[ad_1]

Podiatrists fly beneath the radar. There are solely about 10,000 podiatrists in the USA proper now, despite the fact that they work on one of many extra necessary and complicated elements of the physique, the toes. However with the excessive price of college, is podiatry value it?

The foot and ankle area of the physique has dozens of bones, tendons, ligaments and muscular tissues. Any accidents to the decrease extremities could cause a series response of issues by way of the hips and again. Frequent foot issues and situations podiatrists handle embrace ingrown toenails, bunions, heel ache, ankle situations like sprains, fractures, inflections, and rather more. The work that podiatrists do is essential to an individual’s total bodily construction and alignment.

Due to the complexity concerned (e.g. analysis, remedy plan, surgical procedure, and so forth.), the time and price to turn into a health care provider of podiatric medication (DPM) is important. The journey to turn into a podiatrist begins with incomes a bachelor’s diploma, adopted by 4 years at a school of podiatric medicine and a three-year residency. There’s additionally the choice to turn into extra specialised by way of fellowship packages. It takes the identical period of time for an MD to turn into an attending doctor. Medical college tuition isn’t low cost. Oftentimes, it’s costlier than most different graduate colleges.

So, is the potential podiatrist wage value it in comparison with the everyday quantity of podiatry college debt? Check out the typical podiatrist wage and scholar mortgage debt. We’ve put collectively a pattern scholar mortgage reimbursement technique to equip you with the data you could determine whether or not the everyday podiatry scholar debt is value pursuing a profession in podiatric medication.

What’s the typical podiatrist wage?

Let’s study a couple of completely different sources to see how a lot podiatrists make as a result of it’s exhausting to discover a constant reply.

The Bureau of Labor Statistics, for instance, reveals that the mean salary for podiatrists is $151,110 after finishing their residency. Wage.com reveals a median salary of $211,401, whereas ZipRecruiter says the average podiatrist salary is $130,496, and Certainly says the average salary for podiatrists is $127,796.

The Bureau of Labor Statistics info consists of probably the most complete knowledge on virtually all 10,000 podiatrists on the market. The opposite websites have advantage, although, as a result of that’s the place employers are promoting jobs. That’s the info employers and candidates are contemplating in wage negotiations. These websites’ numbers may present extra risky swings based mostly upon {the marketplace} from week to week. Whereas the BLS may be extra regular.

Podiatrist salaries differ broadly by metropolis and state

Sticking with the BLS knowledge, the typical wage of the 30 DPMs within the Youngstown-Warren-Boardman, OH-PA space is $229,330. Compared, the 110 podiatrists within the Tampa, FL space earn about $185,040 every.

Maine ($214,960), Nebraska ($206,050), New Hampshire ($192,130),Oklahoma ($187,420) and North Carolina ($186,100) are the highest 5 highest paying states for podiatrists.

So far as the bottom paying states, Kentucky ($109,710) and Rhode Island ($112,070) are the worst paying. California is close to the underside, too ($123,130).

There’s an excessive amount of fluctuation by yr, too. A Forbes article reveals the fluctuation in podiatrist salaries from 2013 to 2018. Podiatrist earnings dropped by 30% in Connecticut and 29% in Oregon. Rhode Island and Iowa had been among the many largest will increase at 106% and 30%, respectively. Observe that Rhode Island discovered itself on the prime of the very best paying listing for the Forbes article, but it’s now on the backside based mostly on the newest BLS knowledge.

For podiatrists, location does matter. It’s about $130,000 from prime to backside between completely different states. Simply understand that salaries can fluctuate fairly a bit.

Common podiatrist scholar debt is excessive

Podiatrists undergo intensive coaching, and podiatry college is likely one of the costlier medical colleges on the market.

Kent State University College of Podiatric Medicine’s tuition, for instance, is projected to price about $80,000 per yr for 4 years. The common DPM from Western University of Health Sciences graduates with $241,833 in debt.

At Pupil Mortgage Planner®, the typical podiatrist we’ve labored with has $295,000 in scholar loans. That scholar mortgage steadiness is among the many highest for the graduate-level professionals we work with.

