[ad_1]

Neighborhood property states are states the place each spouses have equal possession of all revenue earned, property and money owed acquired through the marriage.

In group property states, a pair’s marital property and property are cut up 50/50 within the occasion of divorce. However group property legal guidelines may also have an effect on People throughout their marriage. And that’s very true if one or each spouses are scholar mortgage debtors.

On this information, we’ll check out what a group property state is and the way residing in a single can have an effect on your taxes and scholar mortgage compensation plan.

Right here’s what that you must know.

What states are group property states?

Neighborhood property states are a minority in america. Most states comply with the widespread legislation property system and are sometimes called equitable distribution states. In these states, the courts resolve on a case-by-case foundation how property ought to be divided if the couple can not come to an settlement on their very own.

Presently, there are 9 group property states. They’re:

- Arizona

- California (guidelines additionally usually apply to home companions)

- Idaho

- Louisiana

- Nevada (guidelines additionally usually apply to home companions

- New Mexico

- Texas

- Washington (guidelines additionally usually apply to home companions)

- Wisconsin

Alaska, South Dakota, and Tennessee enable {couples} to decide on in the event that they wish to comply with the group property or widespread legislation property system.

What is taken into account group revenue, property and debt?

Solely the revenue you earn throughout your marriage, whereas residing in a group property state is taken into account group revenue. The identical basic rule applies to group property and marital debt accrued throughout marriage (bank card money owed, mortgage, automotive mortgage, and many others.)

It’s vital to level out that each standards have to be met on the identical time for group property guidelines to use. Contemplate the 2 examples beneath:

- You acquire your property whereas residing in a group property state, however earlier than you married your partner.

- You acquire your property whereas married, however earlier than transferring to a group property state.

In each examples listed above, your property wouldn’t be topic to the group property legal guidelines.

Nevertheless, if the house was purchased when you have been married and residing in a group property state, then you definitely and your partner would have equal possession.

Are there any exceptions?

There are exceptions to the principles listed above. For instance, items or inheritance that both partner receives individually is taken into account separate property slightly than being included locally property.

To be taught extra about what qualifies as group property vs. separate property, check out the full IRS guide to Neighborhood Property. Or you may ask a neighborhood household legislation legal professional or property division lawyer about your state’s guidelines.

What for those who personal properties in a number of states?

In the event you personal properties in a number of states, the IRS will use the state guidelines of your everlasting residence. The IRS considers a number of components, together with the place you pay state revenue taxes, the place you vote and the size of your residence, to resolve which state guidelines apply.

Let’s think about that you just personal property in Arizona (a group property state) and Florida (a standard legislation state). And, for sake of instance, let’s additionally think about that you just bought each properties after marriage and whereas residing primarily in Arizona.

On this case, how would the probate courts deal with your Florida property throughout a divorce? In response to the IRS, all of it will depend on your domicile — or your home of your everlasting residence. The entire revenue and property that you just accumulate throughout marriage and residing in a group property state is topic to group property legislation.

So, within the instance above, the Florida property can be cut up 50/50 in a divorce. It will be topic to Arizona’s group property legislation. Even supposing Florida shouldn’t be a group property state.

How can group property legal guidelines have an effect on your taxes?

The largest method group property legal guidelines have an effect on your taxes is once you select a married submitting individually submitting standing.

In most states, every partner experiences their particular person revenue individually on their tax returns. So for those who earned $100,000 and your partner earned $50,000, you’d solely report your $100,000 earnings.

However in group property states, you need to equalize your incomes, even once you file individually. To try this, you are taking the full quantity earned between the 2 of you and divide it in half.

Within the instance above, that might lead to every of you itemizing an revenue of $75,000 in your tax return ($150,000 divided by 2 = $75,000).

This main distinction might make married submitting collectively the higher possibility for sure {couples}. And that might particularly be true for those who’re repaying scholar loans on an income-driven repayment (IDR) plan.

Let’s check out why.

How group property legal guidelines can impression your scholar loans

In sure circumstances, residing in a group property state might have a profound impression in your month-to-month scholar mortgage funds and eventual scholar mortgage forgiveness.

Submitting individually might decrease your scholar mortgage funds

Let’s say that Jenny is a physician who makes $200,000 per yr and has $300,000 in scholar mortgage debt (all federal scholar loans).

We’ll additionally say that Jenny works for a public hospital and is pursuing Public Service Loan Forgiveness (PSLF). Lastly, think about that Jenny’s partner, Paul, is a trainer making $50,000 per yr.

Usually, selecting a married submitting individually standing wouldn’t be all too useful for Jenny.

First, she would lose out on numerous deductions and credit. But her IDR funds wouldn’t drop all that a lot as a result of they might nonetheless be based mostly on her $200,000 revenue.

