[ad_1]

Adjustable-rate mortgages in 2022

As mortgage charges rise, homebuyers and mortgage refinancers are increasingly turning to adjustable-rate mortgages (ARMs).

Preliminary ARM charges are sometimes a lot decrease than fastened mortgage charges, typically by a full percentage point or extra. And that would assist cut back your month-to-month fee or improve your private home shopping for price range.

However adjustable-rate mortgages are dangerous, too. So does an ARM make sense for you? That depends upon your long-term plans. Right here’s what it’s best to know.

On this article (Skip to…)

At this time’s adjustable mortgage charges

Joel Kan, MBA’s affiliate vice chairman of financial and business forecasting, not too long ago wrote that “Extra debtors proceed to make the most of ARMs to fight larger charges. The share of ARMs elevated to 11 p.c of general loans and to 19 p.c by greenback quantity” throughout the week ending Could 6, 2022.

So persons are selecting adjustable-rate loans far more steadily than they used to. However why is that?

First, just about all mortgage charges shot up over the primary quarter of 2022, making homeownership far more costly. One solution to get round that’s to discover a mortgage with a decrease charge — akin to an ARM.

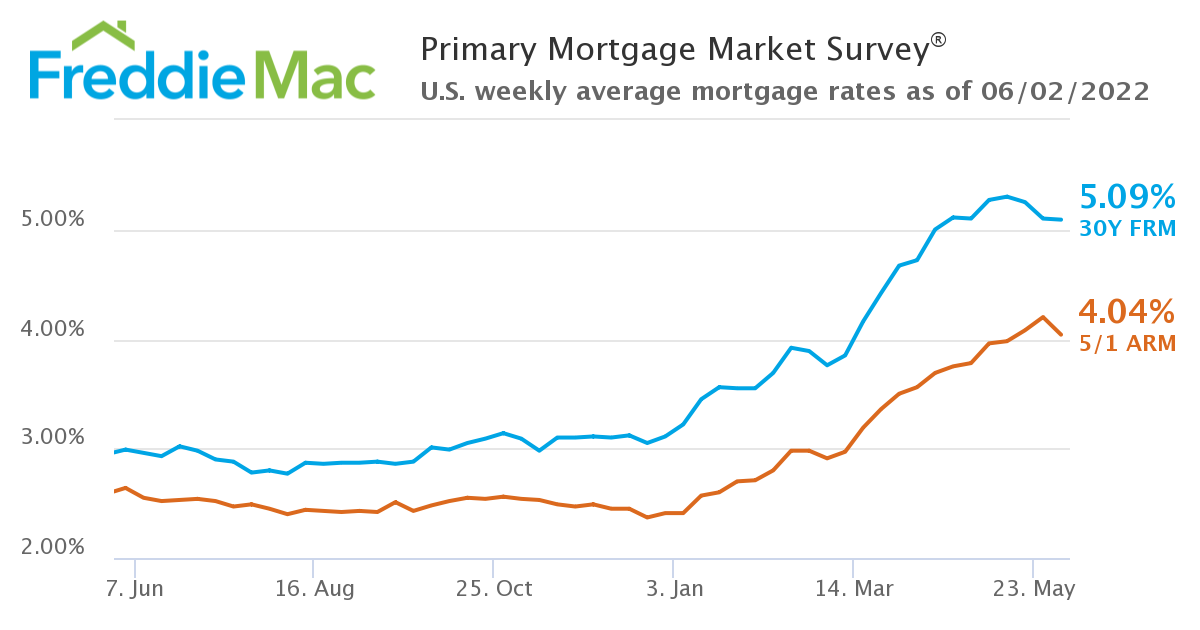

Second, the hole between FRM and ARM charges has grown considerably wider, making ARMs an much more enticing cut price. How extensive is that hole? Check out this graph by Freddie Mac, and also you’ll see how, by the top of Could 2022, common 5/1 ARM charges have been a full share level decrease than 30-year fastened charges:

How ARM loans may help homebuyers

Having a decrease ARM mortgage charge may help you in two methods. You possibly can:

- Purchase a house for a similar value you deliberate and have a decrease month-to-month mortgage fee

- Hold your month-to-month fee the identical however afford a dearer house

Lenders work out how a lot you may borrow primarily based primarily in your debt-to-income ratio (DTI). And a decrease rate of interest, such because the intro charge on an ARM mortgage, provides you extra buying energy.

