[ad_1]

Our aim is to provide the instruments and confidence it is advisable to enhance your funds. Though we obtain compensation from our associate lenders, whom we’ll at all times establish, all opinions are our personal. Credible Operations, Inc. NMLS # 1681276, is referred to right here as “Credible.”

Whereas individuals with larger credit score scores are inclined to get higher phrases on their mortgage, you don’t need to goal for the very best rating potential.

Each mortgage program has its personal minimal credit score rating necessities, and with a 700 credit score rating, you’re prone to qualify for a mortgage and snag a very good rate of interest.

Right here’s what it is advisable to find out about credit score scores of 700 or larger:

How good is a 700 credit score rating?

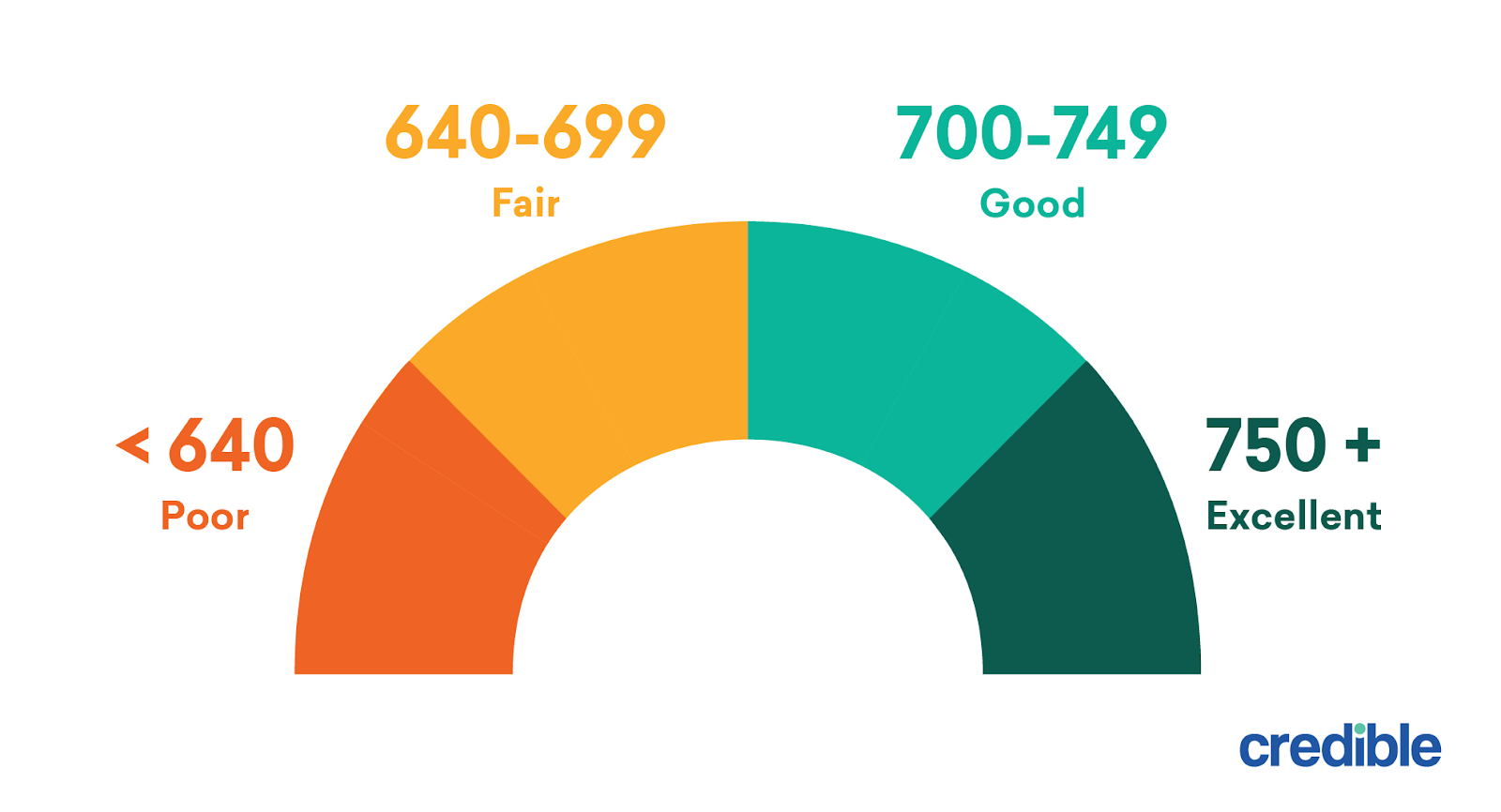

Mortgage lenders are inclined to group credit scores into ranges, and candidates inside one vary obtain the identical (or related) rates of interest. On a scale of 300 to 850, a 700 credit score rating often falls into the “good” vary.

Having a credit score rating of 700 is advantageous as a result of:

- It will possibly enable you to qualify for the mortgage. Most typical and government-backed mortgage packages require a credit score of at least 640. So with a rating of 700, you’ll be capable to test off that requirement.

- You could possibly have room to barter for higher phrases. As a result of you will have a very good credit score rating, lenders may be prepared to barter the mortgage charge and different mortgage phrases to compete for what you are promoting.

- A great rating can result in decrease rates of interest. That’s as a result of credit score scores assist lenders predict threat, and a better rating lets them know you’re prone to make funds on time.

Study Extra: What Is a Mortgage Rate and How Do They Work?

Common mortgage charges for a 700 credit score rating

Credit score scores are an necessary piece of the qualification course of as a result of lenders use them to foretell whether or not you’ll repay a mortgage as agreed. With a very good credit score rating, you’re prone to qualify for a house mortgage and receive a good interest rate.

The desk under reveals charge estimates from our associate lenders. You’ll be able to fill in your monetary info and choose a credit score rating vary of Good to see what sort of mortgage charges can be found to you in your space.

The charges on this desk show an annual percentage rate (APR), which incorporates the mortgage’s rate of interest plus any charges and additional prices charged by the lender.

