[ad_1]

What’s a HomeReady mortgage?

Not having an enormous down fee retains a variety of renters from shopping for their very own properties.

A number of mortgage packages can assist decrease this impediment, together with Fannie Mae’s HomeReady mortgage.

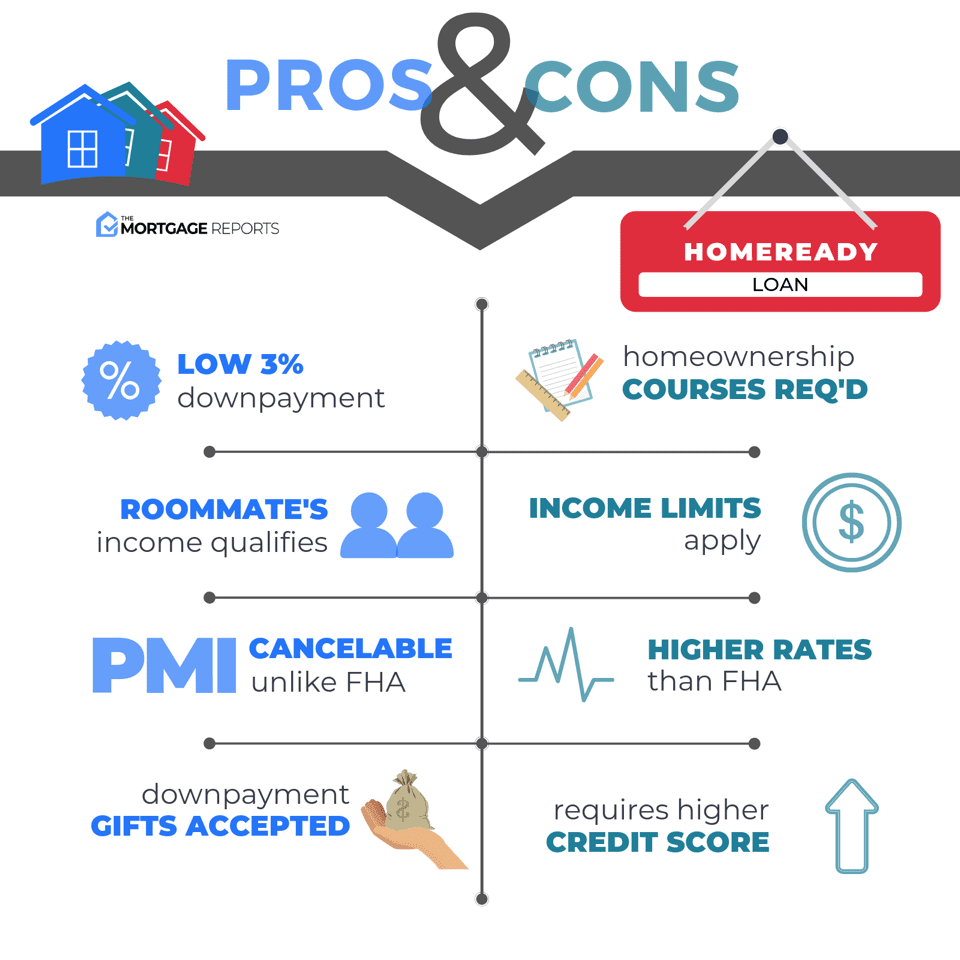

You can pay as little as 3% down on a HomeReady mortgage. That’s $6,000 down on a $200,000 dwelling — even lower than an FHA mortgage’s 3.5% down fee.

Plus you may use presents, grants, or a small mortgage to assist cowl the down fee or closing prices. And, earnings from any grownup dwelling in your house may show you how to qualify.

This makes HomeReady one of many best mortgage packages to qualify for.

Verify your HomeReady eligibility (Jun 3rd, 2021)

On this article (Skip to…)

About The HomeReady Mortgage

Federal mortgage company Fannie Mae launched the HomeReady program in December 2015. It’s now accessible by way of many main U.S. lenders.

