Roth IRA contributions don’t depend).

- Well being financial savings account.

How funds are calculated for IDR plans

How are income-based compensation quantities calculated? It will depend on which IDR plan you select, however there’s a normal income-based compensation system calculation you can begin with.

1. Begin along with your AGI. Then, subtract 150% of the poverty level for your family size. That is your discretionary revenue within the pupil mortgage world.

AGI – (150% x Poverty Stage) = your discretionary revenue

2. As soon as your discretionary revenue, multiply by both 10% for REPAYE or PAYE, or 15% for IBR.

[AGI – (150% x Poverty Level)] x 10% = annual cost for PAYE and REPAYE

[AGI – (150% x Poverty Level)] x 15% = annual cost for IBR

3. Divide by 12 for month-to-month funds.

Bonus, our free student loan calculator does all of this sophisticated math for you. I do know some readers wish to nerd out as we do, however it’s all completed by the calculator, so all you actually need to know is your revenue.

Now that we all know how revenue is outlined, and the way income-based compensation is calculated, let’s take a look at some examples.

Situation 1 – First timers

New to income-driven compensation? This state of affairs is for you.

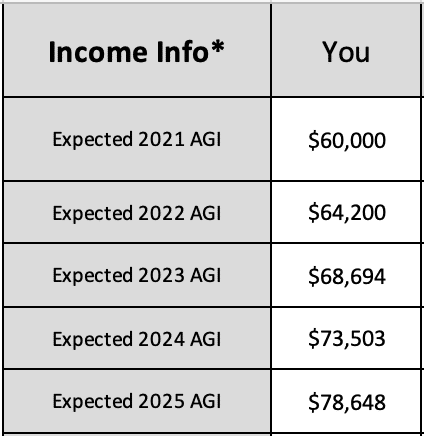

Let’s say you’re leaving your MBA with $125,000 of federal pupil mortgage debt and are beginning a job on the decrease finish of the spectrum to “be taught the ropes.” You anticipate making about $60,000 per 12 months, however anticipate your wage to drastically improve rapidly — about 7% per 12 months — for the subsequent 10 years.

You’re at the moment single for the sake of simplicity (however we’ll take a look at a wedding instance later). Right here’s how your revenue grows, and your choices for pupil mortgage funds.

