[ad_1]

Posted on July 14th, 2021

Mongoose vs. Cobra. Coyote vs. Roadrunner. Pirate vs. Ninja? And at last, “fixed-rate mortgage vs. adjustable-rate mortgage.” Sure, we’re speaking in regards to the biggest rivalries of all time.

So what’s higher, the boring previous fixed-rate mortgage or the extra provocative and sometimes controversial adjustable-rate mortgage (ARM)?

Through the housing increase within the early 2000s, owners typically selected adjustable-rate mortgages as a method to qualify for a house they in all probability wouldn’t have the ability to afford with a standard fastened mortgage.

Again then, you would qualify a borrower on the ARM’s decrease begin price, although the mortgage would finally alter a lot larger.

Even when they might afford a fixed-rate mortgage, owners had been comfortable to take the bottom rate of interest attainable, which usually got here with the ARM.

However occasions have modified, and adjustable-rate mortgages have now fallen out of style with fixed-rate mortgage charges hovering close to document lows.

In truth, fixed-rate mortgages account for greater than 90% of the acquisition cash mortgages and refinance loans being originated these days.

Positive, fastened mortgages are undoubtedly extra widespread, however that doesn’t imply they’re any higher, or at all times the correct selection.

It’s only a matter of desire for many. And as houses grow to be much less and fewer reasonably priced, the recognition of ARMs will rise as soon as extra.

Mounted-Price Mortgages Just like the 30-12 months Are the Default Possibility

- Most householders go for fixed-rate mortgages when shopping for a house or refinancing an present mortgage

- We’re speaking 90% or extra of all house loans are 30-year or 15-year fastened mortgages

- ARMs had been very fashionable previous to the mortgage disaster due to their relative affordability

- However now have lower than 5% market share (that might change as house costs proceed to rise)

When taking out a mortgage, most individuals have a tendency to decide on a fixed-rate mortgage, making it the default choice.

The preferred of the fastened mortgages is the 30-year fastened, seeing that the cost is fastened for all the time period of the mortgage, and the long amortization period retains month-to-month funds low.

The 15-year fixed-rate mortgage can be fairly widespread, however as a result of all the stability have to be paid off in half the period of time, month-to-month funds are a lot larger. Which means fewer debtors are prepared or ready to decide on one as a consequence of affordability issues.

Usually, a house owner will begin with a 30-year fastened, then when it comes time to refinance, they’ll go together with a 15-year fastened to remain on monitor and avoid resetting the clock.

There are additionally adjustable-rate mortgages, which most debtors are inclined to keep away from except they’re extraordinarily savvy investor-types, ultra-rich, or instructed to take action by their mortgage dealer or mortgage officer.

I say savvy as a result of some people will take an opportunity on the preliminary rate of interest low cost provided on ARMs regardless of the related danger of a better rate of interest sooner or later.

So you want to know what you’re doing when choosing an ARM, and most significantly, have the capability to soak up any rate of interest changes sooner or later.

As talked about, there have been additionally these debtors who needed to take out an adjustable-rate mortgage to qualify as a result of the rate of interest was decrease.

This was a routine apply earlier than the mortgage disaster, with the ARM choice sometimes floated by the true property agent, dealer, or mortgage officer whether or not it was within the borrower’s finest curiosity or not.

This isn’t as widespread these days as a result of it’s not essentially simpler to qualify for an ARM because you typically must qualify on the fully-indexed price.

What Kind of ARM Are We Speaking About?

- Right now’s ARMs are often hybrids with a set and adjustable interval

- They function a set rate of interest at first of the mortgage time period for X variety of years

- Adopted by an adjustable-rate interval for the rest of the mortgage time period

- This makes them somewhat bit safer, however not as low cost as they in any other case can be

The massive query when debating the fastened vs. ARM choice is what sort of adjustable-rate mortgage are we coping with?

As of late, it’s fairly widespread to take out an ARM with an preliminary fixed-rate interval, corresponding to a 5/1 ARM or a 7/1 ARM.

The above examples are fastened for the primary 5 and 7 years, respectively, earlier than turning into yearly adjustable for the rest of the time period. They’re often known as hybrid ARMs for that purpose.

There’s even an choice that’s fixed for 10 years before its first adjustment, making it comparatively low-risk.

