[ad_1]

Our aim is to provide the instruments and confidence you’ll want to enhance your funds. Though we obtain compensation from our associate lenders, whom we’ll at all times determine, all opinions are our personal. Credible Operations, Inc. NMLS # 1681276, is referred to right here as “Credible.”

When you’re a house owner, refinancing can provide you an opportunity to economize with a decrease rate of interest, money in on your own home fairness, or modify your mortgage phrases. However the disadvantage is that your credit score rating might drop within the course of. The excellent news, although, is that your credit score can bounce again.

Right here’s what to find out about how mortgage refinancing impacts your credit score and how one can defend your funds within the course of:

How a mortgage refinance impacts your credit score

There are various kinds of credit score scores on the market, however most mortgage lenders use the FICO credit score rating to find out your credit score danger. Figuring out what would possibly trigger your FICO rating to drop will help you are expecting what is going to occur when you refinance.

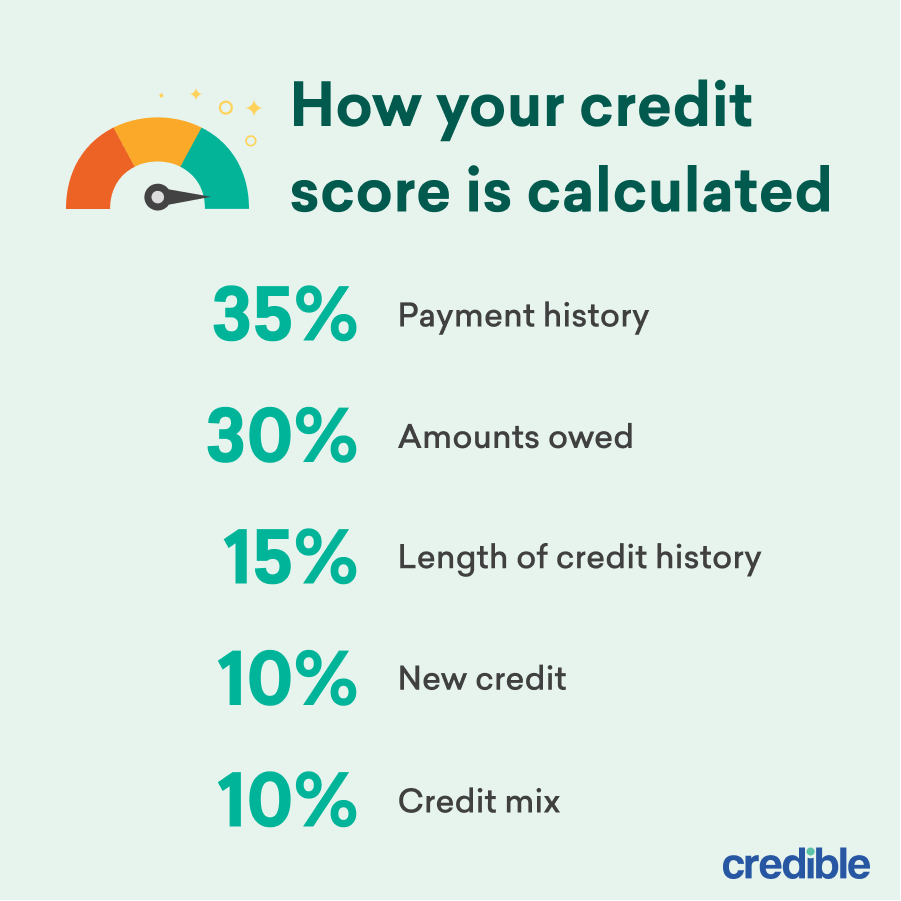

Right here’s how your rating is calculated, in response to FICO:

- Fee historical past: 35%

- Quantities owed: 30%

- Size of credit score historical past: 15%

- New credit score: 10%

- Credit score combine: 10%

Whenever you refinance, you’re taking out new credit score and altering the size of your credit score historical past — so each of those elements might be affected. Refinancing additionally would possibly change the quantity of debt you owe should you do a cash-out refinance.

Nevertheless, any credit score hit is more likely to be short-term and outweighed by the monetary advantages of refinancing.

