[ad_1]

Refinancing could be a good way to scale back your rate of interest and the price of your pupil mortgage pay-back. It’s a course of the place you are taking your federal pupil loans or your present personal pupil loans and change them with a brand new personal mortgage to decrease your rate of interest and/or change your mortgage phrases.

However what if, as a consequence of your credit score, you don’t get authorised for an rate of interest decrease than a few of your present rates of interest?

“Does it make sense to refinance a part of my pupil loans?” I get this query all. the. time. The quick reply is sure. However do you have to? Let’s dissect it.

NOTE: Refinancing is completely different from consolidation. A Direct Consolidation Mortgage combines a number of federal schooling loans into one federal mortgage, protecting them throughout the federal system. Consolidation doesn’t enhance your rate of interest, nevertheless it doesn’t actually make the rate of interest worse both. Consolidation takes the weighted common of your present loans and rounds as much as the closest 1/eighth of a %.

When of us graduate, they often have a laundry listing of loans since monetary help is issued every semester. For federal loans, you too can have two various kinds of loans issued every semester as seen on the mortgage file under.

While you borrow federal loans, you lock in a hard and fast rate of interest which received’t change over the lifetime of the mortgage (except you refinance or consolidate sooner or later), however every following yr the rate of interest can change as you proceed to borrow. Rates of interest on federal pupil loans aren’t set by the U.S. Division of Training — they’re set by federal regulation, yearly.

Within the mortgage file above, rates of interest vary from as little as 3.4% all the way in which to 7.21%. If this individual consolidated, their weighted common rate of interest could be 6.14% which is rounded as much as the closest 1/eighth of a %. Their remaining rate of interest could be 6.25%.

One would possibly say, “Wow that’s a excessive rate of interest… you need to refinance!” However not so quick — pupil mortgage reimbursement planning isn’t simply in regards to the rate of interest.

This individual has $152,000 of federal pupil mortgage debt and has been on PAYE since 2016. They make $62,000 per yr and are married, however filing taxes separately, to maintain the fee off of their very own revenue:

Persevering with the taxable forgiveness route on PAYE is perfect. If this individual refinanced and lowered their rate of interest right down to 4%, their month-to-month fee would greater than triple they usually’d pay a complete value of $49,669 MORE than in the event that they’d keep on PAYE and save for the tax bomb.

I’ll say it once more: it’s not simply in regards to the rate of interest.

However does it make sense to refinance high-interest student loans solely? Let’s tease this thought out. Let’s say we refinanced the entire loans over 6.5%, and saved the remaining federal.

The loans over 6.5% totaled to $59,091, leaving $93,037 left. If we stayed on PAYE with these, the next would play out:

PAYE remains to be the optimum path for the remaining federal loans however you’ll discover that the “Complete Funds” column (the overall month-to-month funds made between now and forgiveness) is the very same whole as our authentic path keping all of the loans federal. The tax bomb adjustments, however not how a lot they pay into the federal system.

How can that be? This individual would nonetheless be on tempo for the taxable mortgage forgiveness and PAYE retains their fee primarily based off of their revenue, not the steadiness or rate of interest in any respect. So not solely does refinancing not cut back the quantity they’re paying to the federal system, it additionally provides one other invoice into the equation:

In the event that they bought that rate of interest right down to 4% and caught to the identical timeline to repay the loans as PAYE would attain forgiveness, this individual would pay:

- $78,676 for his or her personal mortgage repay

- $59,974 into the federal system for his or her month-to-month PAYE funds

- $47,502 tax invoice for the forgiven steadiness on the federal loans in 2036

= $186,152 whole value

In comparison with a complete value of $152,880 on the primary instance, staying the course on PAYE for all of the loans.

This instance boils it down to 1 reality: in case you have federal loans and also you’re a transparent case for IDR or PSLF forgiveness, refinancing a few of your federal loans doesn’t profit you.

Let’s take a look at one other instance the place somebody is NOT a forgiveness case.