Through the HomeReady mortgage, dwelling buyers with lower-than-average earnings for his or her space can get simpler entry to low-down payment mortgages at in the present day’s present charges.

HomeReady permits a down fee of simply 3%. And as a novel profit, it permits “earnings pooling,” that means earnings from all earners in a family will be counted in underwriting.

Because of this earnings from grandparents, mother and father, relations, and dealing youngsters can all be used to assist qualify for a house mortgage.

For a lot of households, this may imply the distinction between getting authorised for a mortgage and getting turned down.

Present householders may also use HomeReady for a refinance.

This system permits as much as 97 p.c loan-to-value (LTV) in some circumstances. With different mortgage packages refinancing may require LTV as little as 80 to 85 p.c.

Qualifying for a HomeReady Mortgage

To get a HomeReady mortgage, you’ll must fall inside the program’s earnings limits, take a brief on-line class about homeownership, and have respectable credit score.

Actual necessities may range by lender, however Fannie Mae units the minimal necessities for all HomeReady mortgage functions.

Fundamental necessities for HomeReady embrace:

- You have to not earn greater than 80% of your Census tract’s median earnings. Check your area’s median income here

- You have to agree to finish a 4-6 hour on-line homeownership training course

- You want a FICO rating of a minimum of 620 typically

- It is advisable use the house as your main residence

- You want a debt-to-income ratio (DTI) no increased than 50%. That is extra lenient than most different mortgage packages

Should you meet these standards, the HomeReady mortgage program could also be simply what that you must transfer from renting to homeownership.

Verify your HomeReady eligibility (Jun 3rd, 2021)

HomeReady earnings limits

Fannie Mae units earnings limits for its HomeReady program. To qualify, you may’t make greater than 80% of your space’s median earnings (AMI).

Which means in case your space has a median yearly earnings of $100,000, you will need to make $80,000 or much less to qualify for the HomeReady program.

Since HomeReady is meant for lower-income debtors, these limits won’t be an issue for many candidates.

However what when you’re frightened your earnings is just too low to qualify?

In that case, the HomeReady mortgage can assist immensely. Fannie Mae permits candidates to depend earnings from different family members on their utility, making it simpler to qualify for the mortgage.

You should use earnings from a renter, so long as they’ve lived with you for a minimum of one yr prior to purchasing the house.

Or you should use earnings from a member of the family, buddy, or different non-renter family member to assist qualify.

On this case, the particular person doesn’t must have lived with you for one yr. And, they don’t should be in your mortgage utility. The lender merely counts their earnings as a ‘compensating issue’ — giving your earnings the additional increase it would have to make you mortgage-eligible.

Check your income eligibility (Jun 3rd, 2021)

Eligible property sorts

Debtors have many choices for getting actual property with a HomeReady mortgage.

You should buy a standard single-family dwelling if you want. However, in order for you one thing a little bit completely different, Fannie Mae additionally permits the acquisition of:

- Condominium models

- Properties in a deliberate unit improvement (PUD)

- Co-ops

- Manufactured properties

- Multifamily properties with 2, 3, or 4 models

Simply word, debtors who need a multi-unit dwelling will want a better credit score rating, probably as excessive as 680.

It doesn’t matter what kind of dwelling you purchase with HomeReady, it must be your main residence. Which means if the constructing has 2-4 models, you will need to reside in one of many models your self full-time.

In different phrases, this mortgage program can’t be used to buy funding properties or trip properties. It’s supposed for low and moderate-income consumers in search of a house to reside in.

HomeReady mortgage rates of interest

Rates of interest for a HomeReady mortgage mortgage are the identical as charges for a “conventional” mortgage. There isn’t any premium utilized for utilizing the HomeReady program.

Actually, mortgage charges for the HomeReady mortgage may be even decrease than for different low-down-payment mortgages — like the three% down conventional 97 loan.

