[ad_1]

Some people are blessed with household who’ve greater than sufficient financially. It’s solely pure that folks, grandparents, and spouses who love you’d need to assist along with your schooling bills not directly. If you happen to graduate with out scholar mortgage debt as a result of you will have mother and father paying for graduate college, take into account your self fortunate.

Nevertheless, many different graduate college students make one of the frequent household monetary errors to keep away from for grad college. There’s a harmful center floor growing due to the ridiculously excessive cost of a graduate degree. If you happen to’re going to take monetary assist from household, it’s greatest if that assist covers your entire value of attendance for that program.

To reiterate, protecting solely a PART of somebody’s grad college value may be DISASTROUS. Right here’s find out how to know if accepting cash from household is useful or simply including large prices to the equation.

Mistake 1: Utilizing the financial institution of grandma and grandpa for scholar mortgage refinancing

Grandparents love curiosity, however they’ll’t get any when financial savings accounts on the banks solely yield 2%.

You, due to this fact, devise a plan collectively to have them fund part of your schooling by making loans out to you off the books. You’ll lower your expenses they usually’ll earn extra earnings than on the financial institution.

Regardless of how low the rate of interest is that you just’re receiving from household, it gained’t be as little as the efficient fee you get when you’re on monitor to have a lot of your loans forgiven.

Alanna the vet getting cash from grandma for vet college

To see how this might go unsuitable, let’s take a look at an instance of a hypothetical veterinarian named Alanna who goes to Penn. She’s anticipating to owe $380,000 if she funds the entire diploma program.

Alanna’s grandma decides to assist her out with the price by protecting $100,000 out of her financial savings. Alanna doesn’t need this to be a present. So, she makes her grandma agree to simply accept funds at a low rate of interest from her when she graduates.

First, let’s tackle the clearly morose. What if Alanna dies earlier than paying again her grandma? That’s an unlikely state of affairs and one which’s simple to guard towards. For instance, she may try the price of a time period life coverage from a spot like Haven Life. Getting $100,000 in protection ought to value virtually nothing.

The true danger right here is that Alanna would nonetheless graduate with $280,000 in debt. That’s unimaginable to pay again on a typical vet wage of about $70,000 to $100,000.

By refinancing along with her grandma, Alanna has taken away $100,000 that was projected to be forgiven with federal scholar loans. If left on the federal authorities system, she may’ve paid maybe 40% in earnings taxes on that cash in 20 to 25 years on a forgiveness-based approach.

Additionally, Alanna’s fee is similar with $280,000 or $380,000 in federal loans as a result of it’s a p.c of her earnings. Meaning by refinancing with grandma, she’s successfully taken on two funds as a substitute of 1.

Quite than saving for retirement or placing cash away for her anticipated tax penalty when the loans are forgiven, she’s making $1,000 monthly funds to grandma to make good on her debt.

Even when the refinancing is taken into account a present, it’s an especially inefficient one.

Mistake 2: Utilizing your private home to contribute to grad college

I see this error made most often by East Asian and South Asian American households, though it’s not restricted to this phase of oldsters. It’s one of many frequent errors to keep away from when paying for grad college.

On this state of affairs, mother and father are keen to assist their grad college college students obtain monetary safety with a excessive paying, assured skilled job.

The mother and father often usually are not rich and may need a mid to excessive six-figure internet price. One among their major property is their house fairness, they usually may need a little bit of retirement financial savings. The mother and father count on the kid they’re serving to to fund them of their older years.

Puja the dentist with mother and father taking up a second mortgage to assist with grad college

To see how this works in apply and why it’s so damaging, let’s faux Puja is a dentist graduating from NYU. She’ll owe $550,000 at commencement if she receives no assist and funds the entire thing.

Puja’s mother and father are first-generation immigrants from India. They’ve received about $300,000 of house fairness and roughly $500,000 of their retirement accounts. They’re of their early 60s and earn about $100,000 a yr.

Puja receives $200,000 in the direction of her dental college value from her mother and father. The expectation is that she’s going to repay them by serving to deal with them financially of their previous age.

Relating to paying for grad college, Puja graduates with $350,000 in dental college debt. She decides that apply possession shouldn’t be for her, so she begins working as an affiliate at Heartland Dental. She’ll begin off making $120,000 and ultimately will prime out round $180,000.

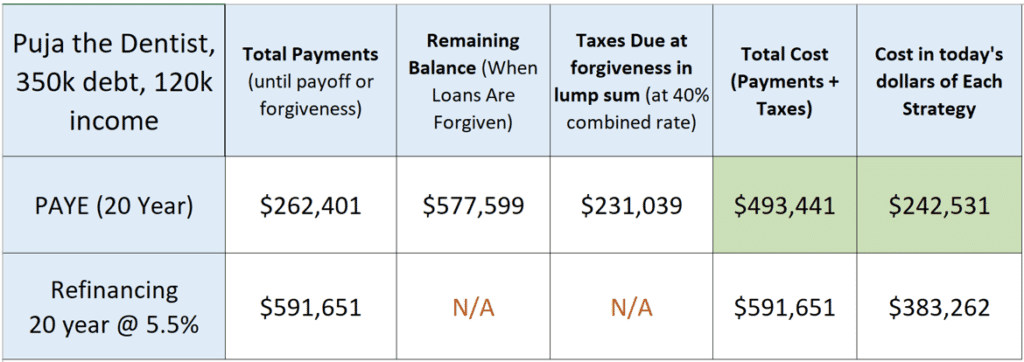

To make issues easy, we’ll simply embrace Puja on this evaluation. Right here’s what the price of her choices seems like with PAYE at 7% vs non-public lender refinancing over 20 years at a 5.5%.