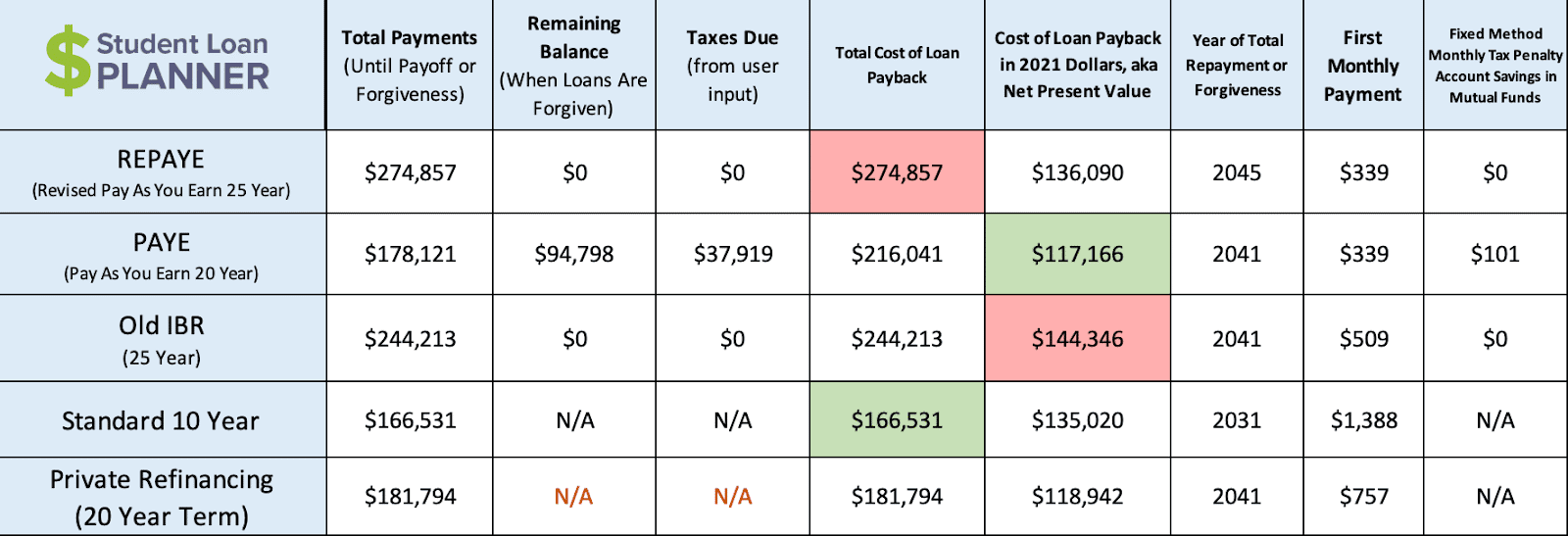

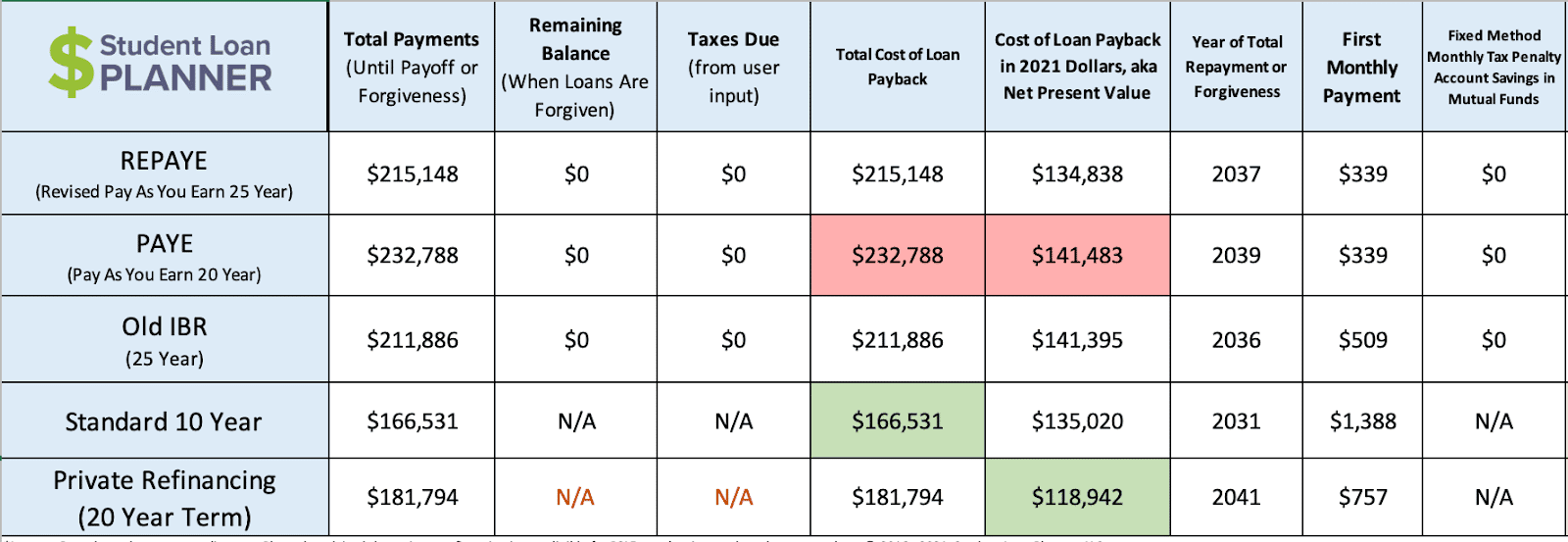

Once you graduate you’ll robotically be positioned on the usual 10-year plan, a month-to-month pupil mortgage cost of $1,388 monthly. That’s painful for a brand new skilled beginning at a $60,000 wage.

Utilizing a 4% rate of interest over a 20-year time period, you might pay $757 monthly by refinancing. You’ll need to qualify for a low refinancing rate of interest like 4%, so that you’ll want good credit score or a cosigner.

Probably the most favorable income-based choices are REPAYE, PAYE, or IBR. REPAYE and PAYE are each 10% of your discretionary revenue, versus IBR which is 15% of your discretionary revenue. We’ll go together with PAYE compensation for this state of affairs. A cost of $339 monthly is far more manageable than $1,388.

As you see with growing revenue, whether or not that improve is 1% per 12 months or 7% per 12 months, your month-to-month PAYE cost progressively will increase.

By way of the overall value of mortgage payback, the usual 10-year plan is the best choice, however keep in mind the month-to-month cost? It’s $1,388 monthly. Yikes.

