[ad_1]

Whereas Direct Unsubsidized Loans include annual borrowing limits, MBA college students can borrow as much as their complete value of attendance with Grad PLUS Loans. And this limitless fountain of federal scholar assist typically leads MBA faculties to cost excessive tuition charges and college students to finish up with giant quantities of MBA debt.

Round 200,000 individuals graduated with an MBA in 2018. In response to a Bloomberg Businessweek survey, 18% borrowed greater than $100,000 in scholar loans, with the majority of these individuals attending high 25 enterprise faculties. Seventeen p.c borrowed between $50,000 to $100,000. When including in undergrad loans, many MBA program graduates find yourself with six figures of scholar debt.

In contrast to graduating as a health care provider, veterinarian or dentist, MBA grads have a bunch of various profession choices to select from. The Bureau of Labor Statistics cites 21 completely different enterprise and monetary occupations with their median salaries. However even an inventory of that dimension isn’t complete. For instance, it doesn’t checklist entrepreneurship, enterprise government and lots of different profession choices.

The MBA is essentially the most versatile graduate diploma, which suggests the optimum mortgage compensation technique may very well be everywhere in the map, relying on the profession path the MBA grad decides to take. Earlier than we dive into strong compensation methods, it’s vital to notice the variations between scholar debt and different sorts of debt.

What makes MBA debt completely different than commonplace debt?

Pupil debt has two nuances that make mortgage compensation completely different from different unsecured debt. First, scholar mortgage curiosity is easy curiosity. If month-to-month funds don’t cowl the mortgage curiosity, it merely accrues in one other bucket. It doesn’t compound.

This implies when evaluating an funding with a projected return of 6% compounded with paying off 6% of scholar mortgage debt, the funding with compound curiosity could be the higher choice from a monetary optimization standpoint (with out accounting for danger, after all).

Only a small word: There are some things that might set off the curiosity to capitalize, like placing MBA loans in forbearance, lacking a fee or switching compensation plans.

Second, scholar loans have plans primarily based on revenue, not the quantity owed, with both taxable or tax-free mortgage forgiveness on the finish of the compensation time period. Let’s say two people are working as monetary analysts making the very same revenue. However one owes $150,000 for his or her MBA and undergrad and the opposite owes $300,000.

Their funds could be completely different in the event that they have been on plans the place the funds have been primarily based on the quantity of debt, comparable to the usual, prolonged or graduated plan. The one who owes $300,000 would have funds just about twice as giant the one who owes $150,000.

That’s not the case in the event that they’re each on an income-driven plan like Revised Pay As You Earn (REPAYE). The quantity of debt is irrelevant when calculating the funds. The month-to-month fee is predicated on their revenue. Within the instance of the 2 debtors with completely different quantities of debt, they might have the identical precise month-to-month fee in the event that they have been on REPAYE.

MBA scholar mortgage compensation choices

It appears fairly easy. You have got debt. Discover the lender that gives the bottom rate of interest and both carry the leverage to optimize your return on fairness or pay it off shortly to maximise money stream in the long term. And, for personal loans, that straightforward technique might be finest.

However MBA scholar mortgage debt compensation on federal scholar loans is a bit bit trickier because of the compensation choices accessible to repay MBA debt. Right here at Pupil Mortgage Planner, we’ve completed over 5,000 consults and suggested on over $1,3 billion of scholar debt. Our expertise exhibits there are two optimum methods to repay scholar loans:

Aggressive Pay Again: For individuals who owe 1.5 instances their revenue or much less (e.g., the MBA grad who makes $100,000 with loans at $150,000 or much less), their finest guess is normally to throw each greenback they will into paying again their loans as quick as doable for not more than 10 years. Revenue-driven compensation doesn’t sometimes come into the image.

Pay the least quantity doable: For individuals who owe greater than twice their revenue (e.g., an MBA grad who makes $60,000 and owes $120,000 or extra), the objective is to get on an income-driven compensation plan that may maintain their funds low and maximize taxable mortgage forgiveness. This may be optimum resulting from easy curiosity, in addition to the distinction in paying off the debt in full in comparison with having 20 to 25 years to save lots of and make investments for the tax portion.

MBA scholar mortgage compensation situations

Let’s check out a few completely different situations — one the place the particular person owes greater than twice their revenue and one other the place they owe lower than 1.5 instances their revenue.

Notice that in all of the situations under we’ll assume that 100% of the coed debt is in federal loans. If in case you have a non-public scholar mortgage, you must ignore the advances methods under and begin wanting into your refinancing choices with non-public lenders.

