[ad_1]

How one can construct (and pay for) your dream residence

Right now’s tight housing markets and low rates of interest have raised residence costs in lots of areas.

As a substitute of competing to purchase an present home, you may take into account constructing a brand new residence.

There are nice perks to constructing your individual residence: you may have management over the structure and supplies, you’ll be able to select the placement, and there’s no competitors from different patrons.

Nevertheless, financing a house development mission is extra sophisticated than shopping for an present residence. So it’s essential to know the method and prices concerned earlier than leaping in.

Check your construction loan options (May 14th, 2021)

On this article (Skip to…)

Constructing a home: the fundamentals

Constructing a house may be very totally different from shopping for a house off the market — particularly with regards to financing the price of development.

A mortgage on an present house is pretty simple: you are taking out a single mortgage which includes one utility, on appraisal, one cut-off date, and one set of closing prices.

With a brand new residence development, the method could be sophisticated. There’s not only a mortgage to think about, but additionally financing for the land, labor, and supplies.

In the event you’re contemplating constructing a house, right here are some things to bear in mind:

- Financing your dream residence mission could require a sequence of loans with a number of rounds of paperwork and charges. Nevertheless, sure mortgage applications and lenders can consolidate this course of

- “One-time-close” development loans may make it easier to finance the land, development, and mortgage all with a single mortgage

- Anticipate to make a bigger down fee for a development mortgage than for a conventional mortgage — usually 20% to 25% (versus as little as 3% for a house buy)

- Planning is important. The lender has to approve your builder and your development plans alongside along with your private funds

- Constructing versus shopping for — Prices range broadly by location, however could also be related in lots of areas

In order for you a customized residence in your best location — and you’ve got the money and time to make a development mortgage occur — constructing a brand new home could possibly be an ideal selection.

In the event you’re in a rush, although, you is likely to be higher off shopping for an present property off the market.

Buying a house is often sooner than constructing one, and also you’ll usually have decrease hurdles to clear for issues like down fee and credit score rating.

Explore home loan options to build or buy (May 14th, 2021)

How development loans work

Constructing your individual residence may require one, two, and even three separate loans. For instance, you want financing to:

- Purchase the land

- Pay the development prices

- Repay the lot and development mortgage with a regular mortgage, which you’ll repay over as much as 30 years

‘True’ development loans are short-term loans, often 6-18 months. They’re used solely to finance residence development (not the land or everlasting mortgage). And typically, you pay curiosity solely on what you borrow.

Building mortgage charges are often variable rates of interest primarily based on the prime price plus a sure share

Some applications allow you to wrap development mortgage curiosity into the everlasting financing. This may be useful if you happen to’re additionally attempting to pay an present mortgage or lease whereas constructing your new home.

How a lot does a house development mortgage value?

Anticipate to pay extra for development financing than you’ll for a conventional residence mortgage — even when the fee to construct or purchase is nearly the identical.

New residence development loans value extra for a pair causes:

- Extra threat — Lenders tackle a much bigger threat as a result of the development course of consists of extra variables. And, the house getting used as ‘collateral’ for the mortgage quantity doesn’t but exist. This threat interprets into increased rates of interest in comparison with commonplace mortgages

- Extra paperwork — Cash is disbursed at totally different factors within the development course of, and the lender has to confirm sufficient work has been accomplished to justify the subsequent “draw” of funds

Lenders additionally require lien waivers proving builders have paid their subcontractors earlier than issuing attracts.

Attracts could be performed in levels, for instance, a lender may divide the mission into seven levels and launch cash at every stage. Or they might permit builders to request cash primarily based on the share of completion.

Usually, the extra attracts allowed, the nicer it’s for the builder. Nevertheless, each draw provides to your prices due to the admin work concerned.

Is it cheaper to purchase or to construct a house?

The thought of constructing a brand new residence may scare you since you imagine it’s the pricier possibility. However, relying on location and residential options, the price of constructing a home is comparable to purchasing an present residence.

The typical new residence prices $296,652 to construct, in line with the Nationwide Affiliation of Dwelling Builders’ 2020 research.

Actual property web site Zillow studies the common worth of an present residence at $269,039.

Each of those numbers range broadly — by tons of of hundreds of {dollars} in some circumstances — relying on the state and particular space the place you propose to purchase or construct.

Verify your home buying eligibility (May 14th, 2021)

Forms of development loans

Some residence patrons use as much as three separate loans to construct a house: one mortgage to purchase the land, one to construct the house, and one to transform the development prices right into a everlasting mortgage (which works like a typical residence mortgage).