Below the PAYE state of affairs, you’ll begin with decrease month-to-month funds of $339/month, and finally spend $178,121 paying your pupil loans again. You’ll want to save lots of about $100 monthly right into a taxable brokerage account to save lots of for the tax bomb of roughly $38,000 over the lifetime of the mortgage (20 years).

If we take a look at in the present day’s {dollars}, or internet current worth (NPV), PAYE is the winner, however it’s very near the overall NPV beneath refinancing. That’s why paying back loans from your MBA will be sophisticated.

Understanding you may pay between $165,000 to $275,000 for $125,000 of pupil mortgage debt, you must take into account aggressively paying these again to keep away from as a lot curiosity as potential, however there’s an argument for PAYE and personal financing on this case.

See? Difficult.

Situation 2 – First timer + marriage

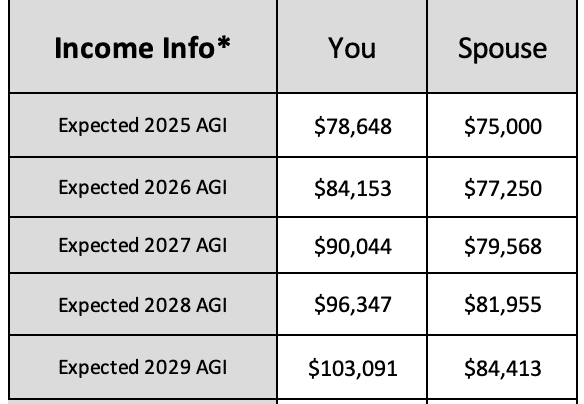

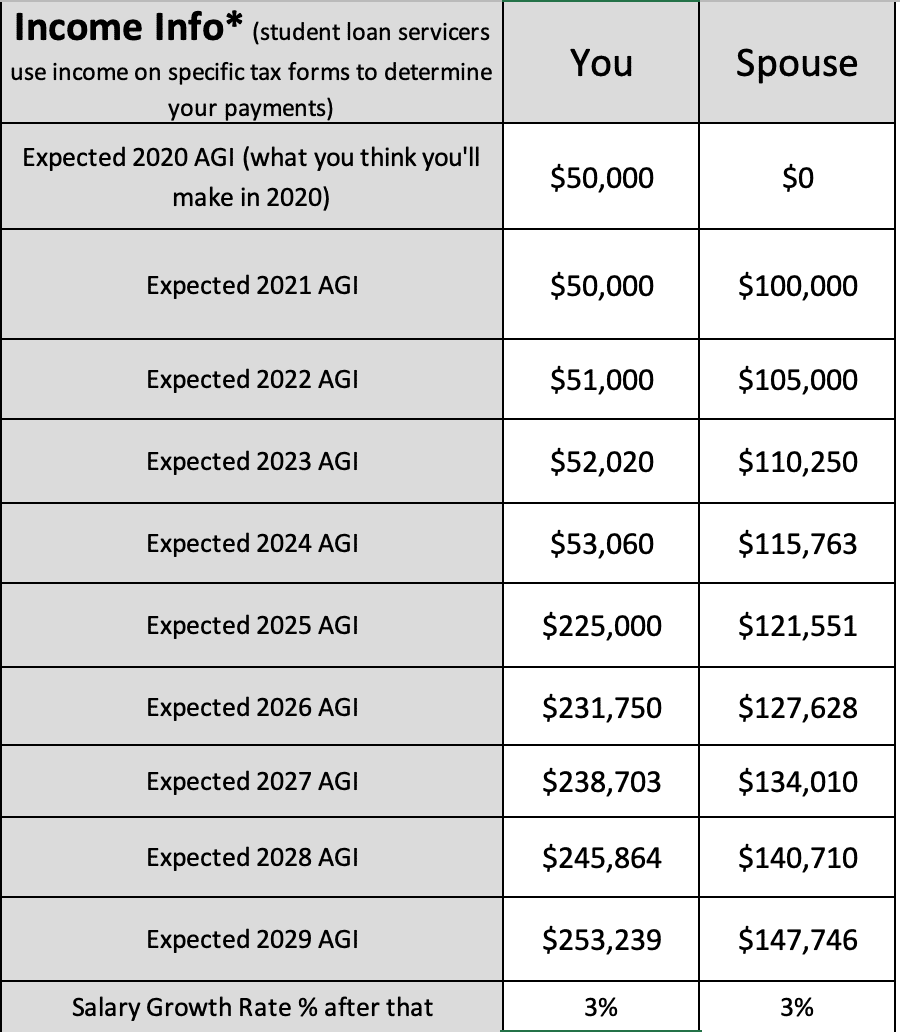

On this state of affairs, our latest MBA graduate marries a nurse making $75,000 per 12 months in 2025. They determine to file their taxes collectively. This modifications our MBA borrower’s state of affairs considerably.

