[ad_1]

Who has one of the best mortgage charges?

If you need to discover one of the best mortgage charge, it helps to know the place to start out wanting.

We analyzed information from the 40 largest lenders in 2020, in search of the bottom rates of interest and charges.1

These lenders topped the listing for greatest 30-year mortgage charges:

- Freedom Mortgage

- Higher Mortgage

- Citibank

- Guild Mortgage Firm

- American Monetary Community

Bear in mind, charges range so much from individual to individual.

Your personal charge relies on components like your down fee and mortgage time period — so there’s likelihood your greatest charge will come from an organization not listed above.

Fortunately, charges are at historic lows proper now. It’s time to buy your greatest supply.

Find and lock a low mortgage rate (Jun 10th, 2021)

On this article (Skip to…)

How one can discover your lowest mortgage charge

Mortgage charges are extremely private. Elements like your credit score rating and debt-to-income ratio may have a huge impact on the speed you get.

Which means the corporate with the bottom common charges gained’t all the time be the most cost effective lender for everybody.

For instance: Among the many 40 mortgage lenders in our research, Freedom Mortgage had the bottom common mortgage charge in 2020, at simply 2.92% for a 30-year mortgage.

However common charges inform solely a part of the story. Total, Freedom Mortgage charges ranged from below 2% to over 6%. So some folks acquired a lot decrease charges than others.

To seek out your greatest supply, you need to request Mortgage Estimates from a couple of firm and examine.

Check your mortgage rates (Jun 10th, 2021)

Greatest mortgage charges from prime lenders

We appeared on the 40 largest mortgage lenders in 2020 to see how their rates of interest stacked up.

The 25 firms with one of the best mortgage charges on common are as follows:

| Mortgage Lender | Common 30-12 months Curiosity Price, 20202 |

| Freedom Mortgage | 2.92% |

| Higher Mortgage | 3.03% |

| Citibank | 3.05% |

| Guild Mortgage Co. | 3.15% |

| American Monetary Community | 3.16% |

| loanDepot | 3.17% |

| Assured Price | 3.17% |

| CrossCountry Mortgage | 3.17% |

| Prosperity Dwelling Mortgage | 3.17% |

| Homepoint | 3.18% |

| New American Funding | 3.18% |

| Financial institution of America | 3.19% |

| Quicken Loans (Rocket Mortgage) | 3.20% |

| Supreme Lending | 3.20% |

| American Pacific | 3.21% |

| Major Residential Mortgage | 3.21% |

| Gateway Mortgage Group | 3.22% |

| Stearns Lending | 3.23% |

| Motion Mortgage | 3.24% |

| Academy Mortgage Corp. | 3.24% |

| Caliber Dwelling Loans | 3.25% |

| Paramount Residential Mortgage Group | 3.25% |

| Finance of America | 3.26% |

| LendUS | 3.26% |

| Residents Financial institution | 3.27% |

Word that common charges proven on this desk are from 2020, when charges had been close to report lows almost all 12 months. At present’s mortgage charges may very well be increased than what’s proven.

You may nonetheless use final 12 months’s rates of interest as a instrument to match lenders aspect by aspect and see how they rank.

However earlier than you lock in a mortgage, you’ll need to get customized rates of interest from a number of completely different lenders to ensure you’re getting greatest charge obtainable right now.

Which mortgage lender has the bottom closing prices?

Closing costs are round 2-5% of the mortgage quantity on common. That’s over $4,000 on a $200,000 mortgage — a substantial amount of money.

Identical to mortgage charges, you may store round for the bottom closing prices to attenuate your out-of-pocket charges.