You might consolidate these steps, particularly in case your builder is prepared to finance development prices till you utilize a regular mortgage mortgage to repay the builder.

Or, you can search for a mortgage that funds your complete course of with one mortgage.

One-time-close development loans

Some lenders provide “one-time-close” or “construction-to-permanent” loans. These are development loans that convert to conventional mortgages after you get the certificates of occupancy to your residence.

For example, Fannie Mae, FHA, VA, and USDA applications all provide one-time shut development loans.

These mortgages require just one closing, and also you get authorized solely as soon as, assuaging the dangers of two approval processes. In the event you get a fixed-rate mortgage, you’ll be able to lock in your curiosity earlier than development begins.

For extra data, see:

Nevertheless, these mortgage applications could be more durable to seek out from mainstream lenders, so it’s best to anticipate to buy round in order for you one in all these loans.

Getting separate loans for every stage of the development course of is likely to be simpler from a lender standpoint. It would provide you with extra management as nicely, as a result of you’ll be able to store for one of the best charges on every mortgage.

Nevertheless, utilizing two or three loans means paying two or three units of closing prices — and going via the underwriting course of a number of instances.

Check your home loan options (May 14th, 2021)

Fannie Mae construction-to-permanent mortgage

Many patrons preferring the “single-closing” technique select Fannie Mae’s construction-to-permanent mortgage possibility.

With this program you’d make no mortgage funds whereas the house stays underneath development. As a substitute, mortgage compensation begins after closing.

Like several construction-to-permanent mortgage, Fannie Mae will roll development prices into your everlasting mortgage upon getting a certificates of occupancy.

This mortgage can generate “on the spot residence fairness” as a result of Fannie Mae bases its loan-to-value ratio on development prices, together with lot acquisition, assuming that quantity is decrease than the house’s eventual worth.

For instance, if a house prices $200,000 to construct, however an appraiser values it at $250,000, Fannie Mae would nonetheless base its LTV on the $200,000 in development prices. You might put $40,000 down (20% of $200,000) and take out a $160,000 mortgage.

Due to the house’s worth of $250,000, you’d immediately have $90,000 in residence fairness ($250,000 minus the $160,000 mortgage stability). It’s essential to recollect development prices and property values range so much by state.

Two-time-close loans

The opposite financing possibility is a two-time-close development mortgage — two separate loans. You’ll get a development mortgage first, after which repay it when development ends by refinancing right into a everlasting mortgage.

This implies making use of for 2 totally different loans with two closings, and all of the related closing prices for each.

Many lenders require you to have a everlasting mortgage lined up earlier than they’ll launch funds for the constructing course of.

This two-loan technique offers you flexibility if there’s a development delay requiring you to increase the development mortgage time period.

And, you’ll have entry to raised refinancing selections than with a construction-to-permanent or one-time-close mortgage.

Which development mortgage is finest?

The fantastic thing about a construction-to-permanent mortgage is that you simply keep away from a number of mortgage purposes, packages of lender charges, and title prices.

Nevertheless, the main disadvantage is that these loans lock you in along with your development lender.

You don’t all the time know what mortgage price you’ll be provided till the development is full. Or if you’re locked in, charges could have dropped through the development interval, and also you might be able to do higher with one other lender.

One-time-close development loans could be easier and value much less upfront, however you may find yourself with the next mortgage price in the long term.

By no means settle for your lender’s everlasting price with out evaluating present mortgage charges from its opponents.

One-time-close mortgages can lower your expenses by consolidating some charges, nevertheless it’s no financial savings in case your everlasting mortgage’s curiosity is considerably increased than present mortgage charges.

In the event you plan to maintain your house and mortgage for a few years, it could pay to switch your construction-to-permanent mortgage with a greater one. You might also be capable to negotiate a decrease price along with your development lender if you happen to usher in affords from different lenders.

Refinancing a development mortgage to a mortgage mortgage

In the event you use a short-term development mortgage that solely covers constructing prices, you’ll seemingly have to refinance into a conventional mortgage as soon as development is full.

Individuals who take out construction-only loans could also be owner-builders who plan to behave as their very own contractor or do the lion’s share of the constructing themselves.

Many mortgage lenders gained’t work with owner-builders as a result of they will’t make sure that the home will actually be a major residence and never a “spec” deal.

You may also select a construction-only mortgage to have extra management over the everlasting financing.

