[ad_1]

Partial Monetary Hardship is a time period related to eligibility for the income-driven reimbursement (IDR) plans, Pay As You Earn (PAYE) and Revenue-Primarily based Compensation (IBR).

It sounds aggressive, however having a partial monetary hardship merely signifies that the cost calculated out of your discretionary income should be decrease than what your cost would’ve been on the Customary 10-year reimbursement plan.

What’s a partial monetary hardship?

Right here’s the technical definition from StudentAid.gov:

“Partial monetary hardship is an eligibility requirement beneath the Revenue-Primarily based Compensation (IBR) and Pay As You Earn Compensation (PAYE) plans. It’s a circumstance by which the annual quantity due in your eligible loans, as calculated beneath a 10-year Customary Compensation Plan, exceeds 15 p.c (for IBR) or 10 p.c (for Pay As You Earn) of the distinction between your adjusted gross revenue (AGI) and 150 p.c of the poverty line for your loved ones measurement within the state the place you reside.”

You have to have a partial monetary hardship to be accepted into PAYE or IBR initially, however you may’t be “kicked off” the plan in case your revenue will get to a degree the place you now not have a partial monetary hardship in a while.

What would occur is your cost would cap-out or cease at that Customary 10-year quantity, and that’ll be your cost going ahead except revenue decreases sooner or later. REPAYE however, doesn’t require a monetary hardship so your cost has no cap beneath this plan as your revenue will increase extra time.

Listed below are a number of often requested questions with regards to partial monetary hardship.

What if I don’t have a partial monetary hardship when making use of for PAYE or IBR?

While you apply for an income-driven repayment plan, the appliance hyperlinks again to your most just lately filed tax return to confirm revenue except your present revenue is decrease than what’s mirrored on that final tax return. If it’s decrease, various documentation is required reminiscent of a paystub or a suggestion letter to calculate your IDR cost.

Should you don’t have a partial monetary hardship whenever you apply for PAYE or IBR, your utility will likely be denied and your mortgage servicer will place you on an IDR plan with the bottom month-to-month cost quantity. REPAYE may possible be this subsequent choice as a result of the one eligibility requirement for REPAYE is having Direct Loans.

What occurs if I’m on PAYE or IBR and now not have a partial monetary hardship?

When you’re already on PAYE or IBR (or any income-driven plan for that matter), each 12 months you need to replace your revenue. This course of known as IDR recertification. In case your recertification generates a cost that exceeds the Customary-year reimbursement quantity subsequent time you recertify, your cost will cap-out at that quantity.

You’ll get a discover out of your servicer that claims you now not qualify on your income-driven reimbursement plan because you now not have a partial monetary hardship, BUT it might probably’t kick you off of the plan like I discussed earlier than.

The letter would possibly make you assume that you must swap reimbursement plans, however the actuality is you don’t need to, and the servicer can’t make you both.

Why would I keep on IBR or PAYE after hitting the cost cap?

I can consider two causes you’d wish to keep on IBR or PAYE, and so they each need to do with mortgage forgiveness.

1. Public Service Mortgage forgiveness (PSLF) is the largest purpose

The Customary 10-year cost, or on this case — your cost cap on account of now not having a partial monetary hardship — nonetheless counts towards the 120 payments for PSLF.

Leveraging the cost cap could be a extra environment friendly method to pursue Public Service Mortgage Forgiveness because it retains the cost from rising previous a sure level. The result’s that you simply’ll get to forgiveness paying much less cash towards your debt.