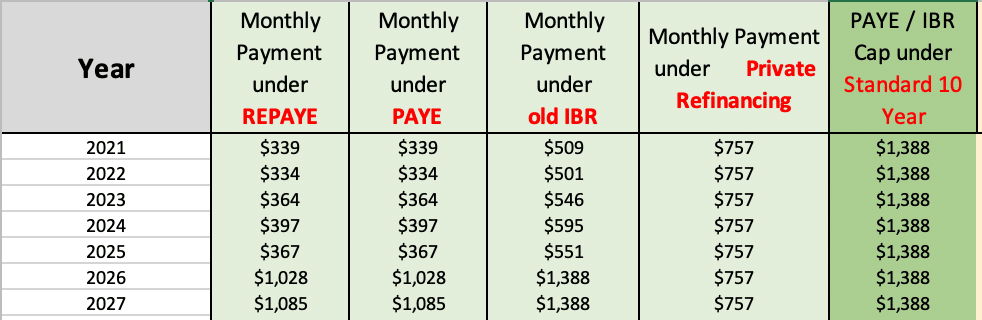

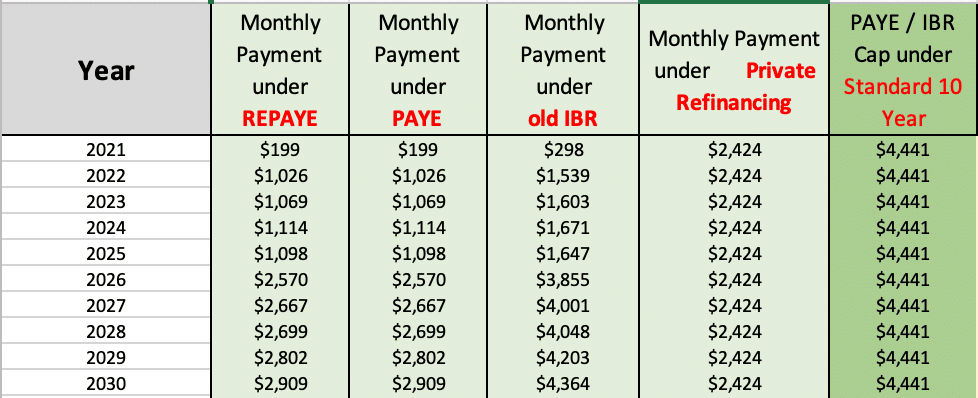

Observe that the usual 10-year and personal refinancing outcomes keep the identical, however all three income-driven compensation choices change, drastically. For instance, in 2026 beneath PAYE, our MBA borrower’s cost jumps from $367 to $1,028 by including their partner’s revenue.

PAYE is now the worst-case state of affairs. The loans are off by 2039, however refinancing to a decrease rate of interest and paying over 20 years is the best choice by way of in the present day’s {dollars}.

This state of affairs is a superb case for filing your taxes separately. For those who file individually, you’re allowed to exclude your partner’s revenue out of your mortgage cost calculation. It’s not a match for everybody, and you may lose out on some advantages like:

- The scholar mortgage curiosity deduction of $2,500 — this won’t be relevant to you, nevertheless, should you make a excessive sufficient revenue.

- Extra advantageous tax brackets, until you’re in a neighborhood property state.

- Baby care tax credit score.

- Earned revenue tax credit score.

- Exclusion or credit score for adoption bills.

- Capacity to contribute to a Roth IRA, although you may nonetheless make the most of the back-door Roth conversion method.

- Capacity to deduct rental property losses.

- Capacity to take the usual deduction in case your partner itemizes, or vice versa.

Situation 3 – Leaving residency

In our ultimate state of affairs, let’s shift gears and take a look at a drastic improve in revenue.

A health care provider is ending their residency or fellowship, the place their revenue will go from about $50,000 per 12 months to $225,000 per 12 months. They’re working at a nonprofit hospital and received married in 2021. This borrower plans to have children beginning in 2025.