The price distinction is discreet when you simply take a look at the full value as a result of a lot of the PAYE funds occur on the finish of the 20-year fee interval.

The price distinction is over $140,000 in right this moment’s {dollars}, assuming a 5% fee of return on investable property.

What does that imply in English? Puja’s mother and father are paying $200,000 however Puja is receiving a fraction of that in profit from decrease tax funds on the finish.

All Puja’s mother and father have accomplished is wipe away $200,000 of house fairness and make their retirement much less safe for the longer term. Puja remains to be going for mortgage forgiveness even with their beneficiant assist.

Mistake 3: Dad and mom paying for graduate college with Father or mother PLUS Loans for actually everyone

Stafford mortgage limits for undergraduates are very low in comparison with grad college. Many mother and father really feel an obligation in our tradition to present their kids no matter faculty expertise they need.

I’ve seen this primary hand when many mother and father paying for graduate college e-mail me with enormous balances that can’t be positioned on essentially the most beneficiant reimbursement plans.

Parent PLUS are solely eligible for Income Contingent Repayment (ICR IF they’ve been consolidated. That requires 20% of your earnings, so many mother and father won’t be able to count on a lot forgiveness.

To see how this error occurs, let’s take a look at Bob the company center supervisor dad of three. Bob needs to retire within the subsequent 5 to 10 years, however he additionally needed to assist his children via college. Bob takes on about $100,000 in Father or mother PLUS Loans for every youngster to assist pay for his or her undergraduate diploma.

The kids have the utmost undergrad Stafford loans, however they aren’t very massive as a consequence of low mortgage limits.

Bob makes about $120,000 a yr, however he finds out that his funds could be $3,000 a month if he was going to pay the loans again in 10 years. As a result of he’s making an attempt to work in the direction of retirement and repay the final little bit of his mortgage, these funds aren’t potential.

His kids wish to assist and take over their $100,000 of scholar loans, however just one can afford to try this because the funds could be $1,000 a month.

Father or mother PLUS Loans additionally carry the best rate of interest the federal government affords, at 7% proper now.

It could’ve been much better to be lifelike with the three kids that simply because the federal government will provide you with the cash, it doesn’t make it sensible, significantly with enormous Father or mother PLUS Loans.

The kids ought to have chosen decrease value applications or utilized for ROTC scholarships if the colleges they selected have been really non-negotiable for them.

Household doesn’t give income-based protections or forgiveness

The federal government affords the most effective safety for scholar mortgage reimbursement in addition to getting extra graduate college monetary help. Economic hardship? You possibly can cease funds for 3 separate one-year intervals. Incapacity or loss of life? Loans are forgiven. Revenue drops as a consequence of job change or household causes? Your income-based reimbursement decreases too.

Household can not supply any of those protections (until the mortgage represents a small slice of their internet price) when mother and father are paying for graduate college.

That’s why earlier than accepting cash from household for grad college, it is best to ask your self these three questions:

- Will this contribution to my schooling delay or hinder my member of the family’s retirement in any manner?

- Does this mortgage signify greater than 10% of their internet price?

- Would this member of the family be upset when you turned unable to pay again the mortgage in full?

If the reply is sure to any of those questions, grad college students mustn’t settle for cash from the member of the family.

The taxpayer is paying for our advanced and tousled scholar mortgage system, so that you may as nicely profit from it moderately than burden mother and father, grandparents, and spouses with the artificially excessive tuition costs we see presently in skilled applications.

Scholar loans carry out any sophisticated household dynamics

Maybe essentially the most ferocious struggle I’ve seen over cash in a household was with a multimillionaire who handed away. He had a number of kids, and two of the youngsters had obtained loans of a number of hundred thousand.

The expectation with their father was that the children would ultimately pay the cash again. He died, after which the property was set to be cut up up.

The youngsters who obtained the mortgage contended that was a present. They needed their full share cut up equally amongst all the children. The kids who didn’t get the mortgage mentioned that their siblings had obtained a portion of their inheritance early, and thus weren’t entitled to extra.

I hope I’ve proven you that having mother and father paying for graduate college is a harmful thought when you’re going to owe greater than two occasions your wage anyway at commencement.

If you happen to gained’t have any debt because of household generosity, make certain it’s pleased with all concerned. In case your mother and pa need to offer you cash for varsity however they haven’t accomplished that to your brothers or sisters, make certain their needs are clear, even when they’re hurtful.

You don’t want a really form and beneficiant act of paying for varsity to show right into a household struggle. Preemptively tackle any pressure created by household monetary assist for grad college.

What when you make the unsuitable selection along with your scholar loans?

Whereas these three household monetary errors to keep away from earlier than grad college can positively value you, say that I described you see on in one in all these errors that I discussed, not all is misplaced. There are all the time methods to mitigate the harm from an unlucky student loan strategy.

Be happy to take a look at our seek the advice of service the place we will make a plan to successfully deal with your six-figure scholar debt.

[ad_2]

Source link

{kind=link}