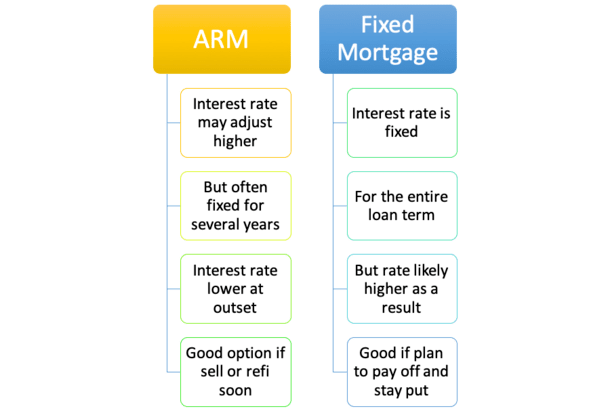

This implies you’ve acquired some respiratory room earlier than the rate of interest adjusts up or down. That’s proper, your mortgage interest rate can transfer up or down if it’s an ARM.

And all of those ARMs are amortized over a 30-year interval, that means they’ll take 30 years to repay, assuming you maintain them till maturity (which most debtors don’t).

So they’re the identical as a fixed-rate mortgage when it comes to size, and in case you solely maintain them for 5 or seven years, they act no in another way relating to how a lot principal and curiosity is paid.

Truly, you’d doubtless repay extra of your principal stability and pay much less curiosity because of the decrease rate of interest on the ARM.

The main distinction is that the 30-year fastened is, ahem, fastened, whereas the ARMs are, you guessed it, adjustable. By adjustable, I imply your mortgage price can transfer up, down, or sideways.

This clearly presents some critical danger, assuming mortgage charges rocket larger through the few brief years you maintain the mortgage.

ARMs Can Go Up and Down

- ARMs can alter larger or decrease over time relying on the related mortgage index

- In that sense they don’t essentially must be refinanced

- Whereas if mortgage charges drop considerably after you get hold of your mortgage

- Chances are you’ll must refinance your fixed-rate mortgage to benefit from decrease market charges

Whereas it’s attainable that mortgage charges may transfer decrease sooner or later, they’re nonetheless close to document lows and can greater than doubtless rise over the subsequent few years.

So an ARM you get hold of immediately will in all probability reset larger upon its first adjustment, that means your month-to-month mortgage cost will go up.

In the event you can’t deal with that hypothetical larger mortgage cost, chances are you’ll need to stick to the 30-year fastened, even when it’s barely larger immediately.

However will you keep within the house for 5-7 years, or will you progress. And can you refinance earlier than that point?

If there’s a great probability you’ll do both, an ARM may make extra sense than a fixed-rate mortgage.

For instance, in case you are shopping for your first house, however plan to maneuver or improve to a greater house as you begin a household, an adjustable-rate mortgage may be the most suitable choice short-term.

And the cash saved throughout these few years can be utilized for a down cost on the subsequent house. Moreover, the decrease rate of interest will increase affordability through the months it’s held.

In the meantime, it hasn’t been unusual these days for owners to decide on a 30-year fastened, then refinance into one other 30-year fastened shortly after as soon as charges improved.

In the intervening time, mortgage indexes tied to ARMs are so low that your first price adjustment may lead to a decrease price, assuming there isn’t a ground on the speed.

For instance, many of those ARMs are tied to the LIBOR, which is at present round 0.25%. If the margin is 2.25, your mortgage price would drop to round 2.50%, assuming the caps/ground allowed for it.

Nonetheless, this low price surroundings gained’t final eternally, so somebody who elects to go together with this sort of ARM will doubtless endure long-term.

Most will in all probability should refinance or promote earlier than that occurs. That’s why short-term ARMs are sometimes reserved for the very rich, who’ve the choice to refinance or repay the mortgage at any time when they select.

In the event you go together with an ARM and don’t have the choice to pay it off or refinance, you would be caught with a rising cost, which may put your mortgage (and property) in jeopardy.

Additionally be aware that each fixed-rate mortgages and ARMs require energetic participation. Simply because your mortgage has a set price doesn’t imply you don’t should keep watch over charges.

If charges transfer decrease, chances are you’ll lose out in case you don’t refinance your fixed-rate mortgage. So it’s not as set-it-and-forget-it because it seems.

Tip: By no means select an adjustable-rate mortgage simply to qualify for a mortgage. In the event you can’t qualify for a mortgage on the fastened mortgage price, contemplate holding off and renting for a while or shopping for a less expensive property.

Does the Preliminary Low cost of an ARM Justify the Danger?