You’d be capable to store for the bottom mortgage price as soon as the house turns into prepared for occupation.

How to buy a development mortgage refinance

When your house nears completion, begin evaluating mortgage charges and interviewing lenders. Don’t let your credit score rating drop throughout development, as a result of that can improve your rate of interest and make approval more durable.

Nearly any program open to conventional residence refinances needs to be obtainable to you as nicely. Get a number of quotes from competing lenders, and attempt to get them on the identical day so you may make an efficient analysis.

After you have your lender, get your utility authorized as quickly as you’ll be able to. You’ll not need pricey delays as soon as your house is able to occupy.

How lengthy does it take to get a house development mortgage?

A 90-day approval course of on development loans is frequent, as a result of the lender should approve the mission and the builder, not simply you.

Your builder ought to submit development plans — together with a description of materials and a cost breakdown — for the lender to judge.

The builder’s development plans ought to embody flooring plans, ceiling heights, timetables — all the pieces it’s going to take to create your dream residence. Skilled builders will seemingly already find out about your lender’s necessities.

When the lender has your builder’s development plans in hand, it’s going to appraise the worth of the house upon its completion.

Building mortgage approval usually takes as much as 90 days. Constructing the house itself can take wherever from 4 months to over a 12 months.

Your lender can even consider your private funds through the approval course of.

For many applications, you want a stable credit score historical past, an excellent FICO rating, and a dependable revenue. You could have to make mortgage repayments throughout development. Lenders favor you may have satisfactory financial savings for value overruns and surprising prices.

Most lenders are useful on this course of, even offering builder approval packages.

Nevertheless, approval insurance policies, prices, and mortgage phrases can range considerably. So evaluate development mortgage prices to see what you’ll be able to afford and interview lenders rigorously earlier than making use of for loans.

Start your home loan approval today (May 14th, 2021)

How lengthy does it take to construct a house?

On common, it will possibly take wherever from 4 to 12 months to construct a house.

The period of time varies with the complexity of the job, the ability of the builder, and outdoors forces just like the climate.

A small manufacturing residence on a fraction of an acre lot may take 4 to 6 months. An infinite customized residence on an acre or extra takes 10-16 months. Labor and supplies availability additionally affect development completion dates.

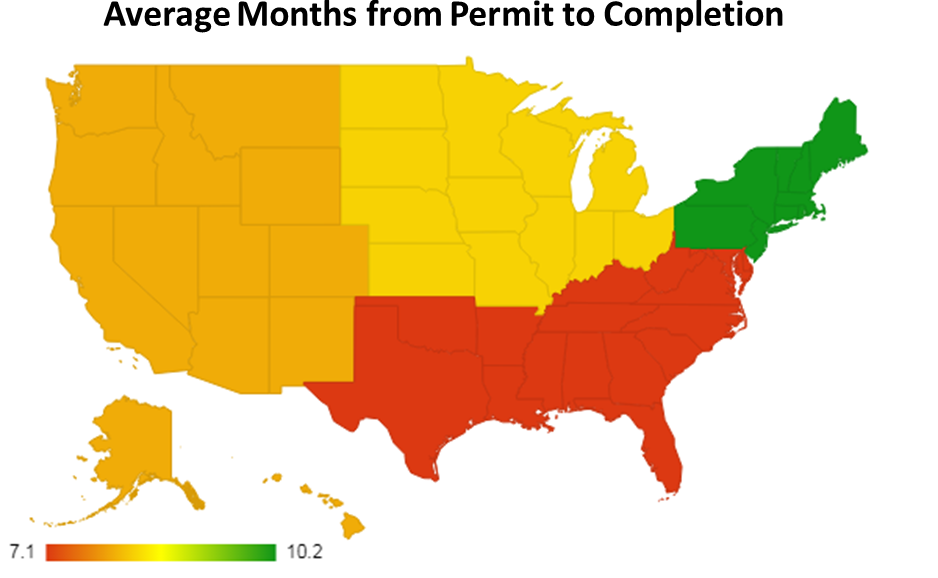

Based on the U.S. Census, common construct instances additionally rely in your location:

Supply: U.S. Census, Traits of New Housing, 2018. Picture: ThePlanCollection.com

Pre-construction points ceaselessly sluggish initiatives down when clearing and prepping land reveals surprises, particularly on massive tons.

Allowing may throw off your schedule and could also be a bit political. And your municipality requires you to get permits, code inspections, and approvals all through development.

