[ad_1]

Nurse practitioners are extraordinarily useful to the medical neighborhood and sufferers. They’ll specialise in many alternative areas of medication, similar to ladies’s well being, psychiatric psychological well being, oncology, adult-gerontology, and extra. However the most typical might be pediatrics. NPs who work with children sometimes have the Household Nurse Practitioner (FNP) designation.

Whereas NPs aren’t main care physicians, they know their stuff and supply high-quality care. The education requirements to turn into a nurse practitioner (a.ok.a. Superior Observe Registered Nurse) have gotten much more strong. Which means nurse practitioners are much more expert than earlier than and might deal with extra complicated medical circumstances.

However with extra coaching comes extra pupil debt. The excellent news is that NPs are in excessive demand and might end their training at a comparatively low value in comparison with the typical nurse practitioner wage. Plus, a lot of them are eligible for favorable mortgage reimbursement like Public Service Mortgage Forgiveness (PSLF).

So is changing into a nurse practitioner value it? Let’s take a deeper dive into the training, salaries, and common pupil debt that can assist you determine if pursuing a nursing profession as an NP is definitely worth the effort and time.

Training necessities for nurse practitioners

Based on the American Association of Nurse Practitioners (AANP), the trail to changing into an NP begins with incomes your Bachelor of Science in Nursing (BSN) and having handed the Nationwide Council Licensure Examination (NCLEX-RN). You’ll then have to take an NP-focused graduate grasp’s or doctoral nursing program (DNP).

DNP applications have risen in reputation over the previous 15+ years because the American Affiliation of Faculties of Nursing (AACN) recommending that superior follow nurses earn doctorates. Immediately, there are over 350 DNP applications scattered by each U.S. state and the District of Columbia.

Lastly, potential nurse practitioners should website for and cross a nationwide board certification examination with a view to turn into licensed. The three hottest certification boards for NPs are the American Academy of Nurse Practitioners Certification Board (AANPCB), the Pediatric Nursing Certification Board, and the American Nurses Credentialing Heart (ANCC).

Associated: How to Become a Nurse Practitioner: Salary, Debt, And What to Expect

Nurse practitioners graduate with extra pupil loans than anticipated

Not too way back, NPs might get a Grasp of Science Diploma in Nursing (MSN) after two years, costing them between $20,000 and $40,000. They may then begin incomes near $100,000.

Now employers are sometimes in search of NPs with their Physician of Nursing Observe (D.N.P.) diploma. This four-year program doubles the years of college and greater than doubles the price of changing into an NP. As I mentioned earlier than although, everybody advantages from more-skilled NPs.

The typical NP we’ve labored with right here at Pupil Mortgage Planner® has about $149,000 in pupil loans. That is on the rise because of the tuition hikes. So is changing into a nurse practitioner value it? Let’s have a look the typical NP wage to get a greater gauge.

Nurse practitioner wage comparability

Based on the Bureau of Labor and Statistics (BLS), the median nurse practitioner wage is round $111,680 per yr. That’s really about $7,000 lower than median pay for all superior follow registered nurses (APRNs). Nevertheless it’s over $36,000 greater than nurses that graduated from an affiliate diploma program (ADN) or BSN program.

The wage can fluctuate by state too. There are at present the top-paying state for nurse practitioners by imply wages:

- California: $145,970

- New Jersey: $130,890

- Washington: $126,480

- New York: $126,440

- Massachusetts: $126,050

The median wage for a university graduate is at present about $74,152 according to the BLS. So changing into a nurse practitioner results in an additional $37,000 in earnings per yr by the averages.

Let’s assume that $37,000 in additional earnings sustains all through the whole 40-year profession of a NP. That works out to an additional $1,480,000 in lifetime earnings for an NP in comparison with somebody with a bachelor’s diploma. That’s an enormous quantity!

Taking out $149,000 in loans to make almost an additional $1.5 million appears to make nice monetary sense on the floor. However, keep in mind, these additional earnings will probably be taxed. We additionally need to think about the price to repay the coed loans.

If we assume a mixed 40% tax price for federal and state, then we will scale back that $1.48 million in earnings right down to about $888,000 in additional take residence pay. So now we’re speaking about NPs having an additional $888,000 to repay the $149,000 of pupil mortgage debt.

Appears good on the floor. However we must always dig deeper. Let’s discover the price of paying again the coed loans to see if it is sensible.