But when Jenny lived in a group property state, that might change the entire equation.

In that case, her reported revenue would drop to $125,000 by submitting individually. And that might make an enormous distinction. Each in her month-to-month IDR fee in addition to the quantity of PSLF forgiveness she might finally obtain.

Associated: PSLF Tax Implications for Married Couples in Community Property States

When submitting individually might improve your scholar mortgage funds

It’s vital to level out that the tax trick described above gained’t work for everybody.

First, you’ll have to be on an Revenue-Primarily based Compensation (IBR), Revenue-Contingent Compensation (ICR) or Pay As You Earn (PAYE) Plan for this technique to work. On Revised Pay As You Earn (REPAYE), your month-to-month funds are all the time based mostly on you and your partner’s mixed incomes, no matter whether or not you file collectively or individually.

Second, for those who’re the partner that earns much less, you’d be elevating your reported revenue by submitting individually in a group property state.

And since your IDR funds are based mostly in your revenue, submitting individually would trigger your scholar mortgage funds to extend.

Division of scholar loans after divorce in group property states

As we’ve already famous, any money owed taken out by both partner in a group property state is taken into account a joint debt. This will trigger some actual complications for {couples} who divorce or legally separate.

For instance, let’s say that you just’re ex-spouse took out $200,000 of scholar loans whereas married to you and whereas residing in a group property state. Upon your divorce or separation, you’d owe half of that debt ($100,000). That is even though not one of the loans would have been taken out in your identify.

Once more, this case would solely apply in case your partner’s debt had been taken out whereas married to you. Any scholar loans taken out earlier than marriage (or earlier than transferring to a group property state), are the precise borrower’s sole accountability after a divorce.

Observe that some {couples} resolve to create a prenuptial settlement (prenup) earlier than marriage to keep away from all these issues. A prenup is a contract that particulars how marital property can be divided in a divorce. If a pair agree in a prenup to maintain their scholar money owed separate, this could supersede their state’s group property legal guidelines.

Need assistance selecting your submitting standing for scholar loans?

