[ad_1]

Our objective is to provide the instruments and confidence it’s worthwhile to enhance your funds. Though we obtain compensation from our accomplice lenders, whom we are going to at all times determine, all opinions are our personal. Credible Operations, Inc. NMLS # 1681276, is referred to right here as “Credible.”

Credit score is likely one of the primary elements of qualifying for a mortgage — and whereas some consumers have constructed a protracted credit score historical past, others are simply getting began. First-time homebuyers are much less more likely to have credit score, which suggests they might face challenges getting a mortgage.

Should you’re on this place, don’t fret, it’s nonetheless doable to purchase a home with no credit score. You’ll simply want to point out you may afford the upfront prices and month-to-month mortgage funds.

Right here’s methods to get a mortgage with no credit score historical past:

What’s credit score?

Credit score is the power to borrow cash if you want it. Should you’ve heard folks speak about constructing credit score, they imply taking steps to point out you usually pay again the cash you borrow as agreed.

There are three main items to your credit score, and understanding how they match collectively may help you qualify for a mortgage.

Credit score historical past

Your credit score historical past is a file of any loans or bank cards you’ve taken out prior to now. Mortgage lenders evaluate your credit score historical past to see what kinds of credit score you’ve taken out and the way you’ve dealt with that debt.

They use that data to foretell whether or not you’ll repay your mortgage mortgage sooner or later.

Credit score report

The small print of your credit score historical past are captured in your credit score stories. These paperwork might embrace:

- Every credit score account you’ve taken out, together with the kind of account

- A historical past of every cost you’ve made and whether or not they have been on time

- The reported account stability

- Public data, corresponding to foreclosures and bankruptcies

You possibly can entry your credit score stories at AnnualCreditReport.com, or by going by way of the three main credit score bureaus: Experian, TransUnion, and Equifax. These corporations accumulate details about your accounts and add the small print to your credit score stories.

Credit score rating

Credit score-scoring corporations usually scan your credit score stories and use the data to calculate your credit score scores. The key credit score scores, corresponding to FICO, vary from 300 to 850. Usually, a better rating may help you purchase a house with a superb rate of interest.

There’s a special minimal credit score rating requirement for each mortgage program. Right here’s a fast overview:

| Mortgage sort | Min. credit score rating |

|---|---|

| Typical | 620 |

| FHA | 500 |

| VA | None |

| USDA | None |

Be taught Extra: 5 Forms of Mortgage Loans: Which One Is for You?

No credit score vs. bad credit report: What’s the distinction?

When you have no credit score, it means your credit score stories lack sufficient latest data to calculate a credit score rating. This is called having a “skinny credit score file” or being “credit score invisible.”

This may occasionally occur if:

- You’ve by no means utilized for a mortgage or bank card

- You’ve borrowed cash however your collectors don’t report your account data to the credit score bureaus

- You paid off your loans greater than two years in the past and haven’t opened new accounts

With a skinny credit score file, collectors don’t have a great way to foretell how probably you might be to repay your debt. The federal authorities estimates 1 in 10 adults lacks a credit score historical past with the three primary credit score bureaus.

Tip: Having no credit score is completely different from having bad credit report, which suggests your credit score historical past accommodates blemishes. This may occur in case you’ve missed mortgage or bank card funds, otherwise you’ve taken on a whole lot of debt.

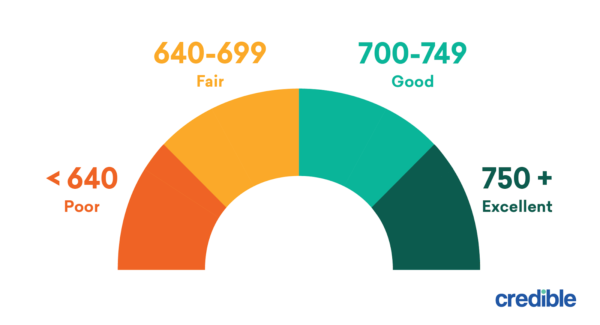

Usually, an individual with a credit score rating of 640 or decrease is taken into account to have unhealthy or poor credit score — right here’s what the usual credit score rating ranges seem like:

Main unfavorable occasions, corresponding to foreclosures and bankruptcies, can significantly bruise your credit score, too. Lenders may see a low credit score rating as a warning signal that you could be default in your mortgage funds sooner or later.

