[ad_1]

Lately, home equity is booming due to quickly appreciating property values.

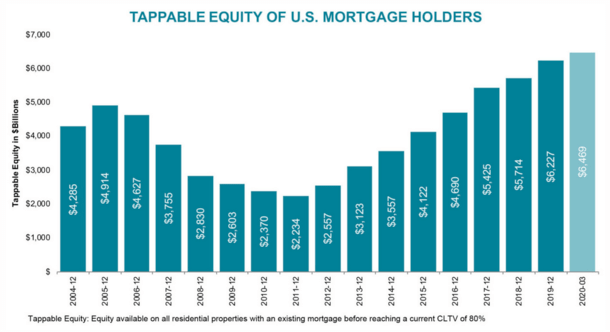

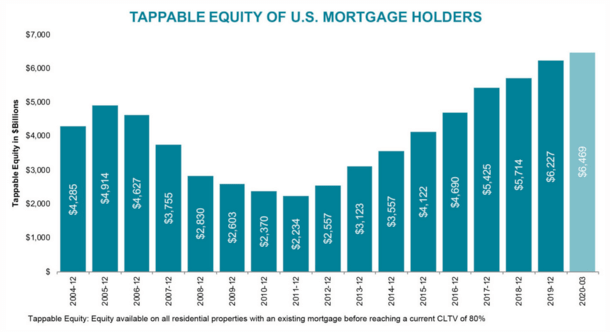

Ultimately look, whole fairness on mortgaged properties exceeded $10 trillion, with greater than $6.5 trillion of it tappable, per current figures from Black Knight.

Sure, that’s a “T” not a “B.” However you’ll of by no means guessed it lower than a decade in the past after the housing bubble burst and put thousands and thousands in underwater positions.

Within the early 2000s, it was all about tapping into your own home fairness with a line of credit or a cash-out refinance, typically at absurdly excessive loan-to-value ratios (equivalent to 100%).

The entire utilizing your own home as an ATM factor to make lavish purchases and even simply pay the payments every month grew to become the norm.

Because of all that extra, the narrative shortly modified to overpriced properties, declining fairness, damaging fairness, underwater mortgages, mortgage modification applications, foreclosures, and so forth.

Humorous how that works…

This reversal of literal fortune was attributable to crashing dwelling costs and zero down mortgages, lots of which weren’t correctly underwritten to start with.

Most of those that obtained into bother bought properties on the top of the market at unsustainable costs, whereas on the similar time counting on 100% financing to get the deal achieved.

This triggered a number of owners to go away or take into consideration strolling away, as home price deprecation was found to be the leading driver of default.

However lots of those that caught round and rode it out are literally in nice form, possibly even higher positions than once they first took out their mortgages.

In reality, those that held on, even when they bought a house in 2006, might be up 50% right now due to the current increase.

Nonetheless, others are nonetheless feeling the damaging results of the housing disaster, even after a number of years of double-digit dwelling value positive aspects.

For those who’re a kind of owners, and even in the event you’re not, you might be questioning the best way to construct some dwelling fairness.

That method, when it comes time to promote your own home (or refinance your mortgage), you are able to do so with out fear.

These with extra dwelling fairness will stroll away with additional cash of their pocket, and if refinancing, might be able to qualify for a decrease rate of interest.

Let’s have a look at the numerous methods you may construct fairness in your house:

1. Rising dwelling costs – Right here’s a straightforward one which requires no effort in your half.

When property values climb larger, you’ll achieve fairness just because your own home or apartment will likely be price extra. It’s so simple as that.

For instance, if your own home was price $200,000, after which rose to $250,000 after 5 years, you’d have $50,000 extra fairness.

That is the great thing about homeownership, and one of many many advantages of owning a home versus renting.

In reality, the latest Survey of Shopper Funds (SCF) from the Federal Reserve revealed that owners had a internet price of $255,000 versus simply $6,000 for renters. Numerous that may be attributed to dwelling fairness.

After all, the alternative may also happen if dwelling costs drop, as all of us now know. However in the intervening time, every thing seems to be on the up and up.

2. Falling mortgage stability – Right here’s extra low-hanging fruit. As you repay your mortgage every month, you pay a portion of curiosity and a portion of principal (assuming it’s not an interest-only home loan).

Any principal funds made will increase your fairness as your own home mortgage will get paid down.

For instance, you’d achieve $343 in principal through the first month on a 30-year fastened with a $200,000 mortgage quantity set at 3%.

After a 12 months, that’s about $4,000. And after 5 years, greater than $22,000!

Each time you make your mortgage cost, you’ll achieve some dwelling fairness. And when mixed with an appreciation, it may be a strong one-two punch.

