[ad_1]

Getting a Grasp of Enterprise Administration (MBA) can open doorways to your profession. That is very true for those who graduated from one of many top-ranking enterprise faculties. The one downside is you most likely shelled out $70,000 or extra per yr for tuition.

With numbers like these, it’s vital to know the methods for paying off MBA scholar loans. MBA student loan refinance is one method to take care of all of that debt. However you is likely to be stunned to study your different choices.

Quantity of debt from MBA scholar loans

Since 2005, graduate college students have been capable of borrow as much as the complete price of attendance in Grad PLUS Loans. This primarily has given graduate diploma applications, like MBA applications, clean checks to obtain 100% federal monetary assist for no matter they cost.

With this in thoughts, it ought to be no shock that tuition costs at graduate applications have massively elevated in recent times which has additionally led to extra graduate scholar mortgage debt. In a 2018 Bloomberg survey, half of the MBA grads from the perfect enterprise faculties had been borrowing at the least $100,000.

PayScale studies that the common MBA grad makes $90,125. It wouldn’t be correct to take this quantity and handle MBA debt payoff, because the profession paths are too assorted for this diploma. For instance, a monetary analyst makes a median of $65,000 whereas a Chief Monetary Officer (CFO) makes a median of $151,000.

Pupil mortgage refinancing for MBA loans would possibly work for the CFO however not the monetary analyst. Your scholar mortgage debt payoff technique will should be particular to your present wage and profession targets.

MBA scholar mortgage refinancing vs federal mortgage consolidation

In the event you took out a number of scholar loans throughout your undergraduate and graduate research, there are two methods which you can consolidate them into one mortgage. The primary possibility is by taking out a Direct Consolidation Mortgage with the Division of Schooling. The second approach is by refinancing with a private lender.

Every possibility has its personal set of execs and cons. In the event you’re solely seeking to simplify cost and alter servicers, federal consolidation stands out as the method to go. All Direct Mortgage debtors qualify no matter their credit score rating. And by protecting your MBA loans with the Schooling Division, you’ll stay eligible for federal advantages.

Nonetheless, the one draw back to federal consolidation is which you can’t use it to decrease your rate of interest. So even when you have a strong credit score report and low debt-to-income ratio, you gained’t be capable of get a extra enticing price.

That is the place refinancing is available in. Whereas non-public lenders can match all the versatile compensation choices supplied by federal scholar loans, they could supply considerably decrease rates of interest. So when you have six-figures of MBA scholar debt, refinancing might prevent tens of hundreds of {dollars} in curiosity funds over the lifetime of your mortgage.

When MBA scholar mortgage refinance is an effective possibility

Refinancing scholar loans may be accomplished on-line or at your native financial institution or credit score union. The lender pays off your scholar loans and points you a brand new non-public scholar mortgage. You then have one cost and new mortgage phrases.

When refinancing, the objective is often to aggressively repay your loans. This implies along with a decrease rate of interest, you may additionally wish to go for a shorter mortgage compensation time period to repay your loans as quickly as doable.

The onerous half is deciding if refinancing MBA loans will truly work to your scenario. You probably have non-public scholar loans, then refinancing for a better rate is at all times one thing you wish to examine. However federal scholar loans are one other story.

Professionals and cons of federal MBA scholar mortgage refinance

With federal scholar loans, there are some normal execs and cons of refinancing your scholar loans. The professionals of refinancing your MBA loans are as follows:

- You can save on curiosity funds. The Direct Unsubsidized Mortgage curiosity for graduate college students is 5.28%. The charges on Grad PLUS Loans and Mum or dad PLUS loans are increased at 6.28%. Refinancing your scholar loans might get you a a lot decrease price.

- You’ll have only one month-to-month cost to handle.

A greater rate of interest means extra money in your pocket. One cost means it’s simpler to take care of, however that doesn’t imply you gained’t miss a number of issues. The cons of refinancing your MBA scholar loans are as follows:

- You’ll lose federal borrower protections, similar to deferment and forbearance.

- You gained’t give you the chance to enroll in an income-driven compensation (IDR) plan.

- You’ll need to undergo a credit score verify and might want to have a superb credit score rating and meet different eligibility necessities to qualify for the perfect charges.

From this normal recommendation, it sounds such as you nonetheless can save extra money by refinancing your MBA loans into non-public loans. However there’s a cost hack that solely applies to federal loans that would align higher along with your profession targets. Let’s check out an instance of when sticking along with your federal loans, even at a better rate of interest, might prevent cash.