So, what’s the easiest way for podiatrists to pay again these podiatry scholar loans and make it value it?

Sensible scholar mortgage reimbursement methods for podiatrists

We’ve labored with over 5,875 particular person shoppers throughout all completely different professions advising on $1.44 billion in scholar loans. Beginning with the the larger image, we’ve discovered there are two optimum methods to pay again scholar loans:

1. Aggressive reimbursement: The technique right here is to do every thing you possibly can to repay debt as quick as doable. This plan ought to take not more than 10 years. You need to pay as little in curiosity as doable, so it typically means refinancing to pay less in interest and put extra money towards paying off the mortgage.

This technique works finest for podiatrists who owe lower than 1.5 instances their earnings in scholar debt. For instance, a podiatrist who makes $150,000 and owes $225,000 or much less in debt.

2. Use an income-driven reimbursement (IDR) plan to maximise mortgage forgiveness: This technique entails signing up for PAYE, REPAYE or IBR to maintain the month-to-month funds as little as doable. Then, benefit from the low funds to save lots of aggressively, ideally by maxing out pre-tax retirement contributions and by saving up for the potential tax bomb you may need to pay on forgiven scholar mortgage debt.

This technique works finest for podiatrists who owe greater than twice their earnings in scholar loans. For instance, a podiatrist who makes $150,000 and owes $300,000 or extra in scholar loans.

When podiatrists ought to refinance scholar loans

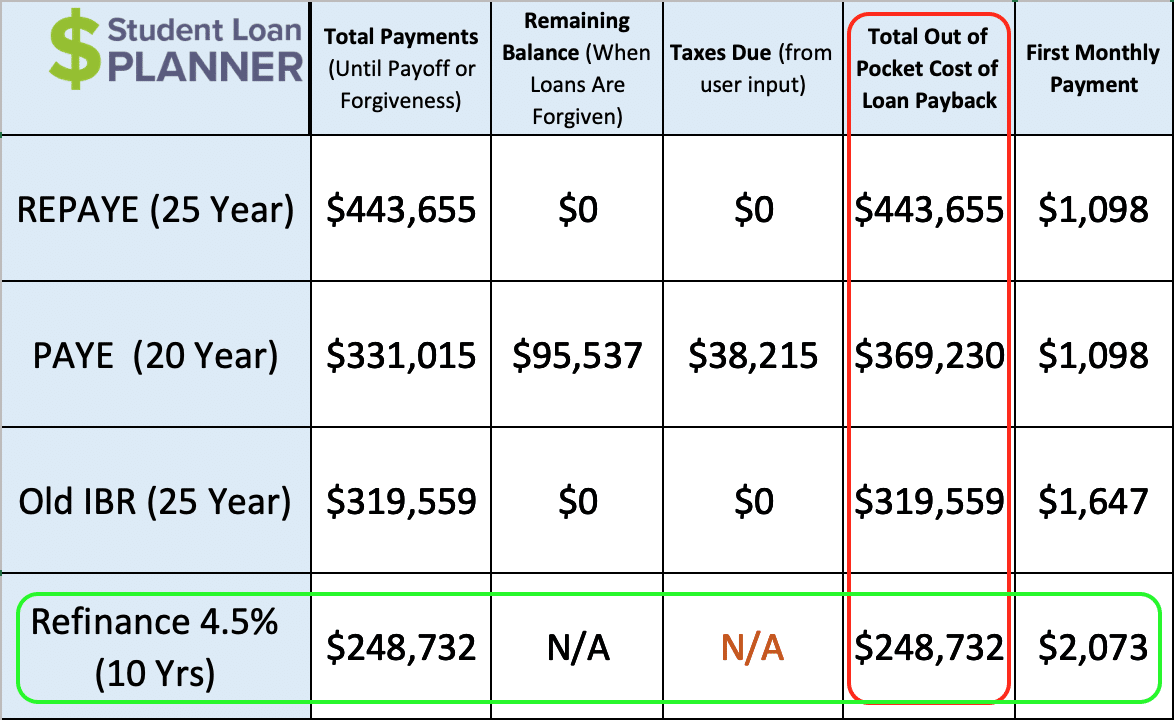

Let’s have a look at a hypothetical instance for example reimbursement choices: Jason has $200,000 at 6.8% in scholar debt with a podiatrist wage of $150,000. His earnings is projected to develop gradual and regular at 3% per yr. Ought to he take the aggressive method or go on income-driven reimbursement to make the price of podiatry value it?