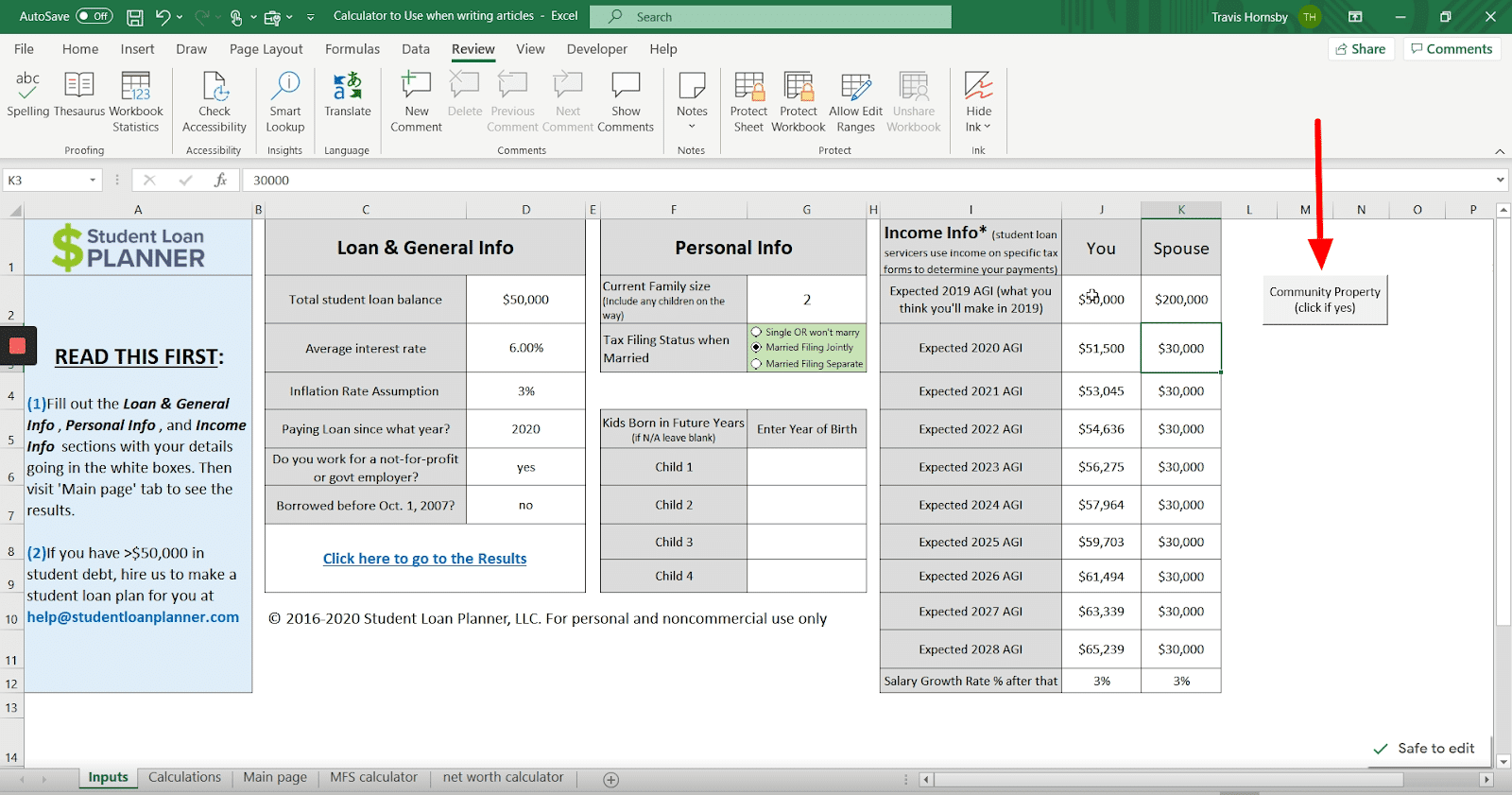

In the event you dwell in a group property state and questioning which submitting standing is greatest, you should use the Student Loan Planner® calculator that will help you resolve.

Contained in the calculator, you may choose whether or not or not you reside in a group property state. It then exhibits which compensation plan would prevent essentially the most cash.

Or, for those who’d like to speak to somebody who actually understands the ins and outs of scholar loans, contemplate booking a consultation with a Scholar Mortgage Planner® advisor.

Every of our advisors are CPA, CFP or CSLP licensed. They may also help you navigate the issues of scholar mortgage compensation for married {couples} in group property states.

Refinance scholar loans, get a bonus in 2021

$1,050 BONUS1For 100k+. $300 bonus for 50k to 99k.1

$1,000 BONUS2 For 100k or extra. $200 for 50k to $99,9992

$1,050 BONUS3For 100k+. $300 bonus for 50k to 99k.3

$1,275 BONUS4 For 150k+. Tiered 300 to 575 bonus for 50k to 149k.4

$1,000 BONUS5For 100k+. $300 bonus for 50k to 99k.5

$1,000 BONUS6For $100k or extra. $200 for $50k to $99,9996

$1,250 BONUS7 For 100k+ or $350 for 5k to 100k.7

$1,250 BONUS8For 150k+. Tiered 100 to 400 bonus for 25k to 149k.8

Unsure what to do along with your scholar loans?

Take our 11 query quiz to get a personalised advice of whether or not you must pursue PSLF, IDR forgiveness, or refinancing (together with the one lender we predict might provide the greatest fee).

All charges listed above symbolize APR vary. 1Commonbond: In the event you refinance over $100,000 by this website, $500 of the money bonus listed above is offered instantly by Scholar Mortgage Planner. Commonbond disclosure. 2Earnest: $1,000 for $100K or extra, $200 for $50K to $99.999.99. For Earnest, for those who refinance $100,000 or extra by this website, $500 of the $1,000 money bonus is offered instantly by Scholar Mortgage Planner. Fee vary above consists of non-obligatory 0.25% Auto Pay low costEarnest disclosures.

3Laurel Street: In the event you refinance greater than $250,000 by our hyperlink and Scholar Mortgage Planner receives credit score, a $500 money bonus can be offered instantly by Scholar Mortgage Planner. If you’re a member of knowledgeable affiliation, Laurel Street would possibly give you the selection of an rate of interest low cost or the $300, $500, or $750 money bonus talked about above. Gives from Laurel Street can’t be mixed. Fee vary above consists of non-obligatory 0.25% Auto Pay low cost. Laurel Road disclosures.

4Elfi: In the event you refinance over $150,000 by this website, $500 of the money bonus listed above is offered instantly by Scholar Mortgage Planner. Elfi disclosure. 5Splash: In the event you refinance over $100,000 by this website, $500 of the money bonus listed above is offered instantly by Scholar Mortgage Planner. Splash disclosure. 6Sofi: In the event you refinance $100,000 or extra by this website, $500 of the $1,000 money bonus is offered instantly by Scholar Mortgage Planner. Fee vary above consists of non-obligatory 0.25% Auto Pay low cost. Sofi disclosures. 7Credible: In the event you refinance over $100,000 by this website, $500 of the money bonus listed above is offered instantly by Scholar Mortgage Planner. Credible disclosure.

8LendKey: In the event you refinance over $150,000 by this website, $500 of the money bonus listed above is offered instantly by Scholar Mortgage Planner. Fee vary above consists of non-obligatory 0.25% Auto Pay low cost.

[ad_2]

Source link

{kind=link}