3. Bigger mortgage funds – This one requires more cash out of your pocket, however can prevent cash on the similar time.

For those who make bigger funds every month, with the additional portion going towards principal, you’ll pay off your mortgage much faster and achieve dwelling fairness lots faster. Easy and efficient.

Whereas it would value you extra initially, you’ll pay lots much less curiosity over time.

For instance, your whole curiosity expense would fall from $104,000 to $59,000 in the event you paid simply $200 additional every month, and your mortgage could be paid off practically a decade early.

4. Biweekly mortgage funds – Right here’s one other strategy to save on curiosity with little or no effort.

You’ll be able to go along with a biweekly mortgage payment plan, the place you make 26 half funds all year long, which equates to 13 month-to-month funds.

This may shave down your mortgage time period, prevent a ton in curiosity, and aid you construct dwelling fairness lots sooner.

There’s additionally a easy method to do that with out having to join a program which will value cash the place you simply add 1/12 to every month-to-month cost.

5. Shorter mortgage term – For those who’ve obtained the means, and need to extinguish your own home mortgage earlier, assume past the 30-year fastened.

It’s potential to refinance right into a shorter-term mortgage with a decrease mortgage rate, equivalent to a 15-year fixed, which can enhance the dimensions of your funds, however construct fairness at a a lot larger price than a standard 30-year mortgage.

You may also be capable of decide one thing in between, like a 20- or 25-year fastened, and even one thing that matches your unique time period, like a 22-year mortgage time period.

This may maintain you on monitor, and even forward of schedule, and likewise aid you keep away from resetting the clock.

6. Keep away from refinancing – Conversely, in the event you don’t refinance and pull money out, you’ll retain all of the fairness in your house.

Throughout the prior housing increase, scores of householders refinanced their loans again and again till they sucked their fairness dry.

This was truly one of many the reason why many selected to stroll away, or had been compelled to promote quick or foreclose.

Had they only paid down their loans over time, most would of been in fairly good condition.

Merely put, it’s superb to faucet fairness, however like every thing else, moderation is vital.

7. Dwelling enhancements – Right here’s a possible win-win which you can truly get pleasure from.

For those who make sensible home improvements, the place the anticipated worth exceeds the associated fee, you’ll enhance your own home fairness by proudly owning a house that’s price extra.

Whereas it’s seemingly the identical precise home, sensible dwelling units, quartz counter tops, and chrome steel home equipment nonetheless draw consumers in, and also you may be capable of promote for extra.

You’ll be able to even do it without spending a dime if it’s your personal sweat fairness. And within the meantime, you get to get pleasure from a greater home.

8. Upkeep – Now let’s discuss being a accountable house owner.

Hold your own home in tip-top form and you can be rewarded when it comes time to promote.

For those who can unload it for extra on account of correct upkeep, you’ve basically created extra fairness in your house.

Dwelling consumers typically hit sellers with expensive restore requests, nevertheless it’ll be harder for them to ask for concessions in the event you took nice care of your own home.

It may even be prudent to get a house inspection your self, earlier than you promote, to handle any crimson flags earlier than a purchaser tries to get you to pay for them.

9. Curb attraction – That is considered one of my favorites and one thing anybody can do to spice up their dwelling worth, and due to this fact fairness if promoting.

I’m referring to curb attraction and likewise dwelling staging. Make your own home look good if you record it and there’s a greater probability it’ll promote, and promote for extra.

Easy issues could make an enormous distinction, equivalent to new paint, carpet, brilliant lighting, vegetation, flowers, and even primary cleanliness or a scarcity of litter.

And even the way you organize your own home. For instance, if dwelling workplaces are en vogue, make a room that served a special function into an workplace to usher in extra consumers.

10. Hire it out – Among the best methods to construct fairness is to have another person do it for you.

For those who lease out half or all your property, it’s potential to construct fairness by way of the lease you obtain out of your tenants every month.

Having another person repay your mortgage is fairly candy, particularly if the property appreciates on the similar time.

11. Greater down cost – Lastly, you may make a bigger down cost on the outset to robotically purchase dwelling fairness and construct it sooner thnaks to a decrease excellent stability.

Whereas this may occasionally seem to be you’re placing cash in an illiquid funding, extra fairness means a decrease loan-to-value ratio, which can equate to a decrease rate of interest, no mortgage insurance coverage, and easier-to-obtain financing.

Over time, that decrease mortgage price and smaller mortgage stability will imply much less curiosity paid and extra fairness accrued.

It’s additionally potential to recast a mortgage or full a cash in refinance to get your mortgage stability down and enhance your fairness.

Simply do not forget that any more money is likely to be higher served elsewhere, such because the inventory market or a retirement account.

Bonus: For those who occur to be an underwater house owner, get the financial institution to grant you principal forgiveness and also you’ve basically constructed dwelling fairness, even in the event you’re nonetheless simply above water consequently.

[ad_2]

Source link

{kind=link}