However, as a result of mortgage charges can range by as a lot as 50 foundation factors (0.50%) between lenders, it pays to buy round. Don’t cease purchasing after you get your first quote.

Fastened-rate mortgage choices

Debtors utilizing the HomeReady mortgage program have entry to a whole mixture of fixed-rate mortgage merchandise, together with:

- 10-year fixed-rate mortgage

- 15-year fixed-rate mortgage

- 20-year fixed-rate mortgage

- 30-year fixed-rate mortgage

This vary of choices is an enormous benefit over USDA loans, which supply solely a 30-year mortgage.

Shorter-term loans typically have decrease rates of interest than 30-year loans. Due to the low fee and quick time period, debtors can save tens of hundreds in mortgage curiosity over the lifetime of the mortgage.

Nevertheless, 10-, 15-, and 20-year loans usually have a lot increased month-to-month funds than 30-year mortgages. That’s as a result of it’s a must to repay the identical mortgage quantity in a shorter period of time.

For that reason, most dwelling consumers select a 30-year fixed-rate mortgage.

Adjustable-rate mortgage choices

Debtors utilizing the HomeReady mortgage program even have entry to a variety of adjustable-rate mortgage (ARM) merchandise. These embrace the:

Adjustable-rate loans have a set fee for the primary 5, 7, or 10 years. After that, your rate of interest and month-to-month fee may rise every year.

This makes ARMs a lot riskier than fixed-rate loans.

Some main lenders have opted out of HomeReady ARMs. So in order for you an adjustable-rate mortgage, you will have to buy round for a lender providing these.

Verify your new rate (Jun 3rd, 2021)

Assist together with your HomeReady down fee

HomeReady’s 3% down fee is about half the average down payment measurement, and it’s a fraction of the 20% many renters assume they’d want to save lots of up.

Nonetheless, arising with 3% — which is $6,000 for a $200,000 dwelling — will be difficult for dwelling buyers who’ve restricted earnings and/or financial savings.

HomeReady helps by permitting versatile sources in your down fee cash. You can use:

- Present funds — Members of the family may show you how to give you your down fee by gifting the cash. Word, this should be a real reward and never a mortgage in disguise. Be taught extra about down payment gift requirements here

- Residence purchaser grants — Ask your mortgage officer or actual property agent about down fee help packages in your space. Many native governments and nonprofits supply these

- Down fee loans — Fannie Mae’s Group Seconds program can assist you safe a second mortgage particularly to cowl your down fee and shutting prices. Down fee help may supply a low- or no-interest mortgage as effectively

Utilizing a second mortgage corresponding to Group Seconds will put a second lien on your property which implies you’d must repay each loans — your main mortgage and your second mortgage — when you promote or refinance.

HomeReady loans vs. FHA loans

Like HomeReady loans, FHA loans assist individuals overcome the monetary challenges to homeownership.

Should you qualify for HomeReady, you may additionally qualify for FHA. However which mortgage program is healthier?

Renters with restricted money for a down fee have used FHA loans since 1934. FHA’s minimal down fee quantity is 3.5%, barely increased than HomeReady’s 3%.

The down funds are related, however these two mortgage packages have some huge variations.

When is an FHA mortgage higher than HomeReady?

FHA works finest for debtors with decrease credit score scores.

With a FICO as little as 580, you may borrow with solely 3.5% down. (Debtors with scores between 500-579 may nonetheless qualify, however they’d want a minimum of a ten% down fee.)

Backing from the Federal Housing Administration helps lenders lengthen favorable mortgage phrases to debtors with decrease credit score scores.

Against this, HomeReady relies upon extra on the borrower’s credit score, and also you’d sometimes want a rating of a minimum of 620 to qualify.

FHA loans additionally work finest for increased earners for the reason that FHA program, not like HomeReady, doesn’t have earnings limits.

When is HomeReady higher than an FHA mortgage?

HomeReady loans supply extra flexibility when it’s time for earnings verification.

For instance, lower-income debtors may add earnings from different adults within the family to the mortgage utility. This might show you how to qualify for a bigger mortgage quantity whereas additionally decreasing your DTI.