Nurse practitioner pupil mortgage reimbursement choices

We’ve accomplished over 5,500 consults and suggested on over $1.2 billion of pupil debt right here at Pupil Mortgage Planner®. Our expertise reveals there are two optimum methods for NPs to pay off their student loans:

- Aggressive Pay Again: For individuals who owe 1.5 instances their earnings or much less (e.g. a nurse practitioner who makes $100,000 with loans at $150,000 or much less), their finest wager might be to throw each greenback they will discover into paying again their loans as quick as attainable, in 10 years or much less. NPs ought to be sure you have a look at their PSLF choices earlier than refinancing. Typically this contains refinancing student loans to get a greater rate of interest.

- Pay the least quantity attainable: For nurse practitioners who owe greater than twice their earnings (e.g., $100,000 wage and $200,000 or extra in pupil loans), the objective is to get on an income-driven repayment plan that can preserve funds low and maximize mortgage forgiveness, whether or not it’s by PSLF or taxable mortgage forgiveness.

The nurse practitioner employer (nonprofit or non-public follow) might be the largest think about selecting between both possibility.

PSLF vs. refinancing for nurse practitioners

Let’s say Melissa has $150,000 in pupil loans at 6.8% curiosity. She’s been a nurse practitioner in Texas for 3 years and was paying on the graduated plan to maintain her funds low.

Proper now, she’s making $100,000 at an employer that will qualify for Public Service Loan Forgiveness (PSLF) with projected 3% wage will increase for the foreseeable future. She’s not married.

In nearly all circumstances, the graduated plan goes to finish up costing a nurse practitioner more cash than they’d in any other case need to spend when paying again their loans.

The graduated plan is neither possibility 1 nor possibility 2 listed above and is way more expensive. Melissa will find yourself paying off a 6.8% mortgage in full over 30 years with rising funds each 2 years.

It appears like a good suggestion to assist with month-to-month money stream. However 99 out of 100 instances, it’s one of many worst reimbursement choices. Selecting PSLF or refinancing to a 10-year fastened price will each value lower than that.

Bear in mind the graduated plan is just not a reimbursement program that qualifies for PSLF. So let’s evaluate beginning on the PSLF path now versus refinancing to a 10-year fastened price.

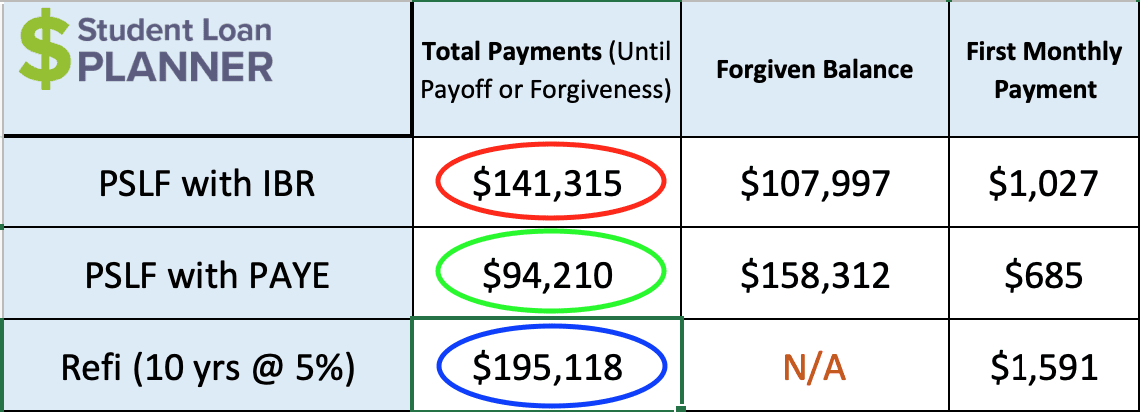

It’s essential to see the distinction in going for PSLF on Pay As You Earn (PAYE) versus Earnings-Based mostly Compensation (IBR). You’ll be able to see being on IBR would value Melissa about 50% extra to pay again her loans in comparison with PAYE. Nurse practitioners with pupil debt who’re eligible for PAYE ought to nearly by no means be on IBR.

As for PSLF with PAYE versus refinancing, PSLF is the clear winner. It’s projected to value about $100,000 much less then refinancing — $94,210 versus $195,118.

However ought to Melissa be beholden to a nonprofit employer simply to get PSLF?

When is it okay for a nurse practitioner to forgo PSLF?

Melissa likes her job working for the nonprofit hospital. However she received a suggestion for a personal follow job the place she’d earn $125,000. That’s an above-average nurse practitioner wage in Texas.

Would it not make extra sense financially to remain the place she is and get PSLF? Or ought to she take the brand new job, hand over PSLF and make more cash to repay her loans in full?

The job transfer might imply her pupil mortgage reimbursement might value $100,000 extra over 10 years. That works out to paying $10,000 per yr.

