[ad_1]

Larger mortgage charges possible coming quickly

Following a Fed assembly that ended on Wednesday, Sept. 22, it’s trying more and more possible that mortgage charges will begin rising — and “quickly.”

Likelihood is that shall be from November 3 onward (which is the date of the subsequent Fed assembly). However rates of interest may begin trending up as quickly as October.

When you’re ready to reap the benefits of in the present day’s low charges, you won’t wish to wait for much longer. The low-rate refinance window may shut in a matter of weeks.

Find your lowest rate. Start here (Oct 1st, 2021)

Why the Fed issues for mortgage charges

First, let’s get one factor straight: the Federal Reserve doesn’t set mortgage charges. However it has been retaining these charges artificially low over the previous 12 months.

The Fed has been shopping for mortgage-backed securities (MBS) since March 2020. MBS are a sort of bond that largely determines mortgage rates. And when there’s extra money flowing into MBS — just like the $40 billion monthly the Fed is contributing — rates of interest go down.

The Federal Reserve at the moment owns MBS price greater than $2.5 trillion. The sheer quantity has distorted the mortgage market, pushing charges beneath 3% and retaining them there all through 2021.

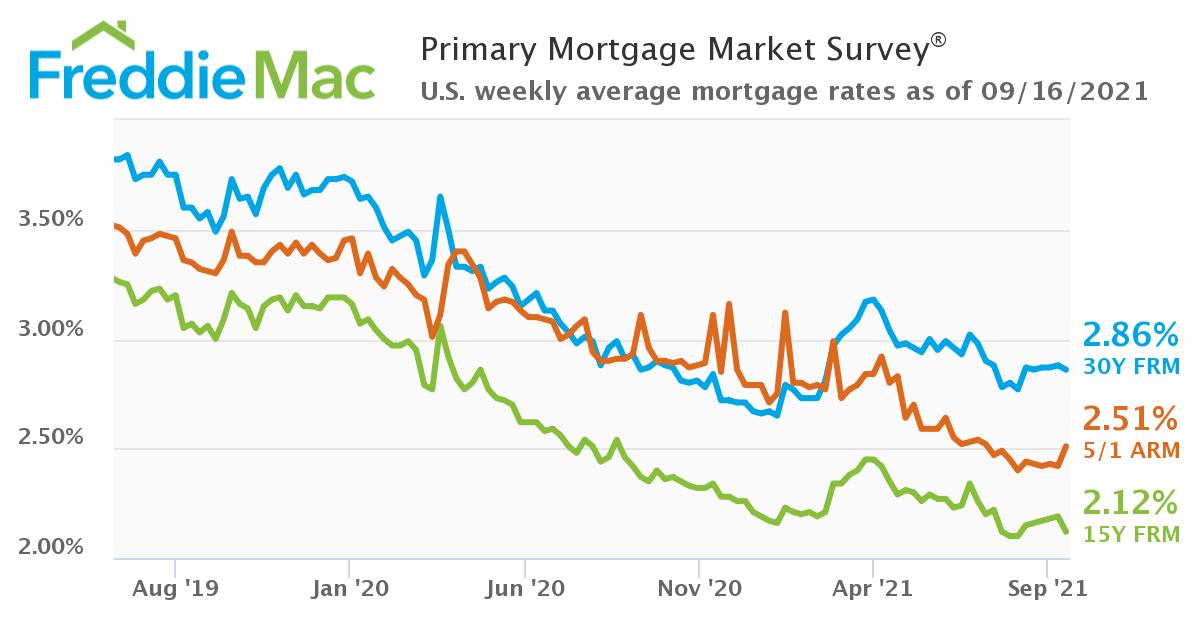

Mortgage rate of interest developments throughout Covid

Supply: Freddie Mac

However this was solely ever speculated to be a short-term program, meant to counter the worst financial results of the COVID-19 pandemic.

And the Fed’s now trying to wind its MBS buy program down, finally to zero. This is named “tapering” in Fed jargon. And when it occurs, it’s prone to drive mortgage charges up out of the two% vary.

Find your lowest mortgage rate before rates rise (Oct 1st, 2021)

The information from this week’s Fed assembly

The Federal Open Market Committee (FOMC) is the Federal Reserve’s decision-making physique. It met this week to debate present financial insurance policies — together with when the Fed may begin shifting away from its Covid stimulus applications.

In a statement and information convention afterward, the FOMC made clear that it deliberate to taper its purchases of MBSs shortly. Within the Fed’s personal ultra-cautious phrases:

“If progress continues broadly as anticipated, the Committee judges {that a} moderation within the tempo of asset purchases [including MBSs] could quickly be warranted.”