You can even depend supplemental earnings from a boarder’s lease when you plan to have a roommate or lease out a room in the home.

Plus, since HomeReady is a traditional mortgage, you may cancel personal mortgage insurance coverage (PMI) when you’ve paid the mortgage right down to 80% of the house’s worth. This could decrease your month-to-month mortgage funds significantly.

By comparability, FHA’s mortgage insurance coverage protection lasts the lifetime of the mortgage until you set 10% or extra down.

Keep in mind, although, it’s a must to earn 80% or lower than your space’s median earnings to qualify for HomeReady.

Fannie Mae HomeReady vs. Freddie Mac Residence Attainable

Freddie Mac’s Residence Attainable program works so much like Fannie Mae’s HomeReady.

Just like the HomeReady program, Freddie Mac’s Residence Attainable mortgage:

- Permits 3% down fee

- Has an earnings restrict of 80% of the world median earnings

- Is co-borrower pleasant

There are two greatest variations, although.

First, many lenders require a credit score rating of a minimum of 660 to qualify for a Residence Attainable mortgage. HomeReady, alternatively, it sometimes accessible with a FICO rating of 620 or increased.

As well as, Freddie Mac doesn’t depend non-borrower earnings on the mortgage utility.

Each packages permit you to use boarder earnings to qualify when you’ll have somebody renting a room, so long as the particular person has lived with you for a minimum of a yr already.

However solely Fannie Mae’s HomeReady program will depend earnings from non-renter family members in your favor. So this program is probably going higher in case your earnings is on the borderline of qualifying.

Compare your low-down-payment mortgage options (Jun 3rd, 2021)

Fannie Mae HomeReady FAQ

No, the HomeReady mortgage program can be utilized by first-time consumers and repeat consumers. Nevertheless, you may’t get a HomeReady mortgage when you nonetheless owe cash on multiple different dwelling mortgage.

No, you do not want to have good credit score to make use of HomeReady. You don’t even must have common credit score. The HomeReady mortgage program is out there to consumers with credit score scores beginning at 620.

Sure, you may nonetheless use the HomeReady program in case your credit score rating is non-existent. This system permits the usage of non-traditional tradelines to ascertain credit score historical past, together with utility payments, mobile phone or web payments, fitness center memberships, and most different accounts which require month-to-month fee.

Fannie Mae provides the HomeReady program through personal mortgage lenders. In different phrases, you don’t apply instantly with Fannie Mae. Slightly, you may apply with nearly any mainstream mortgage lender. Most are approved to do Fannie Mae loans. You may sometimes apply on-line, over the telephone, or by strolling into an area financial institution or lender’s workplace.

Fannie Mae has given all of its authorised mortgage lenders authority to underwrite and approve HomeReady mortgages. Your lender could also be opting out, and that’s okay. There are many authorised mortgage lenders who can assist you. Name up a pair different lenders till you discover one which does supply this program.

No. The MyCommunityMortgage (MCM) program was retired by Fannie Mae in late 2015. HomeReady is a more recent mortgage program launched in December 2015. It’s not the identical as a MyCommunityMortgage and, in some respects, HomeReady will be considered as a alternative.

The HomeReady mortgage program requires a minimal down fee of three%. If you are going to buy a $250,000 dwelling, for instance, you’d want a minimum of $7,500 right down to qualify for HomeReady.

Sure, your down fee on a HomeReady mortgage is usually a money reward from a relative, a partner, a girlfriend or boyfriend, or a fiancé/fiancée. The cash doesn’t want to come back from your individual financial savings. Ensure your mortgage officer and actual property agent know you’ll be utilizing gifted funds. And, be sure that the funds are correctly documented through a mortgage reward letter.