As a result of the APR displays the overall price of borrowing, it’s a good suggestion to match this quantity when searching for mortgages. Qualifying for a decrease APR will help you save 1000’s of {dollars} over the lifetime of the mortgage.

Somebody with a credit score rating of 680, then again, may get an APR of three.17%. Their month-to-month cost can be $862.

Whereas that’s solely a distinction of $20 a month, it provides up over time. The particular person with the decrease credit score rating would pay $7,200 extra over the lifetime of the mortgage.

When you ought to deal with getting your credit score rating as excessive as potential, it doesn’t have to be good. Improving your credit score by only a few factors may put you within the subsequent credit score rating vary and offer you entry to raised charges.

Enter your mortgage info to calculate how a lot you may pay

Whole Cost

$

Whole Curiosity

$

Month-to-month Cost

$

With a

$

residence mortgage, you’ll pay

$

month-to-month and a complete of

$

in curiosity over the lifetime of your mortgage. You’ll pay a complete of

$

over the lifetime of the

mortgage.

Want a house mortgage?

Credible makes getting a mortgage straightforward. It solely takes 3 minutes to see for those who qualify for an on the spot streamlined pre-approval letter.

Checking charges gained’t have an effect on your credit score rating.

Different components behind your mortgage charge

Whereas a very good credit score rating will help you qualify for a mortgage and decrease rate of interest, it isn’t the one issue behind a mortgage supply.

Lenders take the broader financial system under consideration and take a look at the small print of your total monetary scenario when figuring out charges. For instance, they take into account most of the following components:

| Bigger financial components | Private financial components |

|---|---|

|

|

You’ve got management over a few of these components, which provides you a greater likelihood at scoring a low rate of interest.

- Down cost: Each mortgage program has its personal down payment requirements, beginning as little as 0% or 3% for some certified debtors. However for those who can afford to place down at the least 20%, then you definately gained’t need to pay private mortgage insurance and may qualify for a decrease rate of interest.

- Mortgage dimension: Making a hefty down cost has one more benefit: It shrinks your month-to-month mortgage invoice because you’re borrowing much less cash. And since that poses much less threat for the lender, they may decrease your rate of interest.

- Mortgage time period: Whereas shorter mortgage phrases have larger month-to-month funds, they have a tendency to come back with decrease rates of interest as a result of the lender is taking up much less threat.