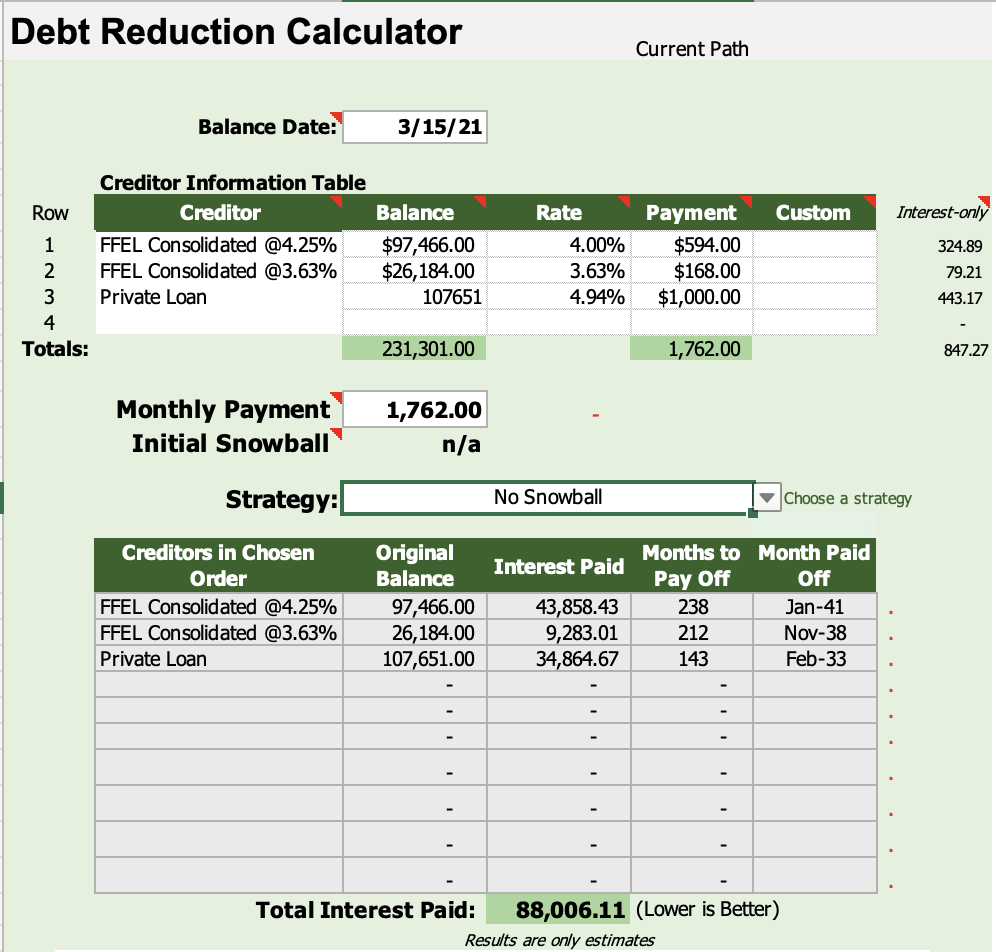

This subsequent individual has each federal loans (listed under) and personal loans at a complete of $107,651 at an rate of interest of 4.94%.

This individual wasn’t a superb candidate for long term forgiveness primarily based on their revenue so paying these off sooner quite than later is extra optimum. Their federal rates of interest are fairly darn good already although! What’s the plan of assault?

The straightforward reply is refinance and hope you get an rate of interest decrease than your entire present rates of interest — on this case, 3.63%. However what if this individual bought authorised for less than 4%?

You may cherry choose and maintain the three.63% loans out of the refinance to protect their decrease price however that might imply two completely different funds and two completely different pay-off timelines, presumably. And is it mathematically price it to maintain them out?

Let’s first set up what their present path seems like. In the event that they saved the course with no snowball (saved paying solely the month-to-month fee due on every mortgage till it was paid off):