The larger the house you’re setting up, the extra endurance and persistence you’ll want.

Selecting a builder or contractor

To get financing to your dream residence mission, you’ll have to work with a certified builder or normal contractor.

You could have imagined being an owner-builder, and you’ll have the abilities to make this occur.

However in actuality, you’d must be an owner-builder with deep sufficient pockets to finance the mission your self, as a result of most banks gained’t again a do-it-yourself mission.

As well as, most lenders have requirements for builders, and if yours doesn’t meet them, you’ll be able to’t finance your development with a mortgage lender.

This may be a bonus for you — by defending themselves from unqualified builders, lenders are additionally defending you.

How one can discover a certified builder

You possibly can verify your builder’s licensing standing and often discover complaints by wanting on-line to your state contractor’s board.

Or, simply seek for your potential contractor’s title, location, and the phrase “license” to get this data.

Personally interview no less than three builders or normal contractors in your brief checklist and be taught all you’ll be able to about how they full development initiatives. Know whether or not your personalities mesh, since you’ll work with them virtually day by day for six months or longer.

Be aware what’s included and what’s assured (defects, overruns, and deadlines, for example).

As with all costly contract, don’t log off on something you don’t perceive. Get a purchaser’s actual property agent specializing in new development or an actual property lawyer to assist if you happen to want it.

How a lot can I borrow for my residence constructing mission?

If you’re shopping for an present residence, it’s doable to finance as much as 100% of the house’s worth relying in your mortgage program.

Not so with development loans. Anticipate your lender to finance solely 75% to 80% of your house’s eventual worth.

This leaves a 20% to 25% down fee requirement for you, the borrower.

Lenders require massive down funds as a result of constructing your individual residence requires a dedication for as much as a 12 months or extra. Debtors who make a considerable down fee are typically much less prone to stroll away mid-project.

The quantity you’ll be able to borrow after your down fee depends upon the mortgage program you utilize.

FHA and standard loans have totally different maximums, and lenders could set their very own limits. So verify along with your lender to see how a lot you’ll be able to borrow primarily based in your mortgage sort and funds.

Learn how a lot residence you’ll be able to afford

You management the out-of-pocket prices for constructing a home by creating an reasonably priced price range.

As soon as you already know what you’ll be able to spend, work with a good builder who is aware of the world and who can inform you what you’ll be able to and might’t afford to incorporate in your new home.

The Mortgage Studies has a home affordability calculator you should utilize to find how a month-to-month fee interprets to a mortgage quantity, or how a lot residence you’ll be able to afford given your earnings and present bills.

Start with the fundamental necessities, including a ten% cushion for value overruns. In the event you can afford further facilities, add them in.

Building prices can escalate, so it’s sensible to price range for this. Because of this, lenders usually construct in 5% to 10% for contingencies.

For example, if you happen to plan to spend $200,000 constructing, you’ll have to qualify for a $220,000 mortgage.

The builder ought to embody an outline of supplies and a price breakdown, which you’ll want whenever you apply for a development mortgage.

Verify your maximum loan amount (May 14th, 2021)

Constructing versus shopping for your dream residence

Constructing versus shopping for is a private selection, and your private funds and preferences ought to information you.

As you determine, take into account these professionals and cons.

Execs of shopping for an present residence

Shopping for a house could be sooner and simpler than constructing one.

You’ll keep away from unexpected delays within the constructing course of, and also you don’t should pay for lease or a mortgage whereas ready to your new residence to be accomplished.

As well as, present houses are sometimes in established residential neighborhoods. Usually, which means they’ll have mature timber and landscaping that provides substantial residence worth.

Mature timber and shrubbery may decrease vitality costs. In the summertime, shade from tall timber reduces cooling prices. Throughout the winter, mature timber and shrubs lower heating prices by blocking winds.

In the event you purchase in a well-developed space, you may additionally have facilities like outlets, eating places, and leisure inside strolling distance.

Cons of shopping for an present residence

Relying on its age, buying an present residence means shopping for all of its issues.

Older homes have extra put on and tear, are sometimes much less energy-efficient, and might generally require costly upkeep. How a lot these are and after they’re needed depends upon the house’s age.

About 50% of the common home wants substitute throughout its first 30 years. A home with a heating or cooling system, home equipment, or a roof previous half its helpful lifespan means you’ll in all probability find yourself changing these objects.

Homeownership prices add as much as hundreds of {dollars}, relying what repairs or replacements are needed and the place you reside.