Right here’s how the highest mortgage lenders examine for whole mortgage prices, in line with 2020 information from HMDA.

| Mortgage Lender | Common Complete Mortgage Prices, 2020 (as % of Common Mortgage Quantity) 2 |

Instance: Upfront Prices for a $250,000 Mortgage |

| Supreme Lending | 0.64% | $1,612 |

| Citibank | 0.83% | $2,070 |

| PNC | 0.90% | $2,248 |

| Chase | 0.99% | $2,470 |

| Higher Mortgage | 1.04% | $2,612 |

| Wells Fargo | 1.20% | $2,992 |

| Gateway Mortgage Group | 1.26% | $3,153 |

| Assured Price | 1.35% | $3,371 |

| Financial institution of America | 1.40% | $3,504 |

| Flagstar Financial institution | 1.41% | $3,531 |

| Prosperity Dwelling Mortgage, LLC | 1.47% | $3,680 |

| LendUS LLC | 1.52% | $3,789 |

| Homepoint | 1.53% | $3,835 |

| loanDepot | 1.54% | $3,855 |

| Freedom Mortgage | 1.55% | $3,876 |

| Northpointe Financial institution | 1.56% | $3,892 |

| Finance of America | 1.56% | $3,902 |

| US Financial institution | 1.64% | $4,102 |

| Residents Financial institution | 1.64% | $4,103 |

| Sierra Pacific Mortgage | 1.65% | $4,114 |

| American Pacific | 1.68% | $4,201 |

| Fairway Unbiased | 1.75% | $4,369 |

| Bay Fairness LLC | 1.75% | $4,377 |

| Caliber Dwelling Loans | 1.75% | $4,382 |

| Motion Mortgage | 1.79% | $4,481 |

If you’re procuring, word that some closing prices can’t be negotiated as a result of they’re set by third events (like appraisal and credit score reporting charges).

However lenders do have wiggle room in relation to setting their very own charges. So if you happen to get a number of affords, you may need some leverage to barter your prices down.

Some homebuyers even get the seller to cover some or all of their closing prices. However that’s not a assure, so it’s best to nonetheless plan forward for these bills.

Compare loan offers from top lenders (Jun 10th, 2021)

What’s extra necessary: A low mortgage charge or low charges?

It’s simply as necessary to match upfront mortgage prices as it’s to match mortgage charges.

Your rate of interest may appear way more necessary as a result of it’s with you for the lifetime of the mortgage. However upfront charges could make an enormous distinction — particularly if you happen to’ll solely be in the home a number of years.

Keep in mind that most individuals who get a 30-year mortgage don’t maintain their mortgage the complete 30 years. The truth is, householders maintain 30-year loans for simply 7 years on common.

If you’re solely paying curiosity over a brief interval, these upfront charges begin to carry extra weight in comparison with your rate of interest.

Lenders may emphasize both low closing prices or low charges to make a proposal look extra engaging, whereas elevating the opposite quantity.

As well as, lenders will typically emphasize one quantity or the opposite to make a proposal look extra engaging than it’s.

As an illustration, lenders may promote low- or no-fee mortgages, saying they’ll cowl the upfront prices for you. However these loans sometimes have the next rate of interest.

Different lenders may emphasize ultra-low rates of interest however cost increased origination charges to make up for it.

So whenever you’re looking for a mortgage, learn your charge quotes completely. Have a look at charges, upfront charges, and your whole estimated closing prices to ensure you’re getting one of the best deal total.

Find your lowest mortgage rate (Jun 10th, 2021)

How to buy mortgage charges

Looking for one of the best mortgage charge — and the bottom charges — is straightforward sufficient if you recognize what you’re doing. There are 5 fundamental steps:

- Work in your credit score and price range to get the absolute best supply

- Determine which type of mortgage loan you want

- Discover lenders providing the kind of mortgage you’re in search of

- Choose your most well-liked lenders based mostly on marketed charges, suggestions, buyer opinions, and expert reviews

- Request Loan Estimates (“quotes”) from these lenders and examine the charges and charges in every supply

That final step — evaluating Mortgage Estimates — is essential to discovering one of the best mortgage charge and most inexpensive mortgage total.

How one can learn your Mortgage Estimates

A Mortgage Estimate (LE) is a regular doc you’ll obtain after finishing a mortgage software with any lender.

The LE lists every little thing you could learn about a mortgage earlier than signing on, together with the rate of interest, lender costs, mortgage size, compensation phrases, and extra.

By evaluating a number of Mortgage Estimates aspect by aspect, you may inform immediately which lender is providing you essentially the most inexpensive house mortgage.