State of affairs 1

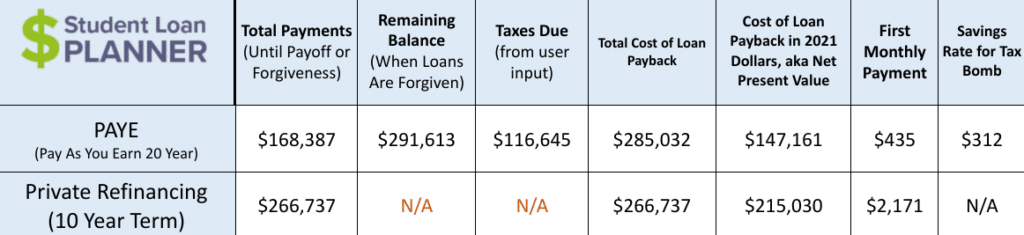

Let’s say Jon has $200,000 of undergrad and MBA debt at 6.5% curiosity. He’s making $70,000 a 12 months with 5% projected revenue development for the following 10 years.

PAYE is the clear winner right here from a wealth-optimization standpoint. After including up the projected funds of $168,387 over the following 20 years and the tax bomb of $116,645 due in 20 years, it could solely value Jon $20,000 extra out-of-pocket than refinancing. However he’d have the ability to unfold out the price over 20 years on PAYE versus solely 10 with refinancing.

That is extra obvious when looking at the cost of loan payback, or web current worth (NPV), for PAYE. It’s about 31% lower than refinancing utilizing the assumptions of 5% funding development and three% inflation.

Fairly than making month-to-month funds of $2,171 for 10 years, Jon would really find yourself in a greater spot from a net-worth standpoint by occurring PAYE and investing on the aspect for the tax bomb of $116,645. He may make his funds, save $312 per thirty days for the tax bomb (at 5% annualized development) and nonetheless have the cash to speculate one other $1,400 per thirty days.

State of affairs 2

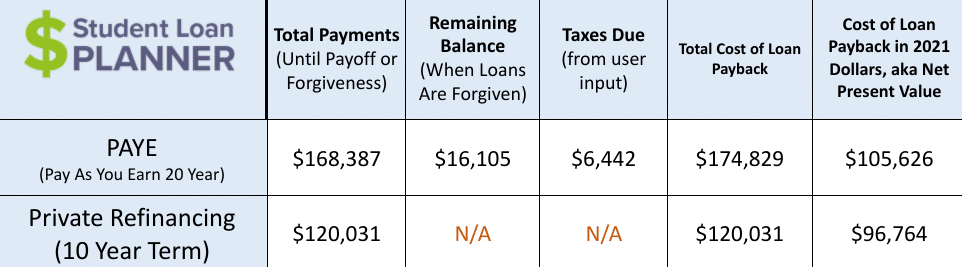

Let’s say Janet has $90,000 of undergrad and MBA debt at 6.5%. She’s making $70,000 a 12 months with 5% projected revenue development for the following 10 years — similar as Jon.

Janet’s state of affairs clearly favors refinancing and aggressively paying off the mortgage. She will be able to save $54,000 out of pocket paying again the loans and be debt-free in 10 years as an alternative of 20. The fee of $977 per thirty days on a $70,000 wage is far more manageable than Jon’s $2,171.

One different factor to level out is their funds on PAYE could be equivalent — $435 per thirty days for the primary 12 months — as a result of their revenue is the very same. Regardless that Jon has greater than twice the coed loans of Janet.

These two situations are pretty clear-cut. However what occurs if somebody begins out with a debt-to-income of 2-to-1, but has a excessive income-growth trajectory? How do they deal with their MBA debt once they can’t afford the massive fee however will have the ability to within the subsequent two to a few years?