Right here’s their revenue and compensation outlook:

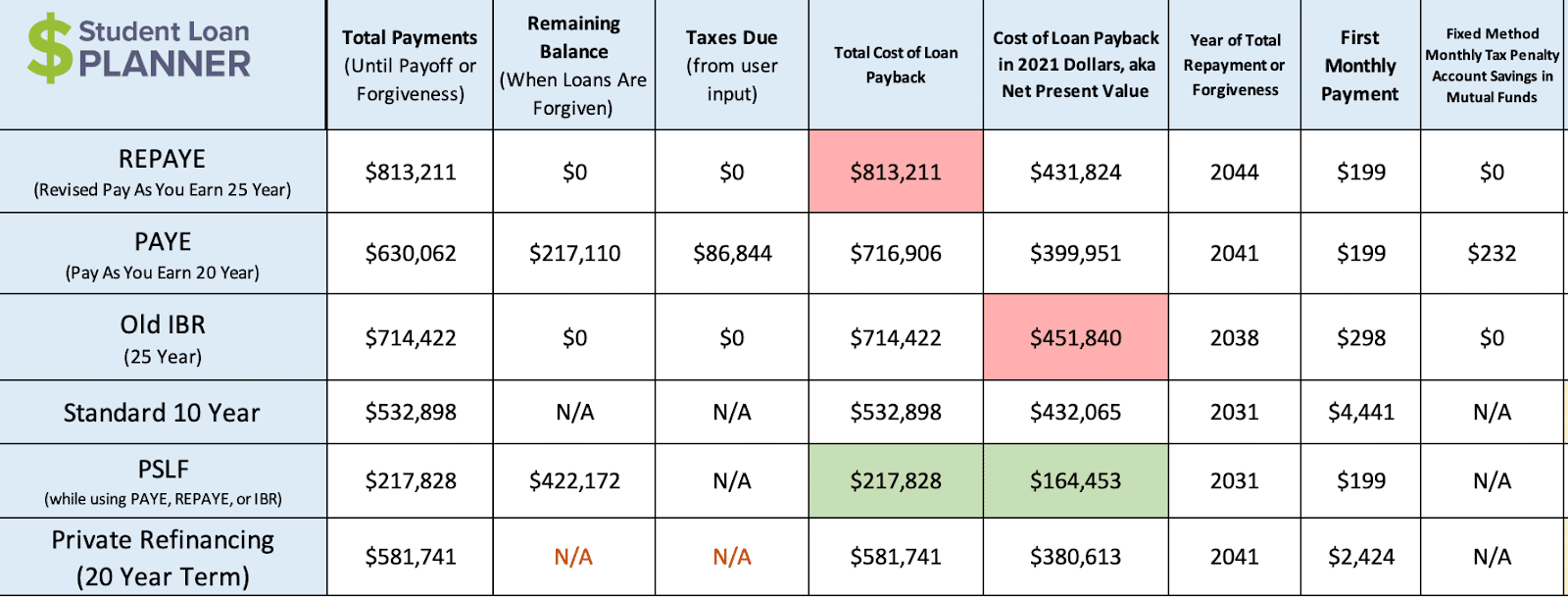

As you may see, as a result of we’re speaking about income-driven compensation plans, the upper the revenue, the upper the cost. The usual 10-year plan would require a $4,441 month-to-month cost primarily based on their $400,000 pupil mortgage stability.

Non-public refinancing is best at about $2,424, however IDR eases a few of that burden, particularly if this explicit doctor is working for a nonprofit hospital.

Even when this couple decides to maintain their tax scenario easy and file collectively, our doctor nonetheless comes out on prime due to Public Service Loan Forgiveness (PSLF).

Particularly, working for a nonprofit hospital via residency, fellowship, and for a couple of years out of fellowship can save the doctor over $300,000 in comparison with their subsequent best choice — the usual 10-year compensation plan with that dreaded $4,000+ cost.

Shockingly, submitting taxes individually from their partner can save one other $100,000.

Key takeaways

To calculate your income-driven compensation quantity, you could know:

- Your AGI. That is discovered immediately in your most up-to-date tax return.

- The federal poverty line for your loved ones measurement.

Issues to contemplate:

- Your eligibility for every compensation plan.

- Your retirement financial savings choices (Trace: it could actually’t damage to save lots of extra).

- Learn how to file your taxes (joint versus individually).

- Which state you reside in. Community property states have completely different guidelines relating to taxes.

- How sophisticated you need your pupil mortgage plan to be.

Does this really feel fully overwhelming? It’s actually sophisticated, which is why we’re right here for you. Schedule a consultation with us and we’ll assessment your particular person circumstances. Having a custom-made pupil mortgage plan can take an enormous weight off your shoulders.

[ad_2]

Source link

{kind=link}