[ad_1]

In the event you’re a health care provider, you’ve in all probability been enthusiastic about your pupil loans for the reason that day you started medical college. And also you possible know you need a plan for your massive medical student loan debt.

The Public Service Mortgage Forgiveness program (PSLF) is a well-liked pupil debt aid possibility for medical professionals. It’s usually the principle plan for docs to wipe out their pupil loans in as little as 10 years. Docs can enter this compensation program as quickly as they start residency.

In the event you’re relying on PSLF, the place you select to finish your residency can determine in case you’re eligible or not. Under, we clarify why for-profit residency hospitals can journey up medical professionals who’re pursuing PSLF. We’ll additionally focus on discover PSLF hospitals close to you.

A evaluation of PSLF

The PSLF program is a authorities pupil mortgage forgiveness possibility. Docs and medical professionals can qualify for this program by working full time at a qualifying employer. The next might be thought-about qualifying public service employment:

- Authorities organizations at any stage (federal, state, native or tribal)

- Not-for-profit organizations which are tax-exempt below Part 501(c)(3) of the Inside Income Code

- Different sorts of not-for-profit organizations that aren’t tax-exempt below Part 501(c)(3) of the Inside Income Code, if their main function is to offer sure sorts of qualifying public providers

Word: You may as well qualify for PSLF by volunteering full-time for AmeriCorps or Peace Corps.

Ensuring your home of residency qualifies as a nonprofit of public service group is barely step one. You’ll additionally wish to be sure that your loans are all federal Direct Loans and that you simply join a qualifying compensation plan. Federal Household Training Loans (FFEL) and Perkins Mortgage) Program don’t qualify however can turn out to be eligible in the event that they’re consolidated into a brand new Direct Consolidation Loan.

In the event you meet the eligibility necessities listed above, you possibly can start the Public Service Loan Forgiveness form here. In case your utility is accepted, your eligible loans will probably be moved out of your present servicer to FedLoan Servicing.

That mentioned, after making 120 qualifying funds, your remaining steadiness will probably be forgiven tax-free. Even higher, these eligible funds don’t must be consecutive.

The typical physician graduates with $200,000 in medical education debt based on the AAMC, the advantage of working at PSLF hospitals might be within the six figures. You possibly can see why you’d wish to get began on this pupil mortgage forgiveness program as quickly as attainable.

How selecting a for-profit residency impacts PSLF

Your required location for residency might land you in a for-profit hospital — particularly with major hospitals being sold to for-profit Hospital Corporation of America (HCA). If this occurs, you possibly can’t start your PSLF program till after your residency.

Which means that for at the least three to 5 years, you’re making pupil mortgage funds with out having them rely towards PSLF. At this level, you might have two choices to check.

Possibility 1: Enroll in an income-driven compensation plan and reduce value throughout residency. Then join PSLF.

Let’s say you enter your residency at a for-profit hospital with $190,000 of pupil mortgage debt with a median 6.5% rate of interest. You’re eligible to enroll in an income-driven compensation (IDR) plan below Pay As You Earn (PAYE). Let’s additionally assume you’re making a median of $57,000 per yr and your month-to-month funds are $323.

Over the course of a five-year residency, you’d put $19,380 towards your federal pupil loans. Your academic loans would have nonetheless grown attributable to curiosity throughout this time. Every year, $12,350 of curiosity is added to your principal steadiness, making the overall you owe about $232,370.

After residency, you can start PSLF, however you’d most probably be making a big quantity extra. The typical pay for a doctor is $208,000 per yr, based on the Bureau of Labor Statistics, so let’s use that quantity.

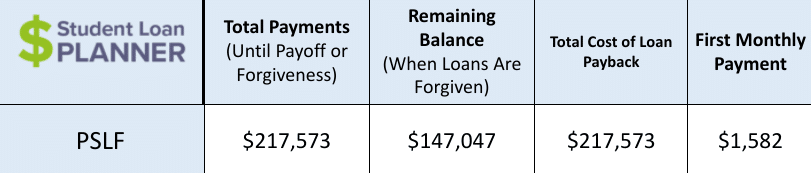

We see that you simply’d make the minimal funds for 10 years. Your first fee could be $1,582 monthly, however this might improve in case your pay or family earnings rises. On the finish of 10 years, you’d have roughly $147,047 of pupil mortgage debt forgiven and may have paid a complete of $217,573.

These few years of not being in PSLF whereas at a for-profit hospital undoubtedly would have value you in the long term. However not as a lot as refinancing would.