The REPAYE curiosity subsidy & waiving the grace interval

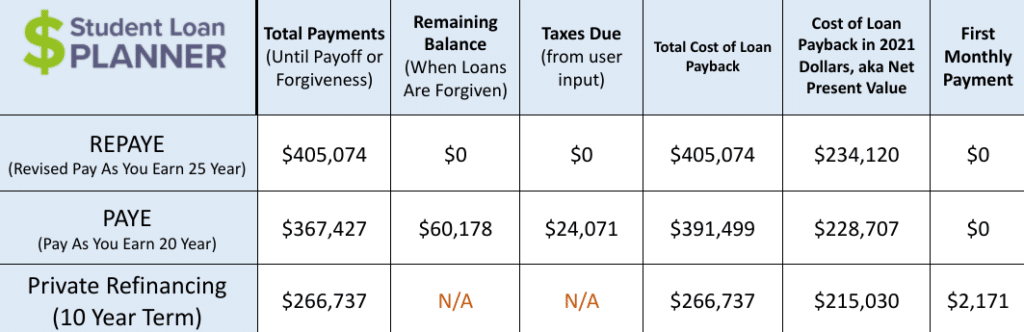

Let’s say Samantha simply graduated and owes $200,000 in scholar loans at 6.8%. Proper now, she’s not working however will begin at her job in two months making $70,000. She expects her revenue to develop quickly and anticipates making $150,000 in 5 years and $250,000 in 10 years.

Refinancing is one of the best long-term choice, however she will’t make that $2,171 fee proper now.

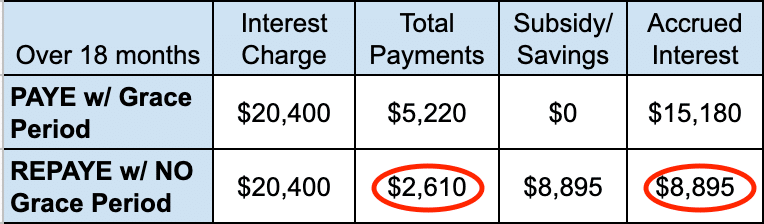

If she chooses to attend her complete grace interval after which chooses PAYE, her mortgage would have accrued six months of curiosity — $6,800. Her month-to-month fee would then be $435 or $5,220 for 12 months, primarily based on a $70,000 revenue. After 12 months on PAYE, she would have accrued one other $8,380 on the mortgage ($13,600 in curiosity – $5,220 of funds).

So by the tip of 18 months (the six-month grace interval plus 12 months on PAYE), she would have accrued $15,180 of curiosity and made $5,220 in funds.

Right here’s a complicated method she will use to economize paying again her loans whereas maintaining her funds low for 2 to a few years and slowing down the expansion of the mortgage: Consolidate in an effort to waive the grace interval, go on Revised Pay As You Earn (REPAYE) after which refinance when she will make the $2,000-plus fee.

Right here’s the way it works.

The REPAYE curiosity subsidy

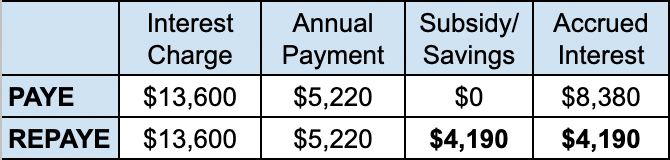

Let’s begin with speaking concerning the REPAYE interest subsidy: The easy clarification is that any curiosity that may accrue on the mortgage will get reduce in half, which cuts the mortgage development in half.

In different phrases, that $8,380 that may accrue on the mortgage beneath PAYE could be half of that beneath REPAYE — $4,190. The federal government subsidizes, or wipes away, the opposite $4,190 that may have accrued on the mortgage.

Since Samantha goes to pay the mortgage again in full anyway, the curiosity subsidy would save her $4,190 simply by choosing REPAYE.

However what if she waives the grace interval, goes on REPAYE six months earlier and begins making funds immediately?

The curiosity subsidy cuts accrued curiosity

One other superior profit on this case is that she isn’t working in the intervening time. Together with her revenue at $0, her REPAYE funds ought to be $0 for 12 months. Plus, waiving the grace interval to go on REPAYE means the six months of curiosity costs that may have accrued on her loans whereas within the grace interval will get reduce, too. She received’t need to certify her $70,000 revenue till it’s time to recertify in 12 months.

Right here’s how a lot Samantha may save by implementing this technique over 18 months. Beneath PAYE, she’s taking the complete six-month grace interval, then making 12 months of funds. With REPAYE, she’s waiving the grace interval, then making 12 months of funds at $0 and 6 months at $435:

Implementing this technique is projecting to chop her funds in half over that point and save her $8,895 in accrued curiosity, in comparison with a extra conventional method and going to PAYE.

Guess the place all that cash finally ends up as an alternative of getting used to pay again her loans? Her checking account.

This technique isn’t for everybody, and consolidation ought to actually be thought out if there’s any credit score towards mortgage forgiveness, whether or not taxable or Public Service Mortgage Forgiveness. Nevertheless it works properly for somebody in Samantha’s state of affairs.