By constructing a home, you won’t have any important upkeep prices for the primary 10 years. And you’ll in all probability have some form of guarantee safety.

Analysis reveals that houses constructed after the 12 months 2000 save their house owners 21% yearly on vitality prices.

Verify your home buying eligibility (May 14th, 2021)

Execs and cons of constructing a brand new residence

Constructing your house places you accountable for all the choices, huge and small, that go into a brand new residence — from the sq. footage of the cupboard space to the peak of the yard fence.

However there are potential pitfalls when constructing a brand new residence, too. Right here’s what it’s best to know.

Execs of constructing a house

Retrofitting an present residence can get expensive. A serious benefit of constructing new is that, from structure to location, you’ll be able to tailor it to your tastes and household wants.

If you construct a home, you’ll be able to put it the place you need it and create the surroundings you want.

A brand new home additionally will get outfitted with the most recent options like energy-efficient supplies, technology-friendly wiring, and safety methods.

And you’ve got virtually full management over the development supplies utilized in your own home, in addition to the price of constructing a house.

Your builder choice might be an important resolution you’ll make, so don’t enter the connection flippantly.

Meaning you may make aesthetic choices (like hardwood vs. carpet) in addition to sensible choices. For example, you may keep away from toxins within the supplies, making the inside surroundings safer for you and your loved ones.

Along with making your house eco-friendly, including Vitality Star or inexperienced home equipment makes it energy-efficient, lowering utility prices. You possibly can select to speculate extra in some areas of the home and fewer in others.

There are different monetary advantages to constructing your individual home, too:

- You don’t pay for premium options you don’t need, like a completed attic or wall-to-wall carpeting

- It’s possible you’ll get extra worth for cash since you get the structure you want

- Upkeep and restore prices shall be low for the primary 7 to 10 years. Minor repairs get lined underneath your house guarantee, and also you often have a one- to ten-year builder guarantee

There aren’t prone to be any surprising damaging surprises if you happen to select the fitting builder or contractor to your mission, and get your house constructed correctly.

Your builder choice might be an important resolution you’ll make, so don’t enter the connection flippantly.

Cons of constructing a house

Dwelling constructing could be sophisticated. It could disrupt your life-style.

What if the timing doesn’t work out and also you promote your present residence, however have to attend a number of extra months to finish your new residence? Likelihood is you’d should put all the pieces in storage and discover short-term housing.

Dwelling development initiatives are liable to:

- Delays from improperly structured contracts

- Delays from modifications to the development plan

- Price overruns

- Climate delays

- Delays as a result of supplies had been delivered late

Good planning might help keep away from many of those issues, however others could occur unexpectedly.

For instance, following Hurricane Katrina, the price of constructing supplies soared — not one thing you’d essentially predict.

Botched or late customized orders should not uncommon. And, when a builder or subcontractor fails to comply with the newest residence blueprint, the impact could be disastrous.

So long as the error isn’t one thing large like improperly put in load-bearing partitions, it’s fixable, although not often cost-free.

Typically, builders or normal contractors cover or trigger development defects. There could also be residence guarantee issues that you simply don’t find out about. In case your builder or residence guarantee doesn’t cowl these defects, it’s possible you’ll face massive prices to right issues.

Shopping for a fixer-upper: A contented medium?

One option to cut up the distinction between shopping for and constructing is rehabbing. That’s, you purchase a home with so much and basis, and finance your renovations proper into the acquisition.

You are able to do this with one in all a number of merchandise:

- The FHA 203(k) loan bases your mortgage quantity on the improved worth of the property and requires solely 3.5% down for many candidates

- Fannie Mae’s HomeStyle mortgage means that you can finance second houses and leases in addition to major residences. Put as little as 5% down

- When you’ve got low-to-moderate revenue, the HomeReady loan can get you within the door with simply 3% down and versatile underwriting

- Freddie Mac’s Renovation Mortgages are just like Fannie Mae’s merchandise. Tips do range, although, so that you may get authorized for one even if you happen to’re declined for one more

As with all mortgage, it pays to match affords from a number of lenders.

Constructing a home: The underside line

Homeownership has a number of benefits whether or not you construct or purchase.

Succeeding in constructing your individual residence requires a powerful group. Your builder and your lender shall be key members of this group. They will make your dream residence a actuality.

Choose your builder and lender rigorously, and also you’ll have an ideal likelihood to construct the house you need inside your price range.

[ad_2]

Source link

{kind=link}