[ad_1]

Regardless of file unemployment and widespread monetary wrestle in 2020, some client markets have remained remarkably intact. Dwelling loans are considered one of them—and even with bodily limitations briefly hampering in-person homebuying, general mortgage debt within the U.S. reached file highs in 2020.

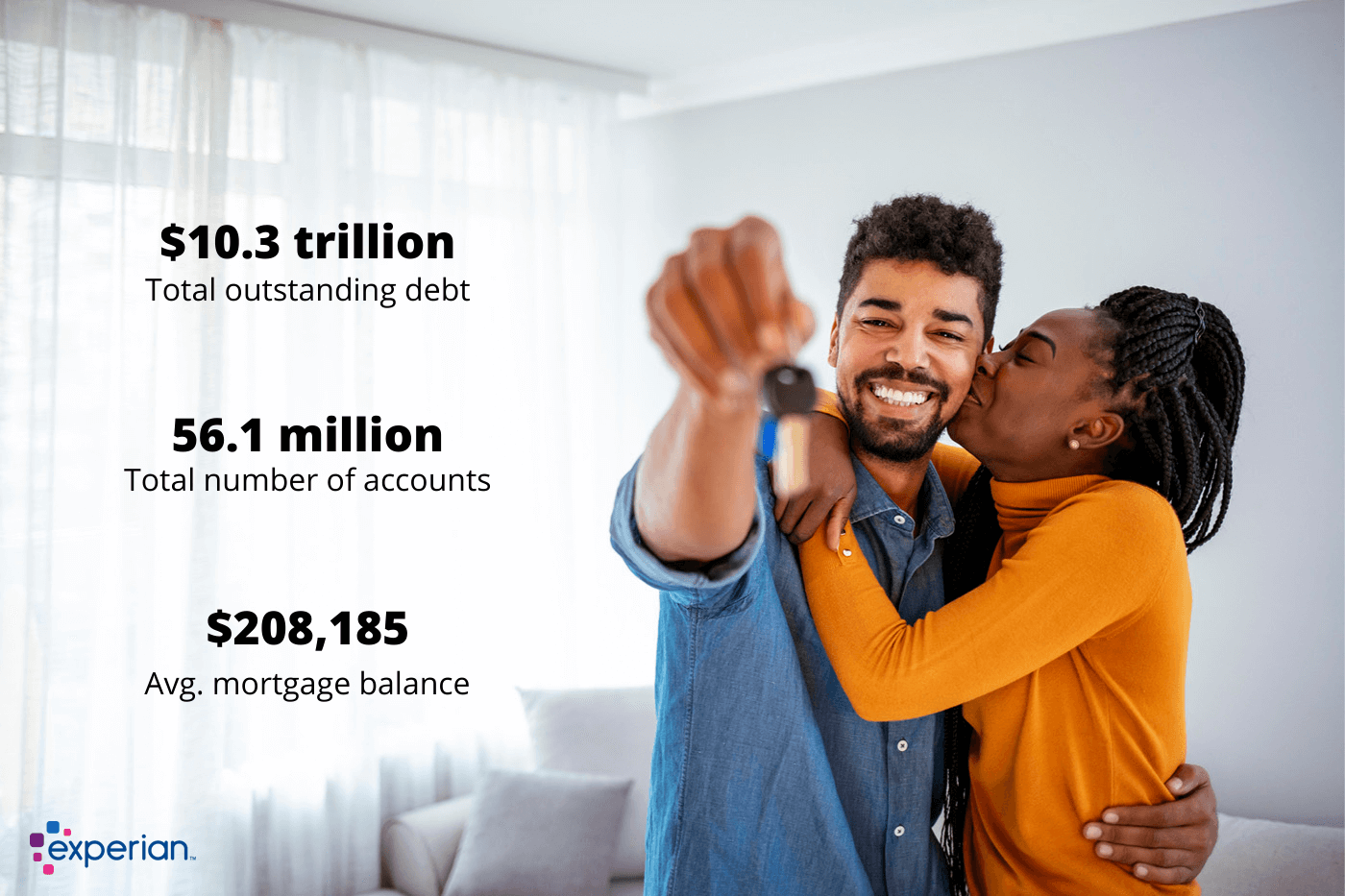

Within the midst of the pandemic, excellent mortgage debt rose to over $10.3 trillion within the third quarter (Q3) of 2020, in keeping with Experian knowledge. Particular person client mortgage balances additionally rose, rising to the best degree in at the least a decade.

One of these development in the course of the worst financial recession for the reason that Nice Melancholy is considerably shocking, and serves as a distinction to what occurred to the mortgage market in the course of the recession of the late 2000s. However because the pandemic and its impact on the financial system proceed, it is turning into clear that most of the monetary impacts of the present recession are distinctive.

As a part of our ongoing analysis on debt within the U.S., Experian reviewed credit score report knowledge to see how the previous 12 months has affected mortgage debt and to grasp what impression the pandemic has had on house loans. This evaluation compares yearly consultant knowledge from 2019 with the info from the third quarter (Q3) of 2020, the newest accessible knowledge.