So you may obtain actual advantages if you get an ARM. That’s, a minimum of whereas the decrease introductory charge lasts — which is often for five, 7, or 10 years. We clarify how ARM charges work in more detail below.

ARM vs. FRM: Greenback-for-dollar comparability

How a lot would possibly you save in the event you get an ARM in comparison with an FRM? We’ve provide you with an instance utilizing our mortgage calculator. In fact, it’s unlikely your situation would be the identical because the one we imagined. So by all means, run your personal numbers your self.

We’re going to imagine you desire a mortgage of $342,960. That’s the median house value nationwide within the first quarter of 2022 ($428,700) minus a 20% down fee.

Primarily based on the mortgage charges proven within the Freddie Mac graph (above), how huge is the hole between month-to-month funds on ARMs and FRMs?

- 5/1 ARM: Month-to-month fee of $1,645 with a 4.04% mortgage charge*

- 30-12 months FRM: Month-to-month fee of $1,860 with a 5.09% mortgage charge*

*Fee examples embody mortgage principal and curiosity solely. Your personal rate of interest and fee will likely be totally different.

On this instance, selecting an ARM will prevent $215 per 30 days, a minimum of for the 5-year fixed-rate interval in your ARM. That’s $2,580 a 12 months for the primary 5 years — or $12,900 whole. Given how inflation’s going, you could be glad for that extra cash.

Affording extra house with an ARM mortgage

Let’s rerun that situation to see how far more you would possibly have the ability to afford as your buy value. This time, we’ve chosen the “By month-to-month fee” tab on our calculator.

We set the goal month-to-month fee at $1,860 and stored the down fee quantity round $85,740 (the identical as the instance above). And we’re nonetheless utilizing Freddie’s mortgage charges for June 2, 2022.

On this instance, assuming the identical month-to-month fee, you can borrow:

- 5/1 ARM: $450,600 with a 4.04% mortgage charge*

- 30-12 months FRM: $429,000 with a 5.09% mortgage charge*

*Examples calculated utilizing mortgage principal and curiosity solely. Your personal rate of interest and residential shopping for price range will likely be totally different.

So, with the identical month-to-month fee, you would possibly have the ability to borrow an additional $21,600 with an ARM. And that could possibly be the distinction between settling for second finest and buying your good place.

How adjustable mortgage charges work

In the event you’re following rates of interest, you’ll know they’ve gone up sharply in 2022. And also you’re in all probability conscious that — as of Could 2022, when this was written — the Federal Reserve has penciled in several more significant hikes.

None of this could hassle you in the event you go for a fixed-rate mortgage. No matter occurs, your mortgage charge can’t change.

However issues are very totally different in the event you select an ARM. The clue’s within the identify: “adjustable-rate mortgage.” Finally, somebody with an ARM could possibly be hit by a lot larger charges and month-to-month funds.

So why would anybody select an adjustable-rate mortgage at a time of sharply rising charges? For 2 causes:

- You get to take pleasure in your low ARM charge for a hard and fast interval of years. With an ARM, you may lock your low intro charge for a set time; sometimes 5, 7, or 10 years. In the event you don’t plan to maintain your mortgage longer than that, an ARM could possibly be an important deal

- The quantity your rate of interest can improve with an ARM is capped. Even when the locked interval expires, most ARMs include protections that average the doable harm

Learn on for extra element on how ARM charges work and what to anticipate in the event you get any such mortgage.