Don’t refinance your MBA scholar loans till you evaluate this hack

As talked about above, MBA salaries range considerably. It’s each your revenue and your scholar mortgage quantity that can decide if refinancing is a good suggestion or not.

The hack is protecting your federal scholar loans and enrolling within the Revised Pay As You Earn (REPAYE) compensation plan. REPAYE is without doubt one of the 4 IDR plans. The benefit of REPAYE is that the federal government truly helps with the curiosity.

In case your month-to-month cost doesn’t cowl the curiosity, the federal government can pay all of your curiosity for as much as three years on sponsored loans, then half for one more three years. Underneath REPAYE, the federal government can even pay half of the curiosity due in your unsubsidized loans.

Case research #1

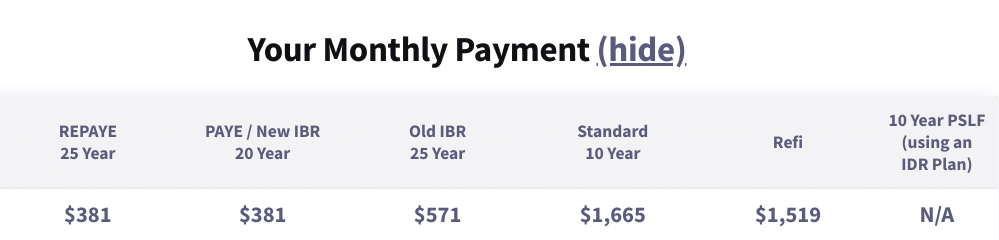

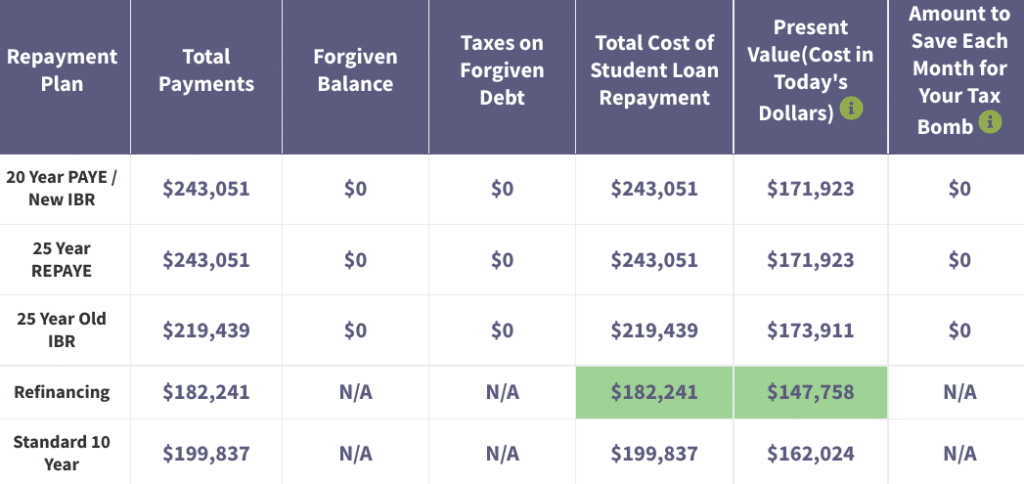

Let’s take a look at how this might play out for 2 totally different situations utilizing the numbers talked about above. In the event you left a high enterprise faculty with $150,000 of scholar mortgage debt and have become a monetary analyst making $65,000 in your first yr working, you’re going to wish to go together with PAYE or REPAYE.

In case your common federal rate of interest is 6% and also you’re single, your month-to-month funds could be round $415. That’s greater than $1,100 lower than you’d pay with the 10-12 months Normal Compensation Plan and over $1,200 lower than your month-to-month cost after refinancing at 4%. That’s an enormous quantity of additional month-to-month money move!

From right here, you may have two choices shifting ahead:

- Go for scholar mortgage forgiveness: After 25 years, your remaining scholar mortgage stability will likely be forgiven by way of the IDR forgiveness program. You’ll must pay taxes on the forgiven quantity, so put together for that.

- Refinance after incomes extra later: In the event you transfer up the pay scale in a number of years, you’ll be able to refinance your MBA loans then. Since half the curiosity is paid for, your mortgage stability gained’t have grown as quickly. With a better revenue down the road, you might be able to aggressively pay your loans off. This could be a good possibility for a grad who’s an entrepreneur or works at a startup.

In the event you go the standard route along with your MBA and land a profession that pays six figures or extra, it’s going to make extra sense to your money move to refinance your scholar loans.