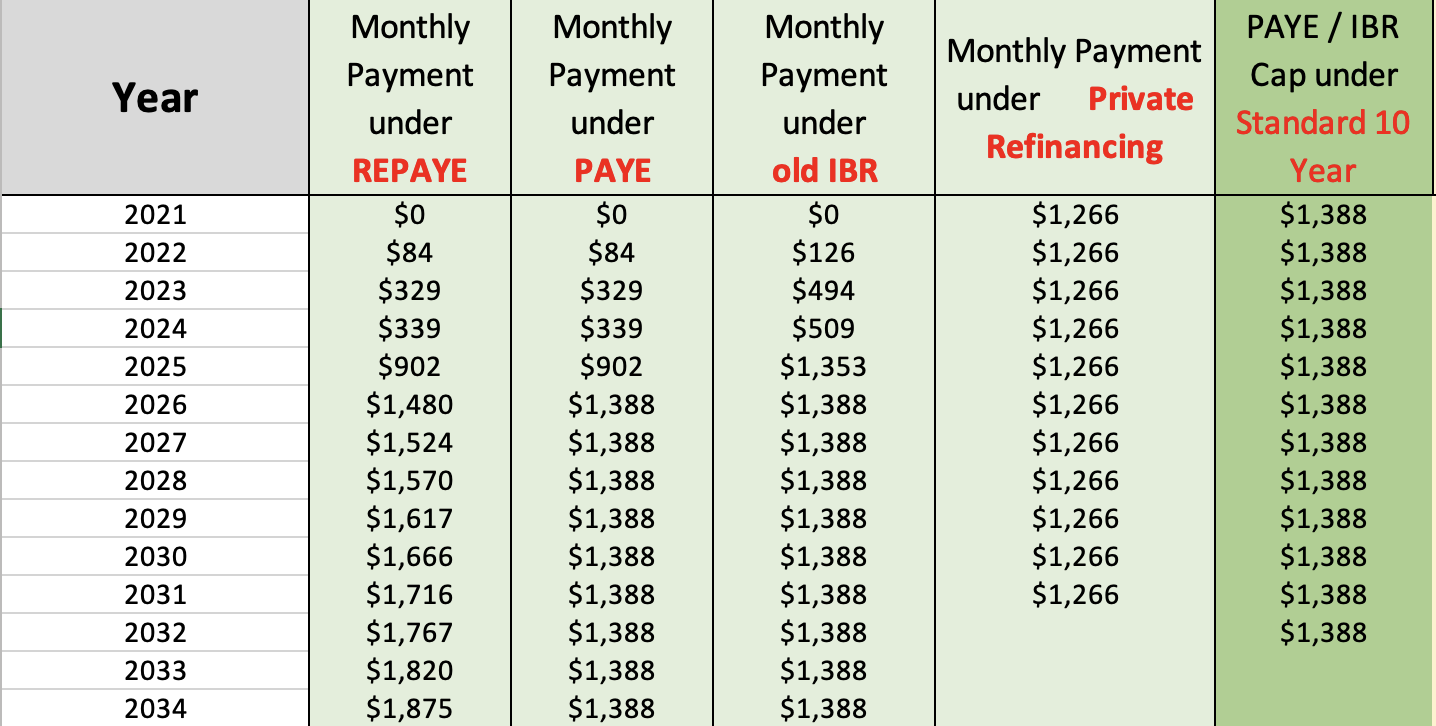

See an instance under of a new-graduate doctor who’s single with $125,000 of pupil debt and their AGI from their tax return prior to graduation was $0. This doctor has 4 years of residency with revenue at about $60,000 per 12 months. Afterward, their attending annual wage will likely be $200,000, all whereas working in a 501(c)(3) hospital setting that’s PSLF eligible.

When pursuing forgiveness, the objective is to pay as little as attainable to maximise how a lot debt is forgiven. PAYE and REPAYE are the least-expensive reimbursement plans, each primarily based on 10% of discretionary revenue, however REPAYE doesn’t have the partial monetary hardship requirement (i.e. cost cap).

This doctor is eligible for PAYE now, as a result of primarily based on their most up-to-date tax return on file, they meet the definition of getting a partial monetary requirement. Their cost’s lower than their customary 10-year cost cap of $1388 per thirty days. Their first 12 months of funds will truly be $0 per thirty days (which nonetheless counts towards forgiveness).

You’ll see in 2026, the doctor’s attending wage makes their cost greater than what the cost would’ve been in the event that they’d began reimbursement from the start on the usual 10-year plan. That cost stops at $1,388 on PAYE, whereas REPAYE continues to extend with revenue progress.

This makes PAYE the optimum reimbursement plan to pursue PSLF.

2. Taxable mortgage forgiveness

Similar story as PSLF for taxable mortgage forgiveness — you wish to pay as little as attainable to maximise how a lot you may get forgiven.

A cost cap will be helpful within the later years of the utmost reimbursement interval to maintain your IDR cost as little as attainable till forgiveness is achieved.

Let’s say forgiveness isn’t your main objective. One other attainable purpose to remain on PAYE or IBR, with out having a partial monetary hardship, is that the cost cap may provide a cost ceiling for money movement functions.

Should you didn’t need the cost to maintain rising with revenue, however weren’t able to decide to student loan refinancing but, that cost cap may offer you some peace of thoughts that the cost gained’t go above a certain quantity.

How do I discover my customary 10-year cost quantity?

This cost quantity’s primarily based on whenever you first entered the IDR plan. If you already know roughly what your stability was at the moment, take the 10-year amortized schedule of that stability to seek out your customary cost. Our student loan payoff calculator can try this for you, too.