General Mortgage Debt Sees Highest Enhance in Decade

From 2019 to 2020, mortgage debt grew by 7% to achieve a file excessive of $10.3 trillion, in keeping with Experian knowledge. Not solely did this debt attain a file excessive, nevertheless it grew on the quickest price it has in at the least 10 years—underscoring how important of a 12 months 2020 was for house loans.

Supply: Experian

Because the Nice Recession within the late 2000s, general mortgage debt has ebbed and flowed, with the development of development seen prior to now seven years approaching the heels of a half-decade contraction that preceded it. In 2008, mortgage debt hit a peak at $8.7 trillion. General mortgage debt decreased for the 5 years that adopted, shrinking to $7.7 trillion in 2013.

Then, mortgage debt started a gradual rebound, rising by $2.6 trillion to the place it stood as of Q3 2020. For context, that development eclipses the sum whole of all scholar mortgage and bank card debt mixed, and it occurred in simply seven years.

Regardless of this bounce again within the aftermath of the Nice Recession, customers in 2020 seem properly poised to handle their rising mortgage debt. Delinquency charges for mortgage holders are down (extra on that later) and the typical FICO® Rating☉ amongst mortgage holders is up. These statistics, whereas not consultant of each particular person’s monetary scenario, point out that People are typically managing their mortgage debt responsibly.

Shoppers Enhance Particular person Mortgage Debt by 2%

Consistent with the previous decade of general development, common particular person client balances grew in 2020, rising to $208,185, in keeping with Experian knowledge. In contrast to the rise in general debt, particular person balances elevated at a price of two%, which is analogous to the annual development seen over the previous decade. Even with the average development, particular person mortgage balances are nonetheless the best they’ve ever been.

Supply: Experian

As of 2020, roughly 44% of U.S. customers have a mortgage. That is unchanged since 2019, in keeping with Experian knowledge. Whereas the slice of the inhabitants with a house mortgage did not change, common mortgage balances are up, which reveals that buyers could also be borrowing greater than regular.

Traditionally low Federal Reserve charges helped ramp up competitors within the housing market in the course of the pandemic, and a few properties have been offered above asking worth because of this. In September 2020, in keeping with knowledge from homebuying web site Zillow, 1 in 5 properties offered above their itemizing worth. This means that competitors and ample demand could have pushed buy costs up, and together with different elements, could clarify why common mortgage balances are creeping up.

Mortgage Inquiries Rise Almost 50% at Onset of Pandemic

A contributing issue to a lot of the surge in general mortgage debt was the elevated variety of folks making use of for house loans. In early March 2020, on the onset of the pandemic, client inquiries for brand spanking new mortgage loans spiked by 47% in contrast with the identical interval in 2019, in keeping with Experian knowledge.

Almost a 12 months into the pandemic, it is clear the monetary impression was felt in a different way throughout numerous populations. Whereas many customers misplaced their jobs or noticed their wages decreased and encountered monetary hardship, others had been in a position to maintain their jobs and even discovered themselves spending lower than earlier than. On high of that, the Private Saving Fee recorded by the U.S. Bureau of Financial Evaluation reached file highs on the onset of the pandemic, most just lately (as of December) settling on the highest degree since 1975.

Together with the Federal Reserve dropping rates of interest in March 2020, customers whose monetary conditions had been safe, and even improved, in the course of the pandemic appeared to see 2020 as an opportune time to buy a house.

For nearly each month in 2020, the variety of arduous inquiries for brand spanking new mortgage loans was measurably larger than it was throughout the identical month within the prior 12 months. And whereas not all these inquiries become new loans, the surge in purposes reveals a degree of eagerness and monetary capacity that will not usually be anticipated throughout a monetary downturn.

Forbearances, Deferrals Double Throughout Pandemic

Although People have been making use of for mortgages at file charges over the previous 12 months, the variety of accounts positioned in forbearance or deferral has additionally risen sharply for the reason that onset of the pandemic. As the truth of the pandemic set in in April 2020, the variety of accounts in forbearance and deferral doubled, in keeping with Experian knowledge.

At one level in April 2020, the variety of accounts reported as in forbearance or deferral grew by 102%. The overall steadiness of those accounts elevated by 132% to greater than $567 billion. In Might 2020, each the variety of accounts and the entire steadiness recorded as in forbearance or deferral elevated once more. Complete balances on accounts in forbearance or deferral grew by 67% (to a complete of $944 billion) and the entire variety of accounts grew by an extra 60%, in keeping with Experian knowledge.

This sharp improve in paused mortgage reimbursement was probably sparked by the Coronavirus Help Reduction and Financial Safety (CARES) Act, which was signed into regulation on the finish of March 2020. The act required firms servicing government-backed mortgages to permit debtors financially impacted by the pandemic to briefly place their loans in forbearance.