Case Examine #2

Now let’s say you turn out to be a CFO with an $150,000 wage and the identical scholar mortgage stability of $150,000. You’ll be able to repay your loans in 10 years after which reallocate these funds towards your future investments. By refinancing, you’ll repay your debt quicker and save tens of hundreds of {dollars} in curiosity alongside the best way.

The final rule to observe for refinancing is that this: In the event you owe lower than 1.5 instances your revenue, refinance and pay your loans off aggressively. However for those who owe greater than that, join an IDR plan to make your funds extra manageable.

There’s additionally an exception to each rule. Most MBA program grads work within the non-public sector. But when that’s not you, don’t refinance in any respect. In the event you work at a not-for-profit or authorities company, you possibly can qualify for complete mortgage forgiveness by way of Public Service Loan Forgiveness after 10 years of funds on an IDR plan. In the event you qualify, this could be a higher compensation possibility than refinancing or REPAYE.

Do you have to pursue an MBA scholar mortgage refinance?

If you’re refinancing your MBA federal scholar loans, you’ll wish to evaluate your money move wants and your profession targets. In the event you’ll be working within the non-public sector and anticipate to be making six figures in a brief time frame, refinancing may very well be the proper transfer.

In the event you do determine to pursue refinancing, ensure that to compare several private lenders earlier than making a choice. In any case, you’ll wish to guarantee that the lender doesn’t cost an origination payment or prepayment penalty.

However you’ll wish to search for different advantages as effectively, similar to a proper forbearance coverage, an autopay low cost, and versatile compensation phrases. And needless to say a number of scholar mortgage refinance corporations are at present providing generous cash bonuses as effectively. Listed below are a number of of our favourite refinance lenders:

In the event you need assistance deciding whether or not you need to refinance your MBA scholar loans, reach out to a consultant on our team. Pupil Mortgage Planner® focuses on serving to individuals with over six figures of scholar mortgage debt. We are able to create a plan for you based mostly in your particular person scenario and wage.

Refinance scholar loans, get a bonus in 2021

$1,050 BONUS1For 100k+. $300 bonus for 50k to 99k.1

$1,250 BONUS2 For 250k+, tiered 300 to 500 bonus for 50k to 250k.2

$1,000 BONUS3 For 100k or extra. $200 for 50k to $99,9993

$1,275 BONUS4 For 150k+. Tiered 300 to 575 bonus for 50k to 149k.4

$1,000 BONUS5For $100k or extra. $200 for $50k to $99,9995

$1,250 BONUS6 For 100k+ or $350 for 5k to 100k.6

$1,250 BONUS7For 150k+. Tiered 100 to 400 bonus for 25k to 149k.7

Undecided what to do along with your scholar loans?

Take our 11 query quiz to get a personalised advice of whether or not you need to pursue PSLF, IDR forgiveness, or refinancing (together with the one lender we predict might provide the finest price).

All charges listed above signify APR vary. 1Commonbond: In the event you refinance over $100,000 by way of this website, $500 of the money bonus listed above is offered straight by Pupil Mortgage Planner. Commonbond disclosure.

2Laurel Highway: In the event you refinance greater than $250,000 by way of our hyperlink and Pupil Mortgage Planner receives credit score, a $500 money bonus will likely be offered straight by Pupil Mortgage Planner. In case you are a member of an expert affiliation, Laurel Highway would possibly give you the selection of an rate of interest low cost or the $300, $500, or $750 money bonus talked about above. Provides from Laurel Highway can’t be mixed. Price vary above consists of elective 0.25% Auto Pay low cost. Laurel Road disclosures.3Earnest: $1,000 for $100K or extra, $200 for $50K to $99.999.99. For Earnest, for those who refinance $100,000 or extra by way of this website, $500 of the $1,000 money bonus is offered straight by Pupil Mortgage Planner. Price vary above consists of elective 0.25% Auto Pay low costEarnest disclosures.

4Elfi: In the event you refinance over $150,000 by way of this website, $500 of the money bonus listed above is offered straight by Pupil Mortgage Planner. Elfi disclosure. 5Sofi: In the event you refinance $100,000 or extra by way of this website, $500 of the $1,000 money bonus is offered straight by Pupil Mortgage Planner. Price vary above consists of elective 0.25% Auto Pay low cost. Sofi disclosures. 6Credible: In the event you refinance over $100,000 by way of this website, $500 of the money bonus listed above is offered straight by Pupil Mortgage Planner. Credible disclosure.

7LendKey: In the event you refinance over $150,000 by way of this website, $500 of the money bonus listed above is offered straight by Pupil Mortgage Planner. Price vary above consists of elective 0.25% Auto Pay low cost.

[ad_2]

Source link

{kind=link}