The right way to get a mortgage with no credit score

Potential homebuyers with out in depth credit score histories nonetheless have choices for getting a house mortgage.

Purchasing round for a mortgage could be annoying. Happily, Credible simplifies this course of and makes evaluating a number of lenders simple.

You possibly can see prequalified charges from our accomplice lenders and generate a streamlined pre-approval letter in just some minutes.

Discover Charges Now

Take into account a government-insured mortgage

A government-insured mortgage is a house mortgage backed by the federal authorities. FHA loans are backed by the Federal Housing Administration and include versatile credit score necessities.

This mortgage program usually requires debtors to have a credit score rating of at the least 500. However as an alternative of utilizing a standard credit score report, lenders can request a “non-traditional merged credit score report” from a credit score reporting firm.

Or the lender can develop a credit score historical past utilizing different tradelines, corresponding to:

- Utility cost data, together with cellphone payments

- Residence rental funds

- Automotive insurance coverage funds

- Funds to baby care suppliers

- Hire-to-own companies

- 12 months’ price of financial savings deposits

- A automobile lease

- A private mortgage with compensation phrases in writing

Downsides: All FHA loans include mortgage insurance coverage premiums, which will increase your month-to-month funds.

Undergo handbook underwriting

When a mortgage software goes by way of handbook underwriting, an underwriter personally opinions the applying as an alternative of an automatic system. Should you’re making use of for a standard mortgage, the underwriter checks that you just:

- Have the funds to make a down cost

- Earn sufficient revenue to cowl the mortgage funds

- Have a suitable debt-to-income (DTI) ratio

- Have money reserves in your checking account

In lieu of a standard credit score historical past, be ready at hand over these paperwork to point out a observe file of creating on-time funds:

- Hire funds for the earlier two years

- Utility and cellphone funds

- Funds for different recurring bills

Downsides: Some lenders received’t manually underwrite a mortgage due to the additional time and expense concerned. Lenders keen to do that might cost a better rate of interest.

Apply with a co-borrower

Another choice is to use with a co-borrower who has a powerful credit score historical past. The co-borrower is usually a partner, relative, or buddy, they usually don’t need to dwell within the dwelling.

The lender would come with that particular person on the mortgage and base the mortgage qualification on their revenue and credit score rating. You and the co-borrower are equally liable for making mortgage funds, and also you each could be included on the property title.

Downsides: To qualify for a house mortgage, you might need to take out a smaller mortgage than you’d have with two borrower incomes.

The right way to construct credit score

Whereas it’s doable to get a home mortgage with no credit score, the method is simpler when you may have a superb credit score rating.

Should you determine to place off the acquisition for a couple of months, work on constructing credit score to enhance your probabilities of qualifying for a house mortgage. Listed below are some methods to take action:

- Develop into a licensed consumer. When a trusted buddy or relative provides you to certainly one of their bank card accounts, the bank card issuer stories the account as a part of your credit score historical past. You received’t be liable for paying the fees, and also you profit from their credit score historical past.

- Take out a secured bank card. A secured bank card works the identical as an unsecured bank card, besides you provide a safety deposit upfront. Making on-time funds and retaining your stability low may help you construct a constructive credit score historical past. This could possibly be a superb choice in case you can’t discover somebody who will add you as a licensed consumer.

- Apply for a credit-builder mortgage. Some credit score unions supply small loans particularly to assist folks construct credit score. As an alternative of getting the cash upfront, the monetary establishment places it in a financial savings account. You’ll construct credit score over a number of months or a few years as you make on-time funds. On the finish of the mortgage time period, you’ll obtain the funds.

- Discover a creditworthy co-signer. Whenever you get a co-signer, that particular person agrees to make your mortgage funds for you in case you can’t. This might assist you qualify for the mortgage and get a decrease rate of interest, too. Nevertheless, the co-signer ought to perceive the dangers concerned earlier than signing on. They’ll be equally liable for repaying any debt.

Preserve Studying: 10 Errors to Keep away from as a First-Time Homebuyer

Concerning the creator

[ad_2]

Source link

{kind=link}