[ad_1]

Our purpose is to provide the instruments and confidence you should enhance your funds. Though we obtain compensation from our companion lenders, whom we’ll all the time determine, all opinions are our personal. Credible Operations, Inc. NMLS # 1681276, is referred to right here as “Credible.”

Paying your mortgage biweekly is a method that may scale back your principal stability quicker and lower your whole curiosity prices, permitting you to personal your own home debt-free sooner. Nevertheless, it won’t be as efficient as you suppose due to how mortgage servicers can deal with additional funds.

Right here’s what you should learn about biweekly mortgage funds:

How biweekly mortgage funds work

Once you pay your mortgage biweekly, you pay half of your month-to-month principal and curiosity each two weeks. Which means that you’ll make 26 funds per yr — the equal of 13 month-to-month funds. So, for those who usually make 12 funds of $2,000 every yearly, you’d as an alternative change to creating 26 funds of $1,000 every.

In case your lender instantly applies every cost, you’ll pay down your principal considerably quicker, which suggests you’ll accumulate much less curiosity.

Some lenders don’t settle for partial funds, so your lender won’t apply your biweekly funds as you make them. As a substitute, they’ll apply them as soon as a month.

Biweekly vs. month-to-month mortgage funds

Paying biweekly can prevent 1000’s of {dollars} in curiosity and lower the lifetime of your mortgage by a number of years.

The desk beneath exhibits how a lot money and time you’ll be able to probably save by choosing biweekly mortgage funds vs. month-to-month mortgage funds. The instance assumes a mortgage stability of $200,000 with a 30-year time period and an APR of 4%.

| Biweekly | Month-to-month | |

|---|---|---|

| Mortgage cost | $477 | $955 |

| Time to repay | 25 years | 30 years |

| Complete curiosity you’ll pay | $120,360 | $143,739 |

| Complete curiosity financial savings | $23,379 | None |

Biweekly mortgage funds and your mortgage phrases

When you took out your mortgage in the previous couple of years, you acquired a type known as the closing disclosure earlier than finalizing your mortgage. It has two necessary items of knowledge for anybody desirous about biweekly funds.

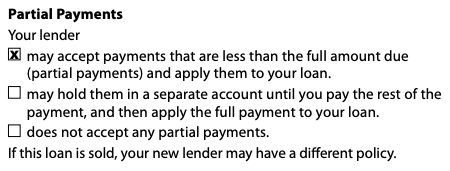

1. Partial funds

1. Partial funds

This part on Web page 4 says whether or not your lender will:

- Settle for partial funds which might be lower than your month-to-month cost quantity and apply them to your mortgage

- Settle for partial funds however maintain them till you make the remainder of your month-to-month cost

- Not settle for partial funds

Discover Out: How to Find the Best Mortgage Lender

2. Prepayment penalty

2. Prepayment penalty

This part on Web page 1 says whether or not your lender can cost you a payment for repaying your mortgage earlier than its scheduled maturity date.

For instance, it would say that you can owe as much as $3,000 for those who repay the mortgage in the course of the first two years, which might occur for those who refinanced or offered.

Nevertheless, it’s best to be sure your mortgage phrases don’t stipulate any early payoff payment — notably in case your mortgage got here previous to 2014 — that might negate the financial savings you’re attempting to attain with biweekly funds.

Execs and cons of paying your mortgage biweekly

Whereas the potential financial savings of biweekly funds is likely to be attractive, there are drawbacks that would make this cost technique much less worthwhile to you.

Execs

- Get monetary savings on curiosity: The upper your mortgage rate of interest, the extra it can save you by making biweekly funds.

- Repay your mortgage sooner: When you make biweekly funds from the start of a 30-year mortgage, you’ll be able to probably pay it off in 25 years.

- Match your mortgage funds together with your work paydays: You might have a neater time managing your month-to-month money movement for those who intently coordinate your earnings and bills.

Cons

- Much less cash for different issues: Placing more money towards your mortgage has a possibility value. Directing that money to your scholar loans, bank cards, and/or retirement financial savings might profit you extra in the long term.