Let’s examine the numbers for IDR versus refinancing:

This can be a clear refinancing case as a result of refinancing will save Jason probably the most cash in comparison with the opposite two choices.

REPAYE and IBR are out of the working. His earnings is excessive in comparison with his loans, which implies that his funds can be excessive sufficient to repay the loans in full earlier than attending to any mortgage forgiveness. Extra particularly, he’d find yourself paying off a 6.8% mortgage over an extended time frame when he might have paid off a 4.5% mortgage extra aggressively.

PAYE is projecting to supply some mortgage forgiveness in the long run however not almost sufficient. Even with that forgiveness, it could price about $111,000 extra to pay again his scholar debt and double the period of time till he’s debt free (20 years versus 10 years).

The refi funds are $1,000 greater monthly versus his preliminary PAYE cost. However he can possible afford that on a $150,000 earnings. It’s value it to save lots of six-figures over the long term.

Why refinance with a private lender relatively than depart it on the 10-year normal plan? Refinancing might decrease his rate of interest from 6.8% right down to 4.5%, lowering the overall price of paying again his debt. His month-to-month cost could be decrease by about $300 monthly and he’d save almost $35,000 over 10 years. Refinancing to save lots of $30,000 could be value it.

When podiatrists ought to get on an IDR plan

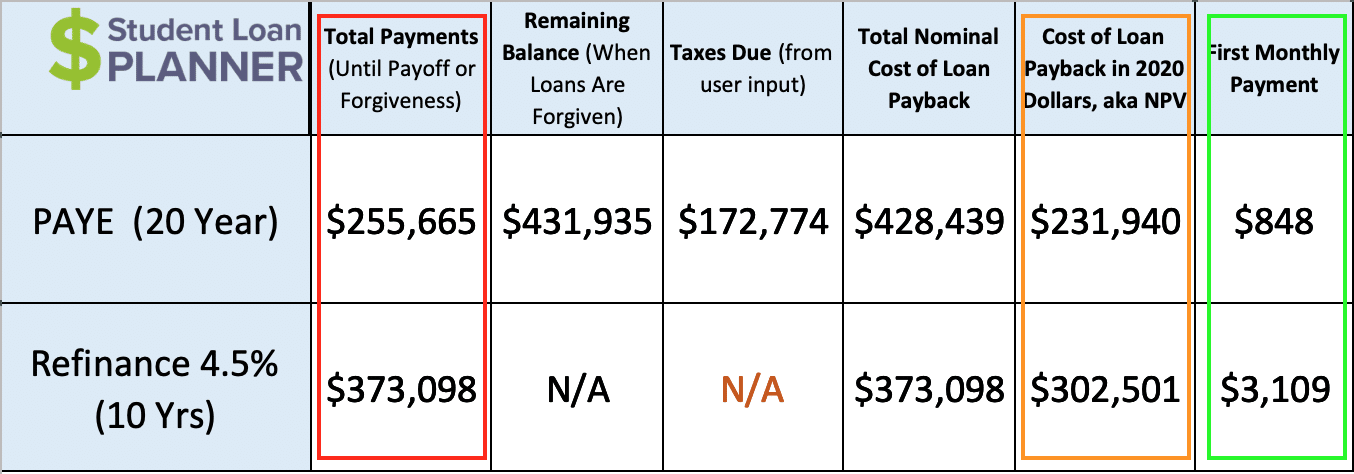

Let’s have a look at a distinct instance involving IDR: Rebecca is a podiatrist who lives in Southern California. Her earnings is $120,000, and he or she owes $300,000 in scholar debt from undergrad and podiatry college. Her earnings ought to develop on the regular price of three% per yr.