In different phrases, her take-home pay must enhance by greater than $10,000 for the yr. All of that extra cash must go towards paying again the refinanced mortgage to interrupt even with PSLF.

However Melissa goes to make a further $25,000 in non-public follow and take residence $15,000 extra per yr. If she pays an additional $10,000 towards her mortgage every year, she’d nonetheless have a further $5,000 in take-home pay. Now that makes monetary sense!

If Melissa and I have been having a dialogue about this, I’d let her know that refinancing means giving up PSLF for good. So we’d discuss taking the job however retaining her loans within the federal program till she’s sure she needs to remain within the non-public area. When she’s 100% sure, she’d wish to refinance her loans to drop the rate of interest down from 6.8% into the 5% vary.

Is changing into a nurse practitioner value it?

The pure monetary reply is sure. The projected lifetime earnings of a nurse practitioner versus the typical school grad is $888,000 after taxes. That is in comparison with the $195,000 estimated value of paying again pupil loans with the extra expensive path.

Both method, most nurse practitioners ought to have a objective to be pupil debt free in 10 years or much less. That might be by refinancing and paying it off in full or going for PSLF and saving aggressively on the facet.

Similar to any career, NP candidates ought to solely pursue this path in the event that they’re all in and pupil loans gained’t make them remorse their resolution.

Having a transparent understanding of how mortgage reimbursement works and the way to mitigate each the monetary and psychological points of carrying that quantity of debt are a should earlier than coming into faculty.

Nurse practitioners want a plan for pupil mortgage reimbursement

Nurse practitioners can discover a clear path to pay again their pupil loans. A path that might not solely save them vital cash however assist them perceive the actions steps to get it accomplished.

Pupil Mortgage Planner® has accomplished over 5,500 pupil mortgage consults for purchasers with over $1.3 billion of pupil loans. Our group will help you determine the optimum path to pay again your loans in simply 1 hour.

You’ll be able to learn more about our consult process here. Or you possibly can e book your session now by clicking the button beneath.

Refinance pupil loans, get a bonus in 2021

$1,000 BONUS1 For 100k or extra. $200 for 50k to $99,999¹

$1,050 BONUS2For 100k+. $300 bonus for 50k to 99k.2

$1,250 BONUS3 For 250k+, tiered 300 to 500 bonus for 50k to 250k.3

$1,275 BONUS4 For 150k+. Tiered 300 to 575 bonus for 50k to 149k.4

$1,000 BONUS5For $100k or extra. $200 for $50k to $99,9995

$1,250 BONUS6 For 100k+ or $350 for 5k to 100k.6

$1,250 BONUS7For 150k+. Tiered 100 to 400 bonus for 25k to 149k.7

Undecided what to do along with your pupil loans?

Take our 11 query quiz to get a customized suggestion of whether or not it is best to pursue PSLF, IDR forgiveness, or refinancing (together with the one lender we expect might provide the finest price).

All charges listed above symbolize APR vary. 1Earnest: $1,000 for $100K or extra, $200 for $50K to $99.999.99. For Earnest, should you refinance $100,000 or extra by this website, $500 of the $1,000 money bonus is offered instantly by Pupil Mortgage Planner. Charge vary above contains non-compulsory 0.25% Auto Pay low costEarnest disclosures.

2Commonbond: For those who refinance over $100,000 by this website, $500 of the money bonus listed above is offered instantly by Pupil Mortgage Planner. Commonbond disclosure.

3Laurel Street: For those who refinance greater than $250,000 by our hyperlink and Pupil Mortgage Planner receives credit score, a $500 money bonus will probably be offered instantly by Pupil Mortgage Planner. If you’re a member of an expert affiliation, Laurel Street would possibly give you the selection of an rate of interest low cost or the $300, $500, or $750 money bonus talked about above. Provides from Laurel Street can’t be mixed. Charge vary above contains non-compulsory 0.25% Auto Pay low cost. Laurel Road disclosures.4Elfi: For those who refinance over $150,000 by this website, $500 of the money bonus listed above is offered instantly by Pupil Mortgage Planner. Elfi disclosure. 5Sofi: For those who refinance $100,000 or extra by this website, $500 of the $1,000 money bonus is offered instantly by Pupil Mortgage Planner. Charge vary above contains non-compulsory 0.25% Auto Pay low cost. Sofi disclosures. 6Credible: For those who refinance over $100,000 by this website, $500 of the money bonus listed above is offered instantly by Pupil Mortgage Planner. Credible disclosure.

7LendKey: For those who refinance over $150,000 by this website, $500 of the money bonus listed above is offered instantly by Pupil Mortgage Planner. Charge vary above contains non-compulsory 0.25% Auto Pay low cost.

[ad_2]

Source link

{kind=link}