- Debt-to-income ratio: Lenders test your debt-to-income ratio to see how a lot you earn every month and the way a lot of that goes towards debt funds. Usually, a DTI ratio of 45% or much less will help you qualify for a mortgage. However a decrease ratio will help you get a greater rate of interest.

Buying round and evaluating charges from completely different lenders is a method to make sure you get an important charge in your subsequent mortgage.

Credible will help with this. In only a few minutes, you’ll be able to evaluate prequalified charges from all of our associate lenders — it’s free, and also you don’t even have to depart our platform.

House mortgage choices for a 700 credit score rating

A credit score rating of 700 will help you qualify for one of many main mortgage packages. Listed here are your fundamental choices:

FHA loans

Mortgages insured by the Federal Housing Administration are widespread with first-time homebuyers as a result of they’ve versatile credit score rating and down cost necessities.

You probably have a credit score rating of at the least 580, you may qualify for an FHA loan, and also you’d solely be required to place down 3.5%. With a credit score rating within the 500-to-579 vary, you may qualify with a down cost of at the least 10%.

- Upsides: Relaxed credit score rating and down cost necessities.

- Downsides: Most FHA mortgage debtors need to pay mortgage insurance coverage, each as an upfront premium and as a month-to-month price baked into the mortgage cost.

VA loans

The sort of mortgage is backed by the U.S. Division of Veterans Affairs and requires no down cost and has no minimal credit score rating. Nonetheless, debtors must pay a funding payment that ranges from 1.4% to three.6% of the house’s buy value.

- Upsides: You don’t need to make a down cost or pay for mortgage insurance coverage.

- Downsides: VA loans are solely obtainable to eligible navy members, veterans and surviving spouses.

USDA loans

A USDA residence mortgage is available in two varieties: direct and assured. Direct loans are funded by the U.S. Division of Agriculture, whereas assured loans are funded by personal lenders and backed by the USDA.

These mortgages don’t include a down cost, and credit score rating necessities begin at 620 (although some lenders may increase the requirement to 640).

- Upsides: You could possibly qualify with a credit score rating as little as 620.

- Downsides: You have to purchase a house in an eligible rural space and meet revenue necessities.

Standard loans

To qualify for a conventional mortgage, you’ll usually want a credit score rating of at the least 620 and a minimal down cost of three%. These mortgages aren’t backed by authorities companies. As a substitute, the lender often sells the mortgage to Fannie Mae or Freddie Mac.

- Upsides: You’ll be able to keep away from paying personal mortgage insurance coverage by placing down at the least 20%. With a smaller down cost, you’ll be able to cancel PMI as soon as the mortgage steadiness reaches at the least 80%.

- Downsides: The minimal credit score rating requirement is 620, which is larger than what the FHA requires.

Jumbo loans

A jumbo loan is a mortgage with a steadiness that’s larger than the conforming mortgage restrict for the county by which you’re shopping for or refinancing. In most locations, the conforming mortgage restrict is $548,250. However in some higher-cost markets, the mortgage restrict rises to $822,375.

You’ll usually need to put down between 10% and 30%, and the credit score rating necessities often begin round 680 or 700.

- Upsides: A jumbo mortgage may enable you to purchase a house in a market with excessive residence costs.

- Downsides: The down cost necessities are larger than different mortgage packages, so that you’ll want to save lots of up a good chunk of change.

Methods to increase your credit score rating

Whereas a 700 credit score rating will help you qualify for a mortgage, you may get higher mortgage phrases by boosting your rating — which may prevent 1000’s of {dollars} over the lifetime of the mortgage.

If you happen to’ve been monitoring your credit, you will have a good suggestion of the place your credit score rating stands.

Listed here are some methods you’ll be able to enhance your credit score scores:

- Pay down your debt balances.

- At all times make funds on time. Computerized funds or month-to-month alerts will help.

- Change into a certified consumer on another person’s bank card account.

- Solely open credit score accounts that you just want.

- If a few of your accounts are delinquent or you will have a considerable amount of debt, take into account contacting a credit score counseling company.

Maintain Studying: How Your Credit Score Impacts Mortgage Rates

Concerning the writer

[ad_2]

Source link

{kind=link}