You would additionally inquire together with your servicer about what your cost cap is for PAYE or IBR. You may need to ask a number of alternative ways to get the correct reply. Right here’s some ideas:

“What’s essentially the most my cost could possibly be on PAYE or IBR?”

“What’s my customary 10-year reimbursement month-to-month cost?”

“What does my cost quantity need to be beneath to be eligible for PAYE or IBR?”

“For me to have a partial monetary hardship for PAYE or IBR, what does my cost should be beneath?”

Can you turn to PAYE or IBR if you happen to’re on REPAYE?

Sure, so long as you at the moment have a partial monetary hardship, you may swap from REPAYE to PAYE or IBR. You’ll be able to apply for this transformation by means of the Department of Education.

Should you’re not eligible for PAYE or IBR now, however assume you is perhaps shut, contemplate a number of methods to cut back your adjusted gross revenue to turn out to be eligible:

- Has your income decreased since your final tax return on file? In that case, use various documentation of revenue reminiscent of a paystub or a suggestion letter to base your cost off of versus the tax return.

- File taxes separately out of your partner to exclude spousal revenue out of your cost calculation.

- Cut back your adjusted gross revenue by contributing extra to your pre-tax or tax-deferred financial savings autos, reminiscent of: 401(okay), 403(b), TSP, 457, IRA, SIMPLE IRA, SEP-IRA, or HSA.

Maximizing the effectivity of your pupil mortgage reimbursement plan

Navigating one of the best ways to reap the benefits of the partial monetary hardship is sophisticated. Fortunately, we’re specialists in slaying complicated pupil mortgage conditions.

We’ve helped 5,382+ shoppers tackle over $1.34 billion of pupil debt optimize their reimbursement technique. We dwell and breathe pupil loans!

Our pupil mortgage consultants would like to make a custom plan for you so that you don’t need to go it alone anymore.

Refinance pupil loans, get a bonus in 2021

$1,000 BONUS1For 100k or extra. $200 for 50k to $99,999¹

$1,250 BONUS2For 250k+, tiered 300 to 500 bonus for 50k to 250k.2

$1,275 BONUS3For 150k+. Tiered 300 to 575 bonus for 50k to 149k.3

$1,000 BONUS4For $100k or extra. $200 for $50k to $99,9994

$1,050 BONUS5For 100k+. $300 bonus for 50k to 99k.5

$1,250 BONUS6For 100k+ or $350 for 5k to 100k.6

$1,250 BONUS7For 150k+. Tiered 100 to 400 bonus for 25k to 149k.7

Undecided what to do together with your pupil loans?

Take our 11 query quiz to get a personalised advice of whether or not it’s best to pursue PSLF, IDR forgiveness, or refinancing (together with the one lender we predict may provide the greatest price).

1Earnest: $1,000 for $100K or extra, $200 for $50K to $99.999.99. For Earnest, if you happen to refinance $100,000 or extra by means of this website, $500 of the $1,000 money bonus is supplied straight by Scholar Mortgage Planner. Fee vary above contains optionally available 0.25% Auto Pay low costEarnest disclosures. 2Laurel Highway: Should you refinance greater than $250,000 by means of our hyperlink and Scholar Mortgage Planner receives credit score, a $500 money bonus will likely be supplied straight by Scholar Mortgage Planner. In case you are a member of knowledgeable affiliation, Laurel Highway would possibly give you the selection of an rate of interest low cost or the $300, $500, or $750 money bonus talked about above. Gives from Laurel Highway can’t be mixed. Fee vary above contains optionally available 0.25% Auto Pay low cost. Laurel Road disclosures.3Elfi: Should you refinance over $150,000 by means of this website, $500 of the money bonus listed above is supplied straight by Scholar Mortgage Planner. Elfi disclosure. 4Sofi: Should you refinance $100,000 or extra by means of this website, $500 of the $1,000 money bonus is supplied straight by Scholar Mortgage Planner. Fee vary above contains optionally available 0.25% Auto Pay low cost. Sofi disclosures.5Commonbond: Should you refinance over $100,000 by means of this website, $500 of the money bonus listed above is supplied straight by Scholar Mortgage Planner. Commonbond disclosure. 6Credible: Should you refinance over $100,000 by means of this website, $500 of the money bonus listed above is supplied straight by Scholar Mortgage Planner. Credible disclosure.

7LendKey: Should you refinance over $150,000 by means of this website, $500 of the money bonus listed above is supplied straight by Scholar Mortgage Planner. Fee vary above contains optionally available 0.25% Auto Pay low cost.

[ad_2]

Source link

{kind=link}