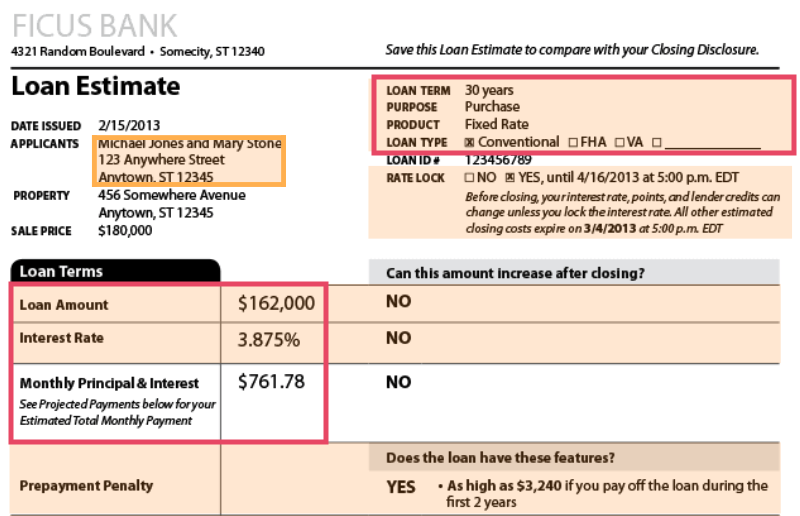

Pattern mortgage estimate, Web page 1. Picture: CFPB

The primary web page of the Mortgage Estimate (proven above) clearly states your mortgage rate of interest and projected month-to-month fee.

These are the numbers folks usually pay most consideration to when looking for house loans.

However the rate of interest isn’t the one half value .

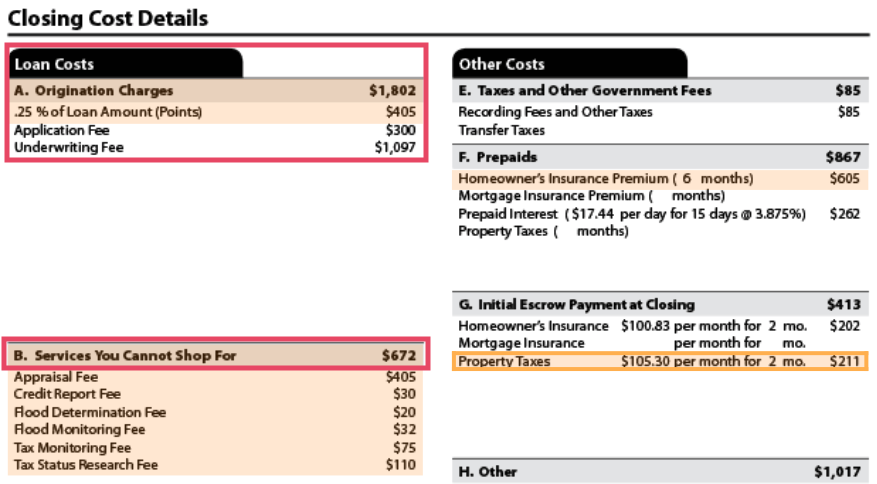

You must also examine the estimated closing prices with every lender, in addition to the closing price breakdown proven on web page two.

Pattern mortgage estimate, Web page 2. Picture: CFPB

Discovering one of the best charge and charge combo

On the finish of the day, one of the best mortgage charge alone doesn’t make for one of the best supply.

Your rate of interest and shutting prices each must be factored in. Their relative weight will rely in your monetary targets and the way lengthy you intend to remain in the home.

As an illustration, if you happen to’re solely going to personal the house a number of years, the next charge however decrease upfront prices may make sense.

However if you happen to’ll keep the complete 30-year period of the mortgage, you possible need the bottom rate of interest potential. In that case, you may settle for barely increased upfront prices for a decrease charge.

your annual percentage rate (APR) can usually make it easier to examine the whole price of a mortgage as a result of APR contains curiosity and mortgage charges.

Find your lowest mortgage rate (Jun 10th, 2021)

Tricks to get the bottom mortgage charge

In order for you the bottom mortgage charge obtainable, you need to store round. That’s the primary rule.

However there are different methods you need to use to get decrease affords from the lenders you discuss to.