ARMs have an preliminary fixed-rate interval

Nearly all ARMs these days include an preliminary interval throughout which their charge is locked. You’ll see them marketed as x/y (e.g. 5/1 ARM). “X” is the variety of years that charge can’t transfer. And “Y” is how typically the speed can rise when that preliminary interval ends. Y is sort of at all times 1, which means the speed can transfer as soon as yearly.

For instance, a 5/1 ARM — the most typical sort of ARM mortgage — has:

- A complete mortgage time period of 30 years

- A hard and fast rate of interest for the primary 5 years

- Potential in your charge to alter as soon as per 12 months after the primary 5 years

You may as well discover 3/1, 7/1, and 10/1 ARMs. These work the identical as a 5/1 ARM apart from the variety of years your intro charge is fastened.

The quantity your ARM charge can improve is capped

You want to speak to your lender and verify your mortgage settlement to ascertain the protections your explicit ARM offers. However federal regulator the Shopper Monetary Safety Bureau (CFPB) offers a list of typical ones:

- Preliminary adjustment cap — How a lot the speed can rise when the preliminary fixed-rate interval ends. The CFPB says: “It’s frequent for this cover to be both two or 5 p.c — which means that on the first charge change, the brand new charge can’t be greater than two (or 5) share factors larger than the preliminary charge throughout the fixed-rate interval”

- Subsequent adjustment cap — How a lot the speed can improve at every annual assessment. “This cover is mostly two p.c, which means that the brand new charge can’t be greater than two share factors larger than the earlier charge”

- Lifetime adjustment cap — How a lot the speed can improve in whole over your entire lifetime of the mortgage. “This cover is mostly 5 p.c, which means that the speed can by no means be 5 share factors larger than the preliminary charge. Nonetheless, some lenders might have a better cap”

These caps could make a giant distinction to ARM debtors who would possibly in any other case face a really sharp improve of their mortgage charge and month-to-month fee. Nonetheless, they solely average these results. And you want to make certain you’re in adequate monetary form to cope with any charge rises after they come.

What it means for you

All this may be necessary to house consumers selecting an ARM. Though a 2020 report from the Nationwide Affiliation of Realtors says the typical house owner stays of their house for 13 years, many transfer far more steadily.

Suppose you’re nearly positive you’ll transfer throughout the subsequent seven years. Maybe your job would require it or your loved ones circumstances will change. What’s the purpose of paying additional to repair your charge for 30 years when a 7/1 ARM will defend you greater than adequately?

Sometimes, the longer your preliminary, fixed-rate interval lasts, the upper the speed you’ll pay. So a 7/1 ARM might be extra pricey than a 5/1 ARM. However with any ARM intro charge, you’re seemingly to economize in comparison with a 30-year fixed-rate mortgage.

Who ought to get an ARM mortgage in 2022?

ARMs usually are not with out danger. Mortgage charges are rising, and in case your fixed-rate interval expires, you can face considerably larger charges and mortgage funds within the coming years.

However for the fitting individual, an adjustable-rate mortgage is a superb instrument.

The dangers are small in the event you’re positive you’ll transfer house inside 5, seven, or 10 years — earlier than the low intro charge expires. In that case, an ARM is a reasonably protected guess. And you may profit from the decrease charges these mortgages carry.

In the event you’re planning to stay in your house for far more than 10 years, nevertheless, an ARM poses larger risks. If rates of interest transfer as excessive as many count on, you can expertise an actual monetary shock when your preliminary, fixed-rate interval ends.

True, you can in all probability refinance to a fixed-rate mortgage at that time. However how excessive will mortgage charges for these be by then?

ARMs present the fitting debtors with nice alternatives to make huge financial savings or to purchase nicer properties. However it’s best to absolutely perceive this product and your homeownership timeline earlier than signing on.

The data contained on The Mortgage Reviews web site is for informational functions solely and isn’t an commercial for merchandise provided by Full Beaker. The views and opinions expressed herein are these of the writer and don’t mirror the coverage or place of Full Beaker, its officers, father or mother, or associates.

[ad_2]

Source link

{kind=link}