- Ensure the ARM low cost is definitely worth the danger of a probably larger price later

- Additionally contemplate how lengthy you’ll maintain your private home mortgage and the property

- You won’t maintain it lengthy sufficient to ever fear a few price reset

- If that’s the case, it could possibly be a significantly better deal than the costlier fastened mortgage you gained’t take full benefit of

Make sure you’re getting a great low cost on the ARM in change for the uncertainty and danger of it rising sooner or later.

At the moment, 30-year fastened mortgage charges are hovering round 3%, whereas the 5/1 ARM is pricing round 2.50%, relying on the lender.

This unfold isn’t nice in the meanwhile, that means ARMs aren’t too favorable.

If we’re speaking a few short-term ARM, corresponding to a 1-month or 1-year ARM, it higher prevent a substantial amount of cash early on.

On a $250,000 mortgage, you’d be financial savings of roughly $66 monthly with the ARM, or almost $4,000 saved over the primary 5 years of the mortgage.

You’d additionally pay about $6,000 much less in curiosity throughout that point, with extra of your hard-earned {dollars} going towards the principal stability.

If and when fastened rates of interest rise, the ARM will present extra worth, assuming spreads widen.

Not dangerous, however is it definitely worth the danger? Nicely, that depends upon a lot of elements.

As talked about, in case you don’t plan to stay round within the house lengthy or maintain the mortgage for the complete mortgage time period, it could possibly be an ideal transfer.

However rates of interest are doubtless headed larger, so chances are you’ll pay the value later as soon as the ARM adjusts. And it might be tougher to refinance sooner or later…

Danger urge for food, age (retirement), job standing, funding technique, and downright stress can even come into play, so you should definitely do loads of math and examine completely different situations earlier than deciding on something!

Merely put, you’re taking a danger when selecting an ARM (therefore the low cost), so take a tough have a look at the numbers in comparison with fastened price choices.

Whereas an adjustable-rate mortgage supplies financing at a reduction, it comes with rather more uncertainty, particularly in immediately’s market.

And if it’s actually a purpose to repay your mortgage, a set mortgage is mostly the most suitable choice for many.

Tip: In the event you purchase an owner-occupied property that you simply intend to later hire out for the long-term, a fixed-rate mortgage may be a great decide since you’ll in all probability maintain the mortgage for a protracted time frame.

And chances are high you gained’t need to refinance the mortgage since financing is costlier on funding properties.

Professionals of Mounted-Price Mortgages

- The rate of interest will NEVER change

- Your month-to-month cost gained’t fluctuate

- Simpler to handle your funds/price range

- Charges on fixed-rate mortgages are very low in the meanwhile

- No stress about what charges are doing (you’ll be able to sleep at night time)

- No must refinance except charges drop dramatically (however you continue to can if want be)

- Simple to wrap your head round, no surprises

Cons of Mounted-Price Mortgages

- Rates of interest are sometimes costlier

- Your month-to-month cost will probably be larger

- You’ll pay extra curiosity over the mortgage time period

- It could possibly be more durable to qualify for a mortgage with the next price

- You’ll pay your mortgage off extra slowly

- You’ll construct fairness at a slower price

- Chances are you’ll select not refinance for concern of dropping your low, fastened price

Professionals of Adjustable-Price Mortgages

- Decrease mortgage price (not less than initially)

- Decrease month-to-month cost

- You’ll pay much less curiosity within the early years

- Construct fairness sooner whereas rate of interest is decrease

- Most ARMs are fastened for a sure period of time

- Caps and ceilings restrict rate of interest motion

- You would possibly promote/transfer earlier than the rate of interest even adjusts

- You possibly can at all times refinance if charges rise and also you qualify

- Rates of interest can really drop over time!

- You’ll have further money readily available for different bills or investments

Cons of Adjustable-Price Mortgages

- Rates of interest can rise considerably in a brief time frame

- Chances are you’ll not have the ability to afford the upper month-to-month cost post-adjustment

- You can lose your private home to foreclosures in case you can’t sustain with funds

- Chances are you’ll refinance time and again and by no means really repay your mortgage

- Refinancing may be fairly pricey versus holding your authentic fixed-rate mortgage

- You may be caught together with your high-rate mortgage in case you don’t qualify for a refinance

- ARMs typically function flooring that restrict in case you rate of interest can really drop

- It’s worthwhile to actively maintain monitor of mortgage charges

- You’ll doubtless be much more careworn

- Your rate of interest could dictate whether or not you progress or keep put

- Tougher to price range precisely

- Time strikes sooner than chances are you’ll suppose

(picture: eckes/bernd)

[ad_2]

Source link

{kind=link}