It’s a no brainer that may save her virtually $10,000 over 18 months. As soon as she will simply afford the 10-year fee and so long as she isn’t working for a nonprofit or authorities employer, she ought to look into refinancing if she will get a decrease rate of interest.

How one can refinance MBA scholar loans

There are a lot of on-line lenders in the present day that make it simple to use for a charge quote on scholar mortgage refinancing with no credit score test. You may as well use lender marketplaces like Credible to test your charges with a number of non-public lenders in minutes.

When selecting a refinancing lender, know that the entire respected corporations don’t cost origination charges or embrace a prepayment penalty. Lenders sometimes have a spread of charges they could cost with glorious credit score being required to entry the bottom charges.

You’ll usually have the choice to use for a hard and fast or variable charge loans. Nevertheless, with rate of interest at present hovering almost all-time lows, fastened charges are extraordinarily enticing. Selecting a variable rate of interest proper now could also be a riskier transfer than common. Notice that you simply could possibly scale back your rate of interest even additional when you join autopay. A 0.25% autopay low cost is commonest within the trade.

Along with charges, you’ll need to think about whether or not the lender permits durations of forbearance of educational deferment. And, relying in your credit score standing, you might also need to think about every lender’s cosigner and cosigner launch choices. Compare your student loan refinancing options here.

MBA grads want a plan for scholar mortgage compensation

MBA graduates can discover a clear path to payoff for his or her scholar loans. This path that might not solely save them vital cash — it may additionally assist them absolutely perceive the motion steps required to get it completed.

Pupil Mortgage Planner has completed over 5,000 scholar mortgage consults for purchasers with over $1.3 billion of scholar loans. We can assist you determine the optimum path in only one hour.

Our workforce can assist anybody so be at liberty to decide on the correct guide for you primarily based in your particular person circumstances. Be at liberty to e-mail me at [email protected] or guide a scholar mortgage plan under.

Refinance scholar loans, get a bonus in 2021

$1,000 BONUS1For 100k or extra. $200 for 50k to $99,999¹

$1,250 BONUS2For 250k+, tiered 300 to 500 bonus for 50k to 250k.2

$1,275 BONUS3For 150k+. Tiered 300 to 575 bonus for 50k to 149k.3

$1,000 BONUS4For $100k or extra. $200 for $50k to $99,9994

$1,050 BONUS5For 100k+. $300 bonus for 50k to 99k.5

$1,250 BONUS6For 100k+ or $350 for 5k to 100k.6

$1,250 BONUS7For 150k+. Tiered 100 to 400 bonus for 25k to 149k.7

Unsure what to do along with your scholar loans?

Take our 11 query quiz to get a personalised suggestion of whether or not you must pursue PSLF, IDR forgiveness, or refinancing (together with the one lender we expect may provide the finest charge).

1Earnest: $1,000 for $100K or extra, $200 for $50K to $99.999.99. For Earnest, when you refinance $100,000 or extra via this website, $500 of the $1,000 money bonus is offered instantly by Pupil Mortgage Planner. Charge vary above consists of non-compulsory 0.25% Auto Pay low costEarnest disclosures. 2Laurel Street: For those who refinance greater than $250,000 via our hyperlink and Pupil Mortgage Planner receives credit score, a $500 money bonus can be offered instantly by Pupil Mortgage Planner. In case you are a member of knowledgeable affiliation, Laurel Street would possibly give you the selection of an rate of interest low cost or the $300, $500, or $750 money bonus talked about above. Affords from Laurel Street can’t be mixed. Charge vary above consists of non-compulsory 0.25% Auto Pay low cost. Laurel Road disclosures.3Elfi: For those who refinance over $150,000 via this website, $500 of the money bonus listed above is offered instantly by Pupil Mortgage Planner. Elfi disclosure. 4Sofi: For those who refinance $100,000 or extra via this website, $500 of the $1,000 money bonus is offered instantly by Pupil Mortgage Planner. Charge vary above consists of non-compulsory 0.25% Auto Pay low cost. Sofi disclosures.5Commonbond: For those who refinance over $100,000 via this website, $500 of the money bonus listed above is offered instantly by Pupil Mortgage Planner. Commonbond disclosure. 6Credible: For those who refinance over $100,000 via this website, $500 of the money bonus listed above is offered instantly by Pupil Mortgage Planner. Credible disclosure.

7LendKey: For those who refinance over $150,000 via this website, $500 of the money bonus listed above is offered instantly by Pupil Mortgage Planner. Charge vary above consists of non-compulsory 0.25% Auto Pay low cost.

[ad_2]

Source link

{kind=link}