Though it appears to be like like refinancing prices much less out of pocket, it isn’t really probably the most reasonably priced or optimum plan. These funds of $3,109 monthly could be crushing on her wage.

Mathematically talking, you need to go together with the choice that has the bottom internet current worth (NPV), or the fee in right this moment’s {dollars}. Taking a look at it there, PAYE is almost $70,000 lower than refinancing. Primarily, this implies it’s cheaper to maintain the funds low so she will be able to save loads cash.

Right here’s what I imply by the decrease NPV being extra necessary than the overall price:

The mixture of a excessive refinance cost ($3,109/month) and a decrease wage doesn’t depart a lot room to succeed in different monetary targets, like shopping for a home or saving for retirement.

Her way of life could be just about nil as nicely. Let’s say her take-home pay is about $7,500 monthly. Greater than 40% would go towards her refinancing funds over the subsequent 10 years. This leaves her with simply over $4,000 for normal month-to-month outflows whereas residing in costly Southern California. That’s just about a no-go.

On PAYE, nonetheless, her cost would begin at $848, which would go away her with about $6,500 monthly in take-home pay. Now we’re speaking.

Bear in mind, although, that you could save aggressively whereas on a PAYE plan. If Rebecca might save about $2,000 a month by maxing out her pre-tax retirement plan whereas additionally saving for the mortgage forgiveness tax bomb ($500/month), she might attain different monetary milestones alongside the way in which. By sticking with this technique persistently, she could possibly be debt free, pay the tax bomb and nonetheless have a $500,000 nest egg in 20 years.

Is podiatry college value it?

Whether or not or not a podiatry diploma is value it’s a combined bag. A podiatrist’s beginning wage and the promise of a doubtlessly fulfilling profession could be enticing. Nevertheless it’s scary to owe $300,000 in scholar loans.

This profession path won’t be value it financially for many who are planning to maneuver to a decrease compensating space of the nation. They’d even be a lot additional forward financially in the event that they didn’t have $300,000 in scholar loans, even when they’re utilizing an income-driven reimbursement plan to optimize their mortgage reimbursement.

However, podiatry could possibly be very financially rewarding for many who arrange a apply in a better compensating space just like the higher Midwest. They might earn sufficient cash to take the aggressive method to scholar mortgage reimbursement. They’d be debt free in 10 years or much less and have the remainder of their profession to deal with saving aggressively with a excessive earnings.

The excellent news is that it doesn’t matter what state of affairs a podiatrist is in, there’s an optimum plan to pay again the price of the diploma and make podiatry college value it, whether or not you’re in a state of affairs the place it makes extra sense to refinance your medical college loans or get on a PAYE plan and aggressively save.

If being a podiatrist is one thing you really need, regardless of the doubtless excessive scholar mortgage debt, then it’s completely crucial to make way of life sacrifices early in your profession so it can save you aggressively to succeed in monetary independence.

Easy methods to maximize a podiatrist’s wage and repay debt

Podiatrists can discover a clear path to pay again their scholar loans utilizing actionable steps that save them cash. Pupil Mortgage Planner® might help you determine which reimbursement technique is best for you in only one hour. Plus, we additionally embrace e-mail help after the session to reply follow-up questions and enable you to implement your plan. Learn more about our consultation process.

In case you have a clear-cut refinancing case, there’s no must get a session. However I’d recommend applying for a refinance loan using our cash-back link. You could possibly reduce your rate of interest and get probably the most reasonably priced phrases on your state of affairs plus get a couple of hundred bucks money.

I work with debtors who owe greater than $200,000 in scholar loans, which features a bunch of podiatrists, so be happy to e-mail me at [email protected] when you have any questions on this text. Our group of specialists might help anybody, so select the guide you assume could be best for you based mostly in your particular person circumstances and get began.

[ad_2]

Source link

{kind=link}