To this point—when measured by the well being of general client credit score scores—these measures to keep away from delinquency and permit these impacted by the pandemic to change reimbursement appear to have labored.

Shoppers See Enchancment in Mortgage Delinquency Charges

Throughout the varied forms of debt within the U.S., customers persistently decreased their delinquency charges in 2020, and mortgage loans had been no exception. Since 2019, customers have seen important enchancment throughout measures of late fee severity.

The best change occurred amongst mortgage funds 60 to 89 days late (DPD), with the share of accounts thought-about delinquent to that diploma falling by 54%, in keeping with Experian knowledge.

Supply: Experian

This discount in delinquency charges reveals, amongst different issues, that buyers are lacking fewer funds than ever. A lot of this discount in delinquency may probably be attributed to the protections put in place by Congress and numerous lenders.

Fee historical past is crucial side of credit score scores, and the lower in delinquencies can probably be linked to general development of credit score scores, particularly the rating development seen amongst householders.

Credit score Scores Amongst Shoppers With a Mortgage Up in 2020

Since 2019, the credit score profile of customers with a mortgage has improved. The typical FICO® Rating amongst People with a house mortgage elevated from 747 in 2019 to 753 in 2020, in keeping with Experian knowledge. That is 43 factors larger than the nationwide common FICO® Rating, which was 710 in Q3 2020.

This rating enchancment mirrors the broader development of the typical FICO® Rating rising over time, however can also spotlight the truth that mortgage lenders have continued to make use of rigorous lending requirements.

Supply: Experian

These stats additionally provide reassurance that the pandemic has not brought about widespread bother (to date) to householders’ credit score scores. If protections had not been put in place to assist financially impacted debtors insulate their credit score to some extent, a wave of delinquencies and foreclosures might have severely impacted particular person scores and funds general.

When taking a look at mortgage debtors who’ve scores under the nationwide norm, solely round 15% of the customers with a mortgage in 2020 had been thought-about subprime or tremendous subprime debtors (these with a median FICO® Rating of lower than 670). These customers had a mortgage steadiness of $160,913 in 2020—23% lower than the nationwide common.

Mortgage Balances Noticed Largest Enhance Amongst Youngest Generations

Consistent with patterns throughout different forms of debt, youthful generations drove a wholesome portion of mortgage debt development in 2020. Since 2019, members of Era Z—the youngest technology in our evaluation—noticed their common balances spike by 19%, in keeping with Experian knowledge. That represents greater than a $27,000 improve in mortgage debt on common in only a 12 months.

Millennials, who noticed a fraction of the expansion that Gen Z did—rising their common mortgage steadiness by 6%—nonetheless had the second-highest spike of any technology. They had been adopted by Era X, child boomers and the silent technology.

Supply: Experian; Ages as of 2020

Shoppers in Almost All States Noticed Mortgage Debt Enhance

Throughout the nation, particular person mortgage balances elevated in all however one state between 2019 and 2020. Solely in Connecticut did client balances shrink—and simply barely at that. The typical mortgage debt in that state decreased by 0.3% in 2020.

General, 36 states and the District of Columbia noticed their mortgage debt improve at a price of over 2% (the nationwide common) in 2020. Shoppers in Idaho noticed the biggest annual improve, at 8.3%, and the smallest development was 0.4% in Illinois.

Debtors within the District of Columbia had the best mortgage debt of any state, carrying a median of $437,976—a rise of practically 4% since 2019. California had the second-highest common, with customers owing $371,981 in mortgage debt in 2020—over $8,000 or 2.2% greater than the earlier 12 months. The nation’s capital and California had been adopted by Hawaii, Washington and Colorado as having the best common mortgage debt.

Supply: Experian knowledge

How Did the COVID-19 Pandemic Affect Mortgages in 2020?

It is tough as an instance the pandemic’s full impression on house borrowing in 2020, however there are a number of tendencies that may be attributed to the pandemic with a excessive diploma of confidence.

First, the spike in mortgage forbearance and deferral clearly reveals that mortgage lenders and customers had been fast to undertake Congress’ emergency protections that allowed some to delay reimbursement. These protections had been meant to assist customers struggling financially, and with the typical FICO® Rating of mortgage debtors rising, this plan seems to have been profitable so far.

Second, the Fed’s discount in rates of interest seems to have helped stimulate borrowing, because the variety of arduous inquiries for first mortgages confirmed a pointy improve the month the Fed introduced modifications to their benchmark price in contrast with the identical month the prior 12 months.

Credit score and Debt Developments in Altering Instances

Although preliminary debt knowledge reveals promising modifications, it is vital to acknowledge that this knowledge is a snapshot taken throughout a turbulent interval. Moreover, most of those modifications occurred over a interval of lower than a 12 months and are topic to additional change as time goes on.

This evaluation seems to be at the newest (upon date of publication) knowledge from Q3 2020 and compares it with an annual snapshot for 2019 and different years cited. Experian will proceed to observe modifications to client credit score studies and can present updates when notable change happens.

[ad_2]

Source link

{kind=link}