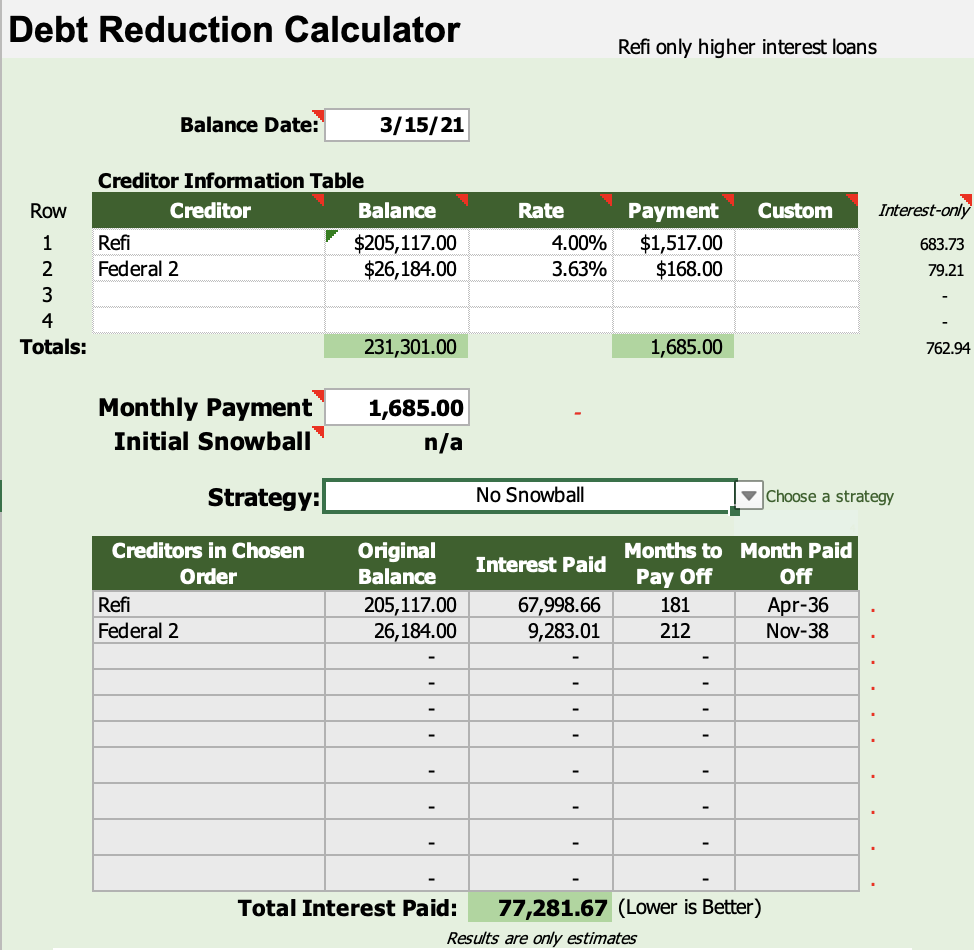

Let’s evaluate to in the event that they refinanced simply the loans that have been over 4% on a 15-year term (protecting the fee considerably akin to their present funds) with no snowball:

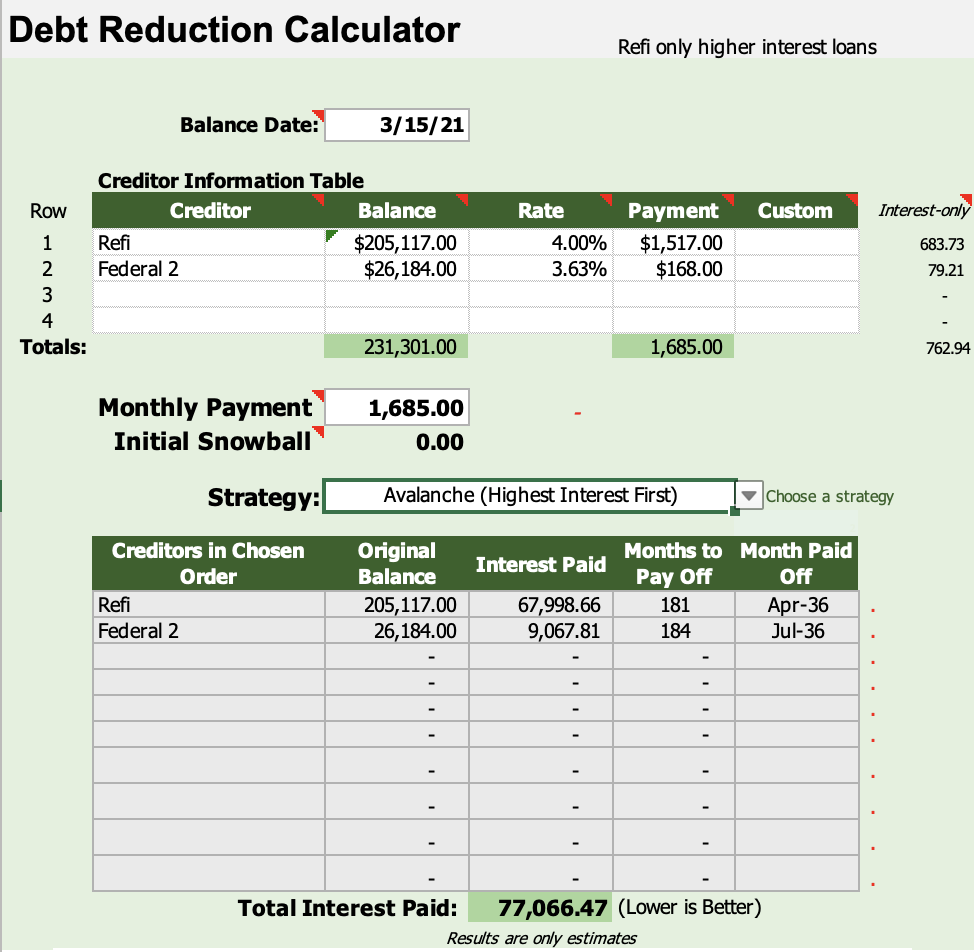

Positively an enchancment, saving them $10,724! However let’s take it a step additional assuming that when the refinanced mortgage was paid off, they’d then snowball their regular fee ($1517) into the federal loans to pay these off quicker:

A whopping $215 of financial savings, however shaved off a yr and ½ of time! Hmm. So let’s take it one other step additional and take a look at if we simply refinanced the whole lot collectively on the 4% rate of interest for a 15-year time period from the start:

Refinancing the whole lot from the start is extra optimum! So on this case, I might recommend simplicity and refinance the whole lot, even when we couldn’t get decrease than the bottom interest-rate loans.

A superb rule of thumb to make use of right here is discovering the weighted common rate of interest for the entire debt scenario, which on this case is 4.5%. Right here’s easy methods to calculate this:

So long as a refi rate of interest supply is decrease than the weighted common, inexperienced mild on refinancing the whole lot collectively. If not, that’s when cherry-picking would possibly make sense, leaving the decrease rates of interest out of the refinance and snowballing your funds as loans are paid off.

There’s clearly MANY methods to take a look at this however total keep in mind:

- In case your federal mortgage reimbursement path is forgiveness, it does NOT make sense to refinance any a part of your federal steadiness. This leads to paying greater than wanted.

- Typically, if the refinance supply is a decrease rate of interest than the present weighted common rate of interest of your entire loans, there’s not an enormous benefit to leaving the bottom curiosity loans out.

Need Assist Fixing Your Pupil Loans? We Can Assist Determine Out the Finest Path to Compensation

When you’ve made it via the entire article, kudos. Let our crew prevent a ton of time and doubtless some huge cash too and create a personalized pupil mortgage plan for you.

Check out how our student loan consult service may prevent 1000’s of {dollars} over the lifetime of your mortgage payback.

Refinance pupil loans, get a bonus in 2021

$1,000 BONUS1For 100k or extra. $200 for 50k to $99,999¹

$1,250 BONUS2For 250k+, tiered 300 to 500 bonus for 50k to 250k.2

$1,275 BONUS3For 150k+. Tiered 300 to 575 bonus for 50k to 149k.3

$1,000 BONUS4For $100k or extra. $200 for $50k to $99,9994

$1,050 BONUS5For 100k+. $300 bonus for 50k to 99k.5

$1,250 BONUS6For 100k+ or $350 for 5k to 100k.6

$1,250 BONUS7For 150k+. Tiered 100 to 400 bonus for 25k to 149k.7

Undecided what to do along with your pupil loans?

Take our 11 query quiz to get a customized suggestion of whether or not you need to pursue PSLF, IDR forgiveness, or refinancing (together with the one lender we predict may provide the greatest price).

1Earnest: $1,000 for $100K or extra, $200 for $50K to $99.999.99. For Earnest, for those who refinance $100,000 or extra via this web site, $500 of the $1,000 money bonus is offered instantly by Pupil Mortgage Planner. Fee vary above contains non-compulsory 0.25% Auto Pay low costEarnest disclosures. 2Laurel Highway: When you refinance greater than $250,000 via our hyperlink and Pupil Mortgage Planner receives credit score, a $500 money bonus shall be offered instantly by Pupil Mortgage Planner. If you’re a member of knowledgeable affiliation, Laurel Highway would possibly give you the selection of an rate of interest low cost or the $300, $500, or $750 money bonus talked about above. Presents from Laurel Highway can’t be mixed. Fee vary above contains non-compulsory 0.25% Auto Pay low cost. Laurel Road disclosures.3Elfi: When you refinance over $150,000 via this web site, $500 of the money bonus listed above is offered instantly by Pupil Mortgage Planner. Elfi disclosure. 4Sofi: When you refinance $100,000 or extra via this web site, $500 of the $1,000 money bonus is offered instantly by Pupil Mortgage Planner. Fee vary above contains non-compulsory 0.25% Auto Pay low cost. Sofi disclosures.5Commonbond: When you refinance over $100,000 via this web site, $500 of the money bonus listed above is offered instantly by Pupil Mortgage Planner. Commonbond disclosure. 6Credible: When you refinance over $100,000 via this web site, $500 of the money bonus listed above is offered instantly by Pupil Mortgage Planner. Credible disclosure.

7LendKey: When you refinance over $150,000 via this web site, $500 of the money bonus listed above is offered instantly by Pupil Mortgage Planner. Fee vary above contains non-compulsory 0.25% Auto Pay low cost.

[ad_2]

Source link

{kind=link}