When will tapering begin?

Nearly each monetary journalist and Wall Road analyst reckons that the FOMC will announce plans to begin tapering instantly after the subsequent Fed assembly, which is due on November 3.

Nonetheless, we must always have some indication of what’s going to occur to charges on October 8.

That’s the day on which September’s employment state of affairs report is revealed.

If the employment report is disastrous, mortgage charges may fall in October as a result of the Fed may delay tapering to a minimum of December 16 (its closing assembly of the 12 months).

However, if employment numbers are good, then mortgage charges may rise as a result of an early begin to tapering would look inevitable.

How a lot may mortgage charges go up in 2021?

Most economists imagine mortgage charges will virtually inevitably rise with tapering. However by how a lot?

Nicely, we will look to historical past for a clue. As a result of the Fed introduced it could taper a really related program in 2013. And after that announcement, mortgage charges skyrocketed greater than a full % over the subsequent few months.

The St. Louis Fed recollects what occurred:

“On Might 22, 2013, Federal Reserve Chair Ben Bernanke introduced that the Fed would begin tapering asset purchases at some future date, which despatched a detrimental shock to the market, inflicting bond buyers to begin promoting their bonds.”

Freddie Mac’s archives present us how 30-year, fixed-rate mortgages (FRMs) reacted to that announcement:

- April 2013 — 3.25%

- Might 2013 (tapering announcement) — 3.54%

- June — 4.07%

- July — 4.37%

- Aug. — 4.46%

- Sept. — 4.49%

For the remainder of the 12 months, charges fell and rose a bit of, ending the 12 months at 4.46%.

Let’s take the least sensational figures we will and say they jumped from 3.54% to 4.07% as a direct results of the announcement.

If historical past does repeat itself within the coming months, and tapering begins in early November, we may see charges for 30-year FRMs approaching 3.5% by the top of this 12 months.

The Fed hopes that historical past received’t repeat itself this time round. It says, ” … the announcement in 2021 [a pre-pre-announcement in July] was according to market expectations and the announcement in 2013 got here sooner than anticipated.”

Nicely, possibly. However, in 2013, the rises saved coming after the preliminary shock. And mortgage charges didn’t dip to their pre-announcement degree till 2016.

If historical past does repeat itself within the coming months, and tapering begins in early November, we may see charges for 30-year FRMs approaching 3.5% by the top of this 12 months and nearer to 4% by March or April 2022.

Find your lowest mortgage rate before rates rise (Oct 1st, 2021)

Charges may rise as quickly as October

The following Fed assembly is in early November. However mortgage charges may rise earlier for 2 causes.

First, there’s that October 8 employment state of affairs report. We already talked about how that would successfully make tapering a certainty. And which may trigger buyers to behave as if a proper announcement had already been made.

However there’s a second risk to low mortgage charges that has nothing to do with the Federal Reserve.

And that’s the debt ceiling.

Congress may fail to boost that ceiling earlier than mid-October, which is when the treasury secretary reckons the federal authorities will run out of cash.

If that occurs, we’ll face a authorities shutdown. However way more critically, america may start to default on its debt funds. And that’s one thing that’s by no means, ever occurred earlier than.

What does the debt ceiling need to do with mortgage charges?

Nicely, CNBC reviews that “Demand for U.S. Treasury bonds may sink if they’re not thought-about a dependable, safe-haven funding… That, in flip, would ship different borrowing prices increased, together with bank cards, automobile loans, and mortgage charges”

Likelihood is, legislators will come to their senses earlier than then. However even taking it to the brink might be critically dangerous. As a result of the final time the debt ceiling was near being left unraised was in 2011. And America’s credit standing was broken and rates of interest rose consequently.

Be aware, these penalties didn’t come up as a result of America had defaulted. It didn’t. They occurred as a result of the threat of default seemed extra doable than anybody had beforehand dreamed.

The refi window may very well be closing

The underside line for house consumers and owners trying to refinance is that in the present day’s low mortgage charges won’t be round for much longer.

If mortgage charges react to the November 3 Fed assembly as most count on, we may very well be waving the present period of “near-record-low charges” goodbye.

After all, financial forecasts aren’t at all times appropriate — not even near it. And it’s doable none of it will come to cross.

However it’s laborious to recollect a time when issues seemed grimmer for mortgage charges. And lots of consultants assume they’re a window of alternative for mortgage refinancings that’s likely closing.

So if you wish to refinance and also you’ve but to lock a charge, it is perhaps time to get severe about doing so.

[ad_2]

Source link

{kind=link}