- Attempt for a last-minute credit score enhance. See what you are able to do to improve your credit before you purchase or refinance. Your credit score rating makes an enormous distinction in your mortgage charge, and bettering it only a few factors may result in actual financial savings

- Contemplate low cost factors. In case you can afford it, you may pay extra upfront for a greater mortgage charge over the lifetime of the mortgage. This may very well be sensible if you happen to plan to maintain your own home a very long time. Discount points price 1% of the mortgage quantity, and sometimes decrease your charge by 0.25%

- Negotiate your charge. Negotiating with a lender may sound intimidating, however belief us once we say it may be achieved. Mortgage lenders have flexibility with the charges they provide, they usually need what you are promoting. A decrease rate of interest from a special firm could be the one leverage you could negotiate a better offer with the lender you need

- Negotiate your closing prices. Some closing prices are non-negotiable, just like the third-party appraisal and credit score reporting charges. However the charges your lender costs can sometimes be negotiated to save lots of you cash on the entrance finish

- Know when to lock your charge. Mortgage charges transfer up and down on daily basis. If you wish to get the bottom potential charge, control daily rate movements and be prepared for a charge lock once they fall

Getting mortgage quotes may not be essentially the most pleasant method to spend a day. However a number of hours of effort may prevent hundreds in the long term.

One study discovered that individuals who examine simply 3 lenders save $300 per 12 months on common. And if you happen to’re a savvy shopper, you could possibly save much more.

Does my down fee have an effect on my charge?

An even bigger down fee will help you qualify for low mortgage charges.

As an illustration, standard loans solely require 3% down. However if you happen to’re in a position to put down 20%, you’ll get a greater charge and keep away from non-public mortgage insurance coverage (PMI). So your mortgage will price so much much less total.

For presidency mortgage packages — like FHA, VA, and USDA loans — your down fee quantity gained’t have as massive of an affect in your charge.

Although an enormous down fee can decrease your mortgage charge, it doesn’t always make sense to save lots of for a 20% down fee.

Tying up most of your financial savings in your house can put you in a decent spot if emergency bills come up. It may additionally go away new house patrons brief on money for repairs and residential enchancment initiatives which are certain to come back up.

Oftentimes, it is sensible to make a smaller down fee and take the next charge and/or mortgage insurance coverage. This places you in a home and allows you to begin constructing fairness sooner.

Then, you could possibly probably refinance to a decrease charge and no mortgage insurance coverage a number of years down the road.

Verify your home buying eligibility (Jun 10th, 2021)

Different components that affect your mortgage charges

There are many completely different variables that have an effect on the mortgage charges you’re supplied.

You’ll have little to no management over a few of these components. For instance, no person anticipated a coronavirus pandemic would drive down mortgage charges in 2020.

In different years, financial forces push the Federal Reserve to boost borrowing charges.

And though the Fed doesn’t control mortgage interest, banks and credit score unions supply mortgage and refinance charges that mirror the broader curiosity market.

As a result of you may’t management every little thing, it’s necessary to know what components you can change when making use of for a mortgage. These embrace issues like:

- Your credit score rating and report: Credit score restore takes time, however each level in your credit score rating will help. If potential, pay down your bank cards to about 30% of their credit score limits earlier than making use of for a brand new house mortgage. Debtors with glorious credit score get one of the best charges

- Your debt-to-income ratio: Lenders test how a lot you owe in different month-to-month funds in comparison with your revenue to seek out out a lot a brand new house mortgage would affect your price range. A debt-to-income ratio above 45% may give lenders trigger for concern. Repay a pair current loans, if potential, to enhance your debt-to-income ratio

- Your mortgage time period: Shorter-term loans like a 15-year mortgage have a tendency to supply decrease charges than 30-year mortgages

- Your charge kind: Adjustable-rate mortgages promote decrease charges than fixed-rate mortgages. However when the introductory ARM charge expires, your rate of interest and month-to-month funds may improve

- Your house’s worth: Figuring out your worth vary will maintain your debt-to-income ratio on observe and open up extra kinds of mortgages — particularly for first-time house patrons. Use a mortgage calculator to experiment with completely different mortgage quantities to seek out your worth vary

- Your down fee or fairness: When shopping for a house, a much bigger down fee quantity can earn you a decrease rate of interest. With a mortgage refinance, the quantity of house fairness you’ve constructed up may affect your charge

In case you can enhance your monetary scenario in all or most of those areas, you’ll have entry to among the lowest-rate loans in the marketplace.

