[ad_1]

Posted on April twenty ninth, 2021

Massive Credit score Card Purchases Actually Can Tank Your Credit score Rating

- Whereas missed funds are arguably the worst offense

- Even racking up quite a lot of debt can decrease your credit score rating considerably

- So it’s finest to place the spending on maintain a couple of months earlier than making use of for a house mortgage

- That means there gained’t be any unwelcome surprises when it comes time to drag your credit score

You’ve in all probability heard sooner or later that making giant purchases along with your bank card(s) earlier than making use of for a mortgage is a no-no.

The truth is, you will have learn that on this very website, since I’ve warned about it on quite a few events in a number of posts as a result of it’s such a standard downside.

You may pay attention to this difficulty, however shrugged it off, pondering what’s a couple of factors, proper?

You have already got wonderful credit score so it doesn’t matter if you are going to buy a brand new $5,000 sofa along with your AmEx card for the brand new digs forward of time.

Effectively, assume once more. It actually does matter, and it may well do critical harm to your credit score rating.

I’m not simply speaking about 5-10 factors. I’m speaking sufficient motion to doubtlessly take you out of the working for a mortgage altogether, or at minimal elevate your mortgage rate.

My Credit score Rating Acquired Rocked After Maxing Out a Credit score Card

- I maxed out one among my bank cards a couple of years in the past

- And my wonderful credit score rating dropped about 50 factors seemingly in a single day

- That’s sufficient to boost your mortgage price relying on how low your scores drop

- Or worse, disqualify you from acquiring a mortgage altogether in case your credit score wasn’t nice to start with

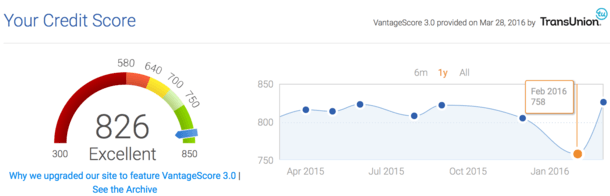

Let’s check out a really actual instance; my credit score rating again in 2016. Sure, I’m utilizing my very own credit score rating for instance this very actual downside.

Luckily, I didn’t apply for a mortgage throughout this era so it wasn’t a problem for me.

As an alternative, it was an ethical blow as I noticed my near-perfect credit score rating drop from over 800 to the mid-750 vary, which by the way remains to be wonderful credit score.

However for individuals who adopted my path and did apply for a house mortgage, it might have spelled critical, critical hassle.

For many of that yr, my credit score rating had been caught in a variety from the low 800s to round 820. This was good as a result of it meant I wouldn’t have any points qualifying for a mortgage based on credit score alone.

Not solely that, however I’d have obtained the most favorable rates and prevented as many mortgage pricing changes as attainable.

When you get your credit score scores above 760 there aren’t many pricing changes (if any) to fret about, so that you don’t want perfection.

Nonetheless, when the vacations hit I began making quite a lot of purchases on my bank card. There was a promotion with Uncover and Apple Pay that supplied 23% money again on all purchases so I hit it arduous.

I principally maxed out my Uncover card, which had a reasonably dismal credit score restrict (possibly solely $5,000 or so) as a result of Uncover is a reasonably conservative lender.

When all was stated and finished, I feel I had 1% obtainable credit score on the cardboard, in any other case often called 99% utilization.

This isn’t a good suggestion, particularly earlier than making use of for a mortgage as a result of it should actually tank your credit score rating, even should you repay the steadiness in full by your due date.

The issue is that the credit score bureaus will take a snapshot of your credit score balances on a sure date after which compute your credit score rating based mostly on that data.

Chances are high TransUnion flagged this maxed out bank card and docked my rating accordingly, principally assuming I used to be happening a nasty path by making a ton of fees in a brief span of time.

That is often a sign {that a} client is in hassle financially, assuming the habits continues. And the bureaus principally despatched out an SOS to new lenders to proceed with warning.

Within the matter of a pair months, my credit score rating fell practically 50 factors. From peak to trough, it fell a complete of 65 factors.

I went from having stellar credit score to having superb credit score. Nonetheless, my rating was beneath 760, which might price you on a mortgage.

Tip: If you happen to should swipe, think about spreading the purchases throughout a number of bank cards to maintain utilization charges on a per-card foundation low. This can be much less damaging than maxing out a single card.

The Good Information Is I Bounced Again Fairly Rapidly!

- Fortunately my maxed out bank card was a short-lived occasion

- My credit score rating bounced again pretty rapidly as soon as I paid off the bank card debt

- So you possibly can resolve it slightly simply, assuming you’ve time to take action

- However the takeaway is to not probability it since you may not at all times have time!

Now the excellent news. As soon as I paid my bank card invoice in full, and the bureaus took word of the brand new $0 steadiness (this isn’t quick), my credit score rating shot as much as its highest level previously 12 months.

My 758 credit score rating went all the best way as much as 826, not too removed from the right credit score rating of 850. It was additionally the very best it had been since Credit score Karma started holding monitor of it a few years earlier.

So regardless of the massive hit early in 2016, I wound up in even higher form than I had been to start with.

This was nice in hindsight, however had I utilized for a mortgage at any time throughout that 30-45 day window, I might have jeopardized the whole factor.

For somebody with a decrease beginning rating, they may have knocked themselves out of eligibility, or at minimal been compelled to tackle a better mortgage price in consequence.

Don’t Make the Identical Mistake I Did If There’s Even a Tiny Likelihood You’ll Apply for a Mortgage Quickly

- If there’s any probability you’ll buy a house or refinance an present mortgage within the close to future

- Put all of your bank cards away and keep away from any pointless purchases

- It’s simply not definitely worth the aggravation or the potential of a better mortgage price and/or denied software

- Simply be affected person and you may return to spending as soon as your own home mortgage funds

The ethical of the story is to heed the warnings of avoiding giant purchases earlier than taking out a mortgage. It’s no joke.

For the document, the identical will be stated of spending your money since you’re depleting your belongings should you make giant money purchases.

And it’s possible you’ll want more cash than anticipated for the down cost, reserves, and shutting prices.

That is very true these days with many properties going for above-asking.

Be sure to put aside plenty of cash in a verifiable account (like a checking or financial savings account) a number of months earlier than you start making bids or inquiring a couple of refinance.

Additionally word that the extra excellent debt you’ve in your bank card(s), the upper your debt-to-income ratio (DTI) will probably be.

And this simply occurs to be one of many fundamental the reason why mortgages get declined.

So racking up bank card debt can damage you in two other ways on the identical time should you’re not cautious.

In different phrases, apply frugality earlier than and in the course of the mortgage software course of and till the mortgage is funded.

These purchases can wait and also you’ll be higher for it.

In spite of everything, mortgages can stick to you for many years – you’d hate for one ill-timed buy to hang-out you for years to come back.

Curiously, when you get your mortgage, you might be able to pay it with a credit card, not that it’s essentially a good suggestion both.

Learn extra: 10 Things You Should Do Before Applying for a Mortgage

[ad_2]

Source link

{kind=link}