Credible makes refinancing straightforward. You may take a look at your customized refinances rates from all of our associate lenders utilizing our on-line instruments. We additionally present transparency into lender charges that different comparability websites usually don’t.

Find My Refi Rate

Checking charges is not going to have an effect on your credit score

Whenever you apply: Exhausting credit score inquiries

Everytime you apply for credit score, together with a mortgage, the lender conducts a hard credit inquiry to see should you qualify for the product. The inquiry is recorded in your credit score stories and will briefly have an effect on your credit score scores.

New credit score accounts for 10% of your FICO rating. The credit-scoring firm says one inquiry might decrease your credit score scores by 5 factors, however a number of onerous inquiries might have a bigger impression.

After you shut: Eliminating an older debt

The size of your credit score historical past accounts for 15% of your FICO rating. Typically, older accounts will help you preserve wholesome credit score as a result of it exhibits lenders the way you’ve dealt with debt for an extended time period.

Whenever you refinance your mortgage, you shut an older mortgage and exchange it with a brand new one. That shortens the age of your common credit score account, which can decrease your credit score scores.

For cash-out refinances: Elevating your credit score utilization

Credit score utilization measures how a lot credit score you’re utilizing, and it accounts for 30% of a FICO credit score rating.

With a cash-out refinance, you are taking out a brand new mortgage for greater than you presently owe, repay the outdated mortgage, and maintain the additional money, minus the closing prices. However since you enhance the quantity of debt you’ve gotten, your credit score utilization ratio goes up, too.

Good to know: The next utilization might make your credit score scores drop. When you’re utilizing the money out of your cash-out refinance to pay down high-interest debt, although, refinancing might finally have a constructive impact in your rating.

Verify Out: How to Refinance Your Mortgage in 6 Easy Steps

5 methods to guard your credit score if you refinance

In the end, householders who can profit from refinancing shouldn’t be delay by the short-term credit score hit. When you’re contemplating this transfer, listed here are 5 steps you possibly can take to guard your credit score:

1. Make sure that it’s the proper time to refinance

When rates of interest drop, householders typically think about refinancing to avoid wasting on their month-to-month funds. Mortgage specialists say refinancing is smart should you can decrease your rate of interest by no less than 0.75%.

Because you’ll pay closing prices on a refinance, you also needs to think about whether or not you’ll stay within the residence lengthy sufficient to recoup that expense. For example, should you save $200 a month by refinancing however pay $4,000 in closing prices, it is going to take 20 months to interrupt even.

2. Verify your personal credit score earlier than you apply

Earlier than making use of for a refinance, it’s a good suggestion to pull your credit to verify whether or not you’d qualify for a brand new mortgage. This creates a tender inquiry, which gained’t impression your credit score.

The minimal credit score rating you want is determined by the mortgage program and your loan-to-value ratio, debt-to-income ratio, and money reserves.

In case your credit score scores want work, think about hitting the pause button in your mortgage functions. You may work on improving your credit and making use of for a refinance mortgage after a number of months.

3. House out your refinancing

Exhausting inquiries can stay in your credit score stories for 2 years, however FICO scores solely take note of inquiries from the final 12 months.

So should you refinanced just lately, think about ready no less than a 12 months earlier than you refinance once more. That method, the brand new spherical of credit score inquiries gained’t accumulate with the primary time you refinanced.

Preserve Studying: Just How Often You Can Refinance Your Home

4. Don’t open every other credit score accounts

Whereas you’ll have plans to purchase a brand new automobile and fill your own home with furnishings, it’s finest to keep away from utilizing credit score till after you shut on the refinance mortgage.

When you wait, maintain your credit score wholesome by paying all of your payments on time and tackling any high-interest debt. Keep away from opening or closing accounts.

5. Examine presents from a number of lenders

The easiest way to economize in your refinance is by submitting functions with a number of lenders and evaluating presents. Credible will help you with this.

The hot button is to time it proper. Credit score-scoring firms know shoppers store round, so a number of inquiries inside a sure time-frame might need a minimal impression in your rating.

FICO, for instance, considers all mortgage functions inside a 45-day window as only one inquiry. Take into account submitting all of your mortgage functions inside this window to restrict the hit to your credit score.

Discover Out: 4 of the Best Mortgage Refinance Companies

Concerning the writer

[ad_2]

Source link

{kind=link}