Your month-to-month mortgage fee: Greater than an rate of interest

Dwelling buyers usually assume when it comes to rates of interest when looking for a house mortgage. However curiosity is just one piece of the puzzle.

Your total mortgage payment may even embrace the next prices:

- Property taxes: Cities and counties levy property taxes annually. Dwelling patrons usually break these annual funds down into 12 month-to-month installments

- Owners insurance coverage: This annual expense can be prorated and added to your month-to-month fee

- PMI or MIP: Until you set 20% down on a traditional mortgage, you’ll want so as to add mortgage insurance coverage onto your month-to-month funds. That may very well be non-public mortgage insurance coverage (for a traditional mortgage) or mortgage insurance coverage premium (for an FHA mortgage). Mortgage insurance coverage usually provides round 1% of your mortgage stability to your funds annually

In case you stay in a apartment or deliberate unit growth, you’ll even be accountable for HOA dues every month.

As you calculate how a lot house you may afford, make sure to add in these further prices so that you’re budgeting precisely.

Mortgage rates of interest by mortgage kind

Various kinds of mortgage loans have completely different rates of interest.

To decide on the proper mortgage kind for you, you’ll have to consider your credit score, down fee, house worth, and site.

- FHA loans: The Federal Housing Administration requires a credit score rating of 580 and at the very least 3.5% down for an FHA mortgage. FHA rates of interest are usually low, however mortgage insurance coverage premiums improve your month-to-month fee

- USDA loans: The U.S. Division of Agriculture backs mortgage loans for low- and moderate-income debtors in rural areas. No down fee is required, credit score necessities often begin at 640, and USDA rates of interest are sometimes under market

- VA loans: Many navy members and veterans can qualify for a VA mortgage backed by the Division of Veterans Affairs. VA loans supply no down fee with no PMI required, and these mortgages often have the bottom charges in the marketplace

- Typical loans: With a conforming or standard mortgage, your rate of interest is straight tied to your credit score rating and down fee. Solely a 620 FICO rating and three% down are required, however debtors with 20% down and a rating over 720 get one of the best mortgage charges

- Jumbo loans: You’ll want a jumbo mortgage to purchase a high-value property. These loans exceed standard mortgage limits and often require 10-20% down (although some lenders will go as little as 5%). Jumbo mortgage rates of interest are sometimes just like standard mortgage charges for debtors with good credit score

Not all lenders supply a full vary of mortgage choices. And never each mortgage kind works for all properties. For instance, you may’t use an FHA mortgage or a VA mortgage to purchase a trip house or rental property.

In case you’re undecided which mortgage will work greatest for you, discuss with a mortgage officer or mortgage dealer about your choices.

Together with mortgage charges, ask about what you’re prone to qualify for in addition to the short- and long-term prices of every mortgage kind.

What are present mortgage charges?

Present mortgage charges are nonetheless at historic lows, creating nice offers for house patrons and refinancing householders.

Evaluating mortgage affords from a wide range of lenders is essential to discovering your greatest charge. However charge procuring is only one a part of the house shopping for course of.

Getting the proper mortgage kind — and saving cash on closing prices and different charges — will help you decrease your total borrowing prices.

Be sure you take a look at charges, mortgage phrases, and long-term borrowing prices in addition to rates of interest whenever you’re mortgage procuring. That’s the surest method to save cash in your new house mortgage.

Verify your new rate (Jun 10th, 2021)

1High 40 lenders for 2020 sourced from S&P Global, HousingWire, and Scotsman Guide.

2Price and charge information had been sourced from self-reported mortgage information that each one mortgage lenders are required to file annually below the Dwelling Mortgage Disclosure Act. Averages embrace all 30-year loans reported by every lender for the earlier 12 months. Your personal charge and mortgage prices will range.

[ad_2]

Source link

{kind=link}