[ad_1]

Final week, the World Well being Group (WHO) designated Omicron, formally often known as B.1.1.529, a variant of concern.

This information rocked monetary markets nationwide amid issues of one other sequence of lockdowns, journey restrictions, and so forth.

Briefly, there’s renewed concern that we’re not out of the woods on COVID, as some appeared to assume previous to this bombshell.

In fact, that is all simply preliminary info, and researchers in South Africa and elsewhere are conducting research to find out if it presents extra dangers to the world.

In case you’re available in the market to purchase a house or refinance your mortgage, you is perhaps questioning what it means for mortgage charges. Let’s talk about.

Mortgage Charges Are inclined to Drop When There Are Unknowns

Whereas mortgage rates and COVID don’t have a long-term relationship, given COVID’s latest emergence, one factor is obvious.

Rates of interest typically transfer decrease when there may be uncertainty within the air, it doesn’t matter what’s behind it.

Previous to this announcement from the WHO, there was a basic perception that we had seen the worst of COVID, and thus the financial system might get again on its merry upward trajectory.

This information has thrown a wrench is that concept, and as such protected havens like Treasuries have rallied.

In the meantime, their yields have plummeted, with the bellwether 10-year bond yield falling about 20 foundation factors (.20%) from round 1.68 to 1.47, earlier than recovering considerably.

It now stands at about 1.52, as buyers digest this Omicron information and attempt to make sense of all of it.

Lengthy-term mortgage charges (e.g. the 30-year fixed) have a tendency to trace the motion of the 10-year bond yield, so they’re now decrease as nicely.

Whether or not they stay low or transfer even decrease within the near-term and past is one other query.

To my level about uncertainty, we don’t actually know something but by hook or by crook. There’s simply new concern and maybe hazard afoot.

WHO famous that it’s unclear if Omicron is extra transmissible, causes extra extreme illness, or circumvents accessible vaccines. However all these unknowns are/had been sufficient to rattle buyers.

Omicron Might Push Mortgage Charges Decrease for Longer

Whereas it is a very new growth, mortgage rates have already moved decrease because of this.

For instance, a 30-year mounted quoted at 3% may now be 2.875% and even 2.75% in the present day, relying on the lender in query.

And charges might proceed to drop if extra unhealthy information is unveiled associated to Omicron. However that’s nonetheless a giant query mark.

Will Omicron be the following Delta pressure, and even worse, or extra innocuous, just like the Mu pressure?

We don’t know, however we do know Israel, Japan, and Morocco have closed their borders to all overseas vacationers, and Australia has delayed its reopening by two weeks.

That is definitely ominous information, and will imply the Omicron variant will likely be lots worse than earlier ones. And extra importantly, really create headwinds for the financial restoration.

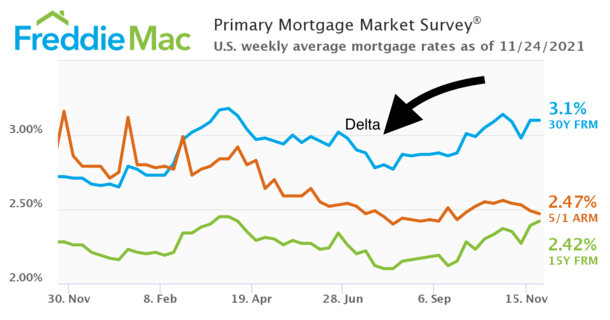

The Delta pressure was declared a variant of concern in mid-June by the CDC, when the 30-year mounted averaged roughly 3%, per Freddie Mac.

Charges yo-yoed a bit after that earlier than drifting to round 2.75% a month later, then started their most up-to-date ascent.

So if Omicron proves to be just like Delta, the 30-year mounted may fall again to those decrease ranges.

However the transfer might show short-lived if it seems to not be as unhealthy as Delta.

In fact, if it’s worse than Delta, and exacerbated by the winter months, it would imply mortgage charges transfer even decrease. And keep decrease for an extended time period.

What to Anticipate for Mortgage Charges in Coming Months

In the end, this new pressure is yet one more reminder that the COVID pandemic isn’t going to vanish anytime quickly. It can take years to play out.

We had been instructed this from the start, so to consider it was going to be enterprise as regular in 2021 was clearly shortsighted.

Whereas the world doesn’t appear like it did a yr in the past, when the financial system was principally shuttered, we’ve got one other doubtlessly lethal winter in entrance of us.

And with the emergence of Omicron, it means there’s an entire lot of uncertainty within the air.

It occurred to return proper after the Fed tapered its purchases of mortgage-backed securities (MBS), with attainable price hikes additionally on the horizon.

That might push this potential price hike additional into the long run, and switch these 2022 mortgage price predictions on their head.

Perhaps we received’t see a 30-year mounted mortgage price method 4% in 2022. Perhaps charges will slide again to their report lows.

Omicron primarily reopens the door to this risk, however doesn’t definitively inform us something simply but. Within the meantime, get pleasure from these tremendous low mortgage charges.

[ad_2]

Source link

{kind=link}