[ad_1]

Charges cross 3% for the primary time since June

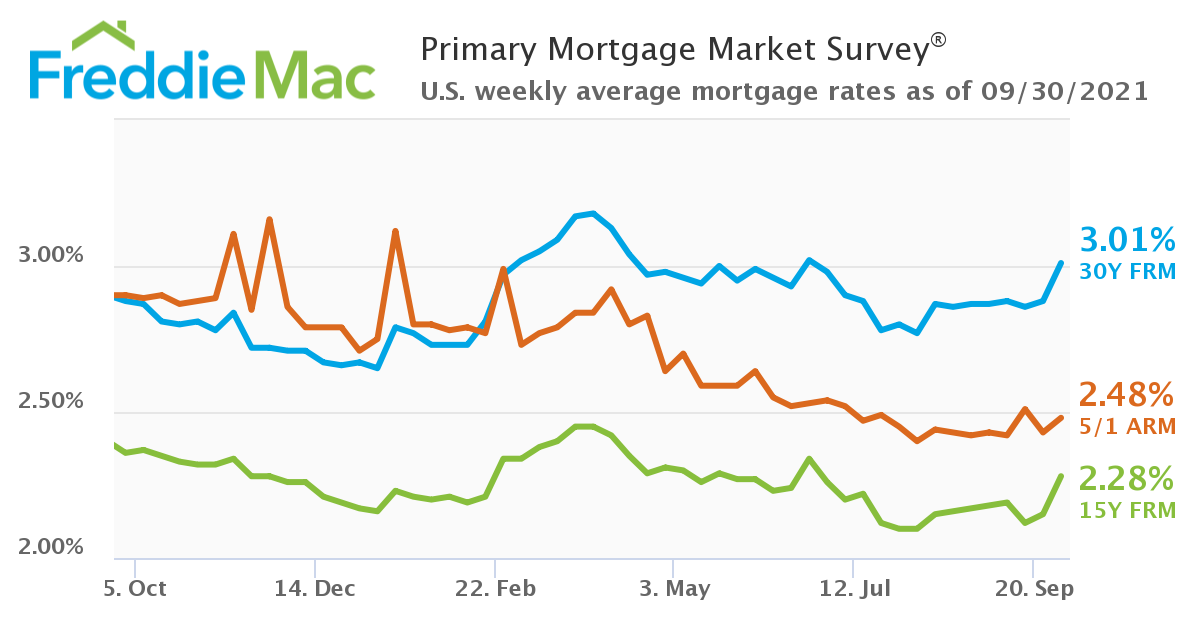

30-year mortgage charges have stayed within the 2% vary by means of almost all of 2021, in line with Freddie Mac.

However this week they spiked above 3% for the primary time since June.

Different charge bumps this yr have been adopted by large drops. However these new, increased charges may very well be right here to remain.

With the financial system enhancing and the Fed pulling back on stimulus soon, there are robust forces driving charges upward.

Debtors who thought record-low charges have been the brand new norm may wish to reevaluate. Immediately’s charges may very well be the bottom we’ll see for some time.

Find your lowest rate before they rise. Start here (Sep 30th, 2021)

Larger charges are right here — to remain?

Most economists and mortgage specialists have been predicting increased rates of interest for the reason that starting of the yr.

With widespread vaccinations, companies and journey reopening, and client confidence on the rise, our financial outlook appeared shiny. And a greater financial system ought to result in increased charges.

We even noticed a false begin in March and April, when charges spiked to three.18% — their highest this yr.

Supply: Freddie Mac

However then the Delta variant struck, and it wasn’t clear how issues would shake out for monetary markets. So charges turned again down.

Now, it appears like we’re lastly seeing these long-awaited ‘increased charges’ begin to materialize.

Why are mortgage charges rising?

There are a pair causes for this week’s enhance in mortgage charges.

The Federal Reserve

First, the Federal Reserve has indicated it can begin pulling again on pandemic-era monetary insurance policies “quickly.” That in all probability means earlier than the top of the yr.

Because the begin of the Covid pandemic, the Fed has been retaining mortgage charges artificially low by injecting billions of {dollars} into the mortgage market every month.

Charges have been at all times going to rise when the Fed stopped this program.

Now the Fed has a clearer roadmap for truly fizzling out its mortgage stimulus. And traders (who ultimately determine mortgage rates) are already pricing in these adjustments. So charges have began going up although the Fed hasn’t formally made a change.

The debt ceiling debate

Second, there’s an more and more scary debate occurring in Congress over the debt ceiling.

“A lot of the rise [in mortgage rates] is because of issues the U.S. will successfully be out of money by October 18 except the debt ceiling is lifted, which was reiterated by each Treasury Secretary Yellen and Fed Chair Powell yesterday,” defined mortgage commentator Rob Chrisman in his September 30 commentary.

If Congress can’t agree to boost this ceiling, the U.S. might default on its debt, which it’s by no means carried out earlier than.

This may seemingly result in no less than a gentle recession in addition to increased rates of interest on mortgages and different types of borrowing.

Find your lowest rate before they rise. Start here (Sep 30th, 2021)

Will charges hold going up?

Earlier charge spikes this yr have been adopted by dramatic falls. However this new enhance may very well be the beginning of an extended upward pattern.

Finally, rates of interest are going up as a result of the financial system is enhancing.

Though Covid isn’t gone — removed from it — we’re all discovering a ‘new regular.’ And it doesn’t seem like we’ll swing again within the different route any time quickly.

As Chrisman mentioned, “Regardless of the challenges that the latest upswing in COVID circumstances presents, it doesn’t seem the COVID fears will create the economy-crushing headwinds they have been on the onset of the pandemic.”

That mentioned, we would see a jagged path upward — with some spikes and a few falls — fairly than a gentle march.

If Congress does discover a answer to the debt ceiling subject, as we’re all hoping they’ll, we might see a brief respite from these charge hikes.

However, general, charges will seemingly hold rising because the financial system strengthens. So debtors mustn’t count on sustained drops within the close to future.

A possible shiny spot for dwelling consumers

Rising charges usually aren’t excellent news for owners. However there could be a silver lining for dwelling consumers if charges do proceed upward.

Freddie Mac’s chief economist Sam Khater explained:

“We count on mortgage charges to proceed to rise modestly which is able to seemingly have an effect on dwelling costs, inflicting them to average barely after rising over the past yr.”

Even a modest decline in dwelling costs may very well be welcome information for consumers combating an uphill battle in right this moment’s red-hot market.

However understand that your charge additionally impacts your property shopping for price range. So should you’re already maxing out the quantity you may borrow, even a minor enhance in charges might probably value you out of the house you need.

Don’t miss the low-rate window

Rates of interest actions might be nearly unattainable to foretell — particularly in right this moment’s weird and ‘unprecedented’ financial system.

Nonetheless, in the intervening time, it appears much more seemingly that charges will proceed upward by means of the top of the yr, fairly than fall again to the two’s and keep there.

Should you’ve been ready on a refinance, or pinning your property shopping for price range on right this moment’s low charges, it’s a great time to get severe about locking a mortgage.

[ad_2]

Source link

{kind=link}