You aren’t required to convey any of your individual cash to closing with the HomeReady mortgage program. Your down fee will be gifted to you from a third-party, and you may have the house vendor pay in your closing prices utilizing an choice often known as vendor concessions. Sometimes, closing prices vary from 2% to five% of the mortgage quantity, so make certain you focus on these prices together with your actual property agent and mortgage officer earlier than you go beneath contract to purchase a house. And, you’d want to debate any vendor concessions previous to signing the contract.

Sure, the HomeReady program limits debtors to a 50% debt-to-income ratio.

Sure, the HomeReady program requires debtors to pay personal mortgage insurance coverage (PMI) once they borrow greater than 80% of the house’s worth. PMI cancels robotically as soon as the mortgage reaches 78% LTV.

The HomeReady program options decrease mortgage insurance coverage prices than different standard loans, together with the opposite 3% down program, the standard 97. Actual PMI prices rely in your credit score rating and down fee. Your mortgage officer can inform you how a lot PMI will value in your HomeReady mortgage when you’ve accomplished an utility.

HomeReady is a traditional mortgage mortgage through Fannie Mae, which implies that you’re required to pay personal mortgage insurance coverage till your property’s loan-to-value (LTV) reaches 80% of the unique buy worth, or 80% of the house’s market worth.

Sure, you should use the HomeReady program to refinance your present dwelling, together with a restricted money out refinance (LCIR). One advantage of refinancing with HomeReady is that you simply solely want 3% fairness within the dwelling to qualify (that means the max LTV is 97 p.c). Another refinance packages require a minimum of 20% fairness, or a most loan-to-value of 80 p.c.

Sure, the HomeReady program permits a borrower to make use of boarder earnings to assist get certified. That features rental earnings from accent dwelling models. Boarders will need to have a 12-month historical past of dwelling with you and contributing earnings. Documentation of all 12 months shouldn’t be all the time required.

Sure, that is the aim of the HomeReady mortgage program. You’re allowed to make use of the earnings of an individual dwelling in your house that can assist you qualify in your dwelling mortgage. Utilizing another person’s earnings in underwriting can decrease your DTI considerably and make it a lot simpler to qualify. This consists of earnings from mother and father, youngsters, roommates, and different grownup members of the family.

No, you do not want to incorporate different individuals in your HomeReady mortgage utility — even when their earnings is used that can assist you qualify. To be able to use one other particular person’s earnings in your utility, you’ll solely want to point out that particular person’s proof of earnings and a signed assertion indicating their intent to reside with you for a interval of a minimum of 12 months.

No, the HomeReady program doesn’t restrict the variety of relations dwelling in a single dwelling, nor the variety of relations whose earnings is used to assist qualify for this system.

No. Nevertheless, non-borrowing relations will need to have authorized paperwork to point out their immigration standing — a inexperienced card, work visa, and many others.

No. Debtors should meet earnings pointers to qualify. Initially, HomeReady labored for all debtors in low-income census tracts, however Fannie Mae revised this system in 2019 to take away that characteristic. Now, all dwelling consumers utilizing HomeReady should meet earnings eligibility necessities.

Sure, house owner counseling is required with the HomeReady program. The net course, known as Framework, will be accomplished in 4-6 hours in your smartphone.

Sure, you should use the certificates out of your earlier house owner counseling course as a part of your HomeReady mortgage utility, as long as the course was accomplished inside the final six months.

Sure. You may personal different residential properties and nonetheless get a HomeReady mortgage, assuming you propose to make the brand new dwelling your main residence. Nevertheless, you may’t use HomeReady when you nonetheless owe cash on multiple different property mortgage. Co-borrowers who don’t plan to reside within the dwelling can owe cash on multiple further property.

What are in the present day’s HomeReady mortgage charges?

The HomeReady mortgage program is designed to assist extra U.S. households get authorised for low-down fee loans. Debtors can use earnings from relations and non-relatives for buy and refinance dwelling loans.

Get in the present day’s reside mortgage charges now. Your Social Safety quantity shouldn’t be required to get began, and all quotes include entry to your reside mortgage credit score scores.

[ad_2]

Source link

{kind=link}