- Prices additional to get the cash again: Sure, you construct home equity quicker whenever you make additional principal funds. But when you find yourself having to re-borrow that cash via a house fairness mortgage or cash-out refinance, you’ll set your self again. Not solely will you draw down your fairness, however you could pay borrowing charges and the next rate of interest on the brand new mortgage.

- Funds may truly be utilized month-to-month: Mortgage servicers received’t essentially apply your funds to your account each two weeks. As a substitute, they’ll typically maintain the primary cost till you make the second cost, then apply each funds collectively to your full month-to-month mortgage cost. You’ll nonetheless come out forward, however you’ll save much less curiosity and maintain your mortgage longer.

arrange biweekly mortgage funds

Some mortgage servicers supply their very own biweekly mortgage cost plans, giving debtors a transparent technique to make extra frequent funds. You can even simply deal with biweekly funds your self, which can have added benefits.

By your mortgage servicer

Test your mortgage servicer’s web site for details about biweekly cost choices. They might require you to be one month forward in your mortgage earlier than enrolling in a biweekly cost plan.

On prime of that, your mortgage servicer’s plan might not even apply the funds to your account each two weeks. For instance, Caliber Dwelling Loans states that the one advantage of enrolling in a biweekly cost program is that your thirteenth and twenty sixth funds every year might be utilized to your principal stability, lowering what you owe quicker.

What’s worse, trusting these third events together with your cash units you as much as get scammed and fall behind in your mortgage.

By your self

Dealing with biweekly funds your self provides you essentially the most management over the method and is totally free.

Once you log in to your mortgage account, your servicer might present the choice to make an additional principal cost so long as you’re present in your mortgage.

Divide your month-to-month mortgage cost by 26 to get the quantity of additional principal it’s best to pay each two weeks. Maintain making your month-to-month mortgage funds in full, as traditional.

Managing biweekly funds your self additionally lets you simply change again to month-to-month funds at any time with out contacting your mortgage servicer.

Make certain to test the field on the cost web page or in your cost slip indicating whenever you’re paying additional principal.

Different methods to cut back your principal stability quicker

Apart from making biweekly mortgage funds, there are different methods you should utilize to pay down your principal quicker.

Refinance to a shorter mortgage time period

Finest if: Refinancing will considerably decrease your rate of interest

Refinancing to a shorter mortgage time period solely makes monetary sense in case your rate of interest financial savings will exceed the closing costs in your new mortgage. The less months it’ll take so that you can acquire this profit, the higher, however your breakeven level ought to positively be earlier than whenever you anticipate to promote your own home.

When you’re able to refinance, Credible makes the entire course of straightforward. You’ll be able to examine a number of lenders and see prequalified refinance rates in as little as three minutes with out leaving our platform.

Find My Refi Rate

Checking charges won’t have an effect on your credit score

Study Extra: How to Refinance Your Mortgage in 6 Easy Steps

Make additional funds each quarter

Finest if: Your money movement is irregular

Biweekly mortgage funds will be logical for individuals who get a gradual paycheck each two weeks. However for those who’re a small enterprise proprietor or impartial contractor, your earnings can range quite a bit within the quick run.

Making an additional mortgage cost every quarter — as an alternative of each two weeks — may higher align your earnings together with your bills whereas nonetheless permitting you to avoid wasting on curiosity and repay your mortgage sooner.

Recast your mortgage

Finest if: You need to apply a big lump sum to your mortgage principal

When a lender recasts your mortgage after you make a further lump sum cost towards your principal, you’ll get a decrease month-to-month cost with out having to refinance. You received’t repay your mortgage quicker, as a result of your mortgage time period will keep the identical.

Your rate of interest may also keep the identical, however you’ll lower your expenses on curiosity since you owe much less principal. Your lender might cost just a few hundred {dollars} to recast your mortgage, however refinancing often prices a number of thousand {dollars}.

Study Extra: How to Pay Off Your Mortgage Early

In regards to the creator

[ad_2]

Source link

{kind=link}