Possibility 2: Refinance your pupil loans for a decrease charge and start payoff

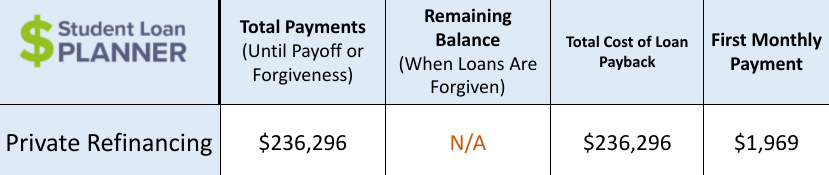

You can refinance your student loan debt for a decrease charge — below 3% in some circumstances. However right here we’ll assume you refinance at 4.5% together with your unique beginning steadiness of $190,000. You’d pay a complete of $236,296 to repay your pupil loans over a 10-year interval.

PSLF vs. refinancing

The underside line is you’ll save extra money by working at PSLF hospitals and pursuing forgiveness than refinancing your federal loans.

Whereas staying on an IDR plan throughout residency after which becoming a member of PSLF will take 5 years longer than an ordinary refinancing fee time period, you’ll have extra money in your pocket by the tip of it. That mentioned, you run the chance of this system going away, as is true with anybody at present on PSLF.

In the event you plan to remain within the personal sector or transfer to non-public apply, you possibly can’t even think about PSLF. It then is smart to refinance your student loans or go for an income-driven compensation plan.

Find out how to discover PSLF hospitals

The supply of hospitals that qualify for PSLF close to you’ll rely largely on the place you reside. For instance, there are at present seven states by which over 90% of hospitals are nonprofits or state hospitals according to the Kaiser Family Foundation (KFF). Nevertheless, in 4 states, the share of PSLF hospitals is under 30%.

In the event you’re desirous to see if a hospital close to you, you possibly can seek for it on Guidestar’s directory or nonprofit organizations. You may as well use the PSLF Help Tool to seek for eligible employers. Lastly, it could’t damage to easily ask your recruiter a few hospital’s for-profit or non-profit standing throughout your job interview.

What about choosing an income-driven compensation plan as a substitute?

You might determine to remain working within the personal sector. In the event you already signed up for an IDR plan throughout residency, you possibly can proceed to remain the course. Bear in mind, this plan is much less fascinating than PSLF for 2 main causes:

- You’ll make funds for 20 to 25 years, and

- It’s a must to pay taxes on the quantity forgiven.

After all, you possibly can’t assist this when working within the personal sector. You possibly can, nonetheless, just remember to choose a repayment plan that prices you the least sum of money.

What fee program do you have to be on for PSLF or IDR?

Each PSLF and IDR forgiveness require the borrower to be on an eligible IDR compensation plan. Your choices are:

In the event you nonetheless determine to pursue PSLF after residency — or IDR throughout residency — the fee plan you select impacts how a lot cash stays in your pocket. Within the instance above, PAYE was used as a result of it’s one of many plans that retains your fee low.

Select the plan that permits for the bottom month-to-month fee, even when this implies your pupil mortgage steadiness will develop. PAYE and REPAYE are the most effective choices, since they take solely 10% of your discretionary earnings. You possibly can decrease your month-to-month adjusted development earnings by maxing out your pretax retirement accounts.

The thought is to capitalize on forgiveness. Preserve to the minimal funds and don’t make additional funds, as these will probably be a waste of your cash.

Weighing your entire choices for mortgage forgiveness

There are extra student loan forgiveness options for healthcare professionals accessible. Consider what a for-profit hospital PSLF strategy will appear to be for you in comparison with the IDR mortgage forgiveness route, in addition to how different packages would possibly assist.

State-specific loan forgiveness programs and mortgage forgiveness for areas in excessive want of main care supply incentives and mortgage forgiveness. When you have the liberty to take action, these plans can knock out a very good chunk of pupil mortgage debt.

In 2019, HCA launched a student loan assistance program for people who work at certainly one of its for-profit hospitals. At the moment, this program provides a month-to-month advantage of $150 in case you work full-time and $75 in case you’re a part-time worker. Whereas that is one thing to think about in case you work for an HCA facility, it pales compared to your different pupil mortgage forgiveness choices.

Nonetheless undecided which route you wish to take? The professionals at Pupil Mortgage Planner® might help. We’ll run your particular numbers and supply a compensation plan that can mean you can reside a full life in your new profession. Reach out and schedule a consultation today.

Refinance pupil loans, get a bonus in 2021

$1,050 BONUS1For 100k+. $300 bonus for 50k to 99k.1

$1,000 BONUS2 For 100k or extra. $200 for 50k to $99,9992

$1,050 BONUS3For 100k+. $300 bonus for 50k to 99k.3

$1,275 BONUS4 For 150k+. Tiered 300 to 575 bonus for 50k to 149k.4

$1,000 BONUS5For 100k+. $300 bonus for 50k to 99k.5

$1,000 BONUS6For $100k or extra. $200 for $50k to $99,9996

$1,250 BONUS7 For 100k+ or $350 for 5k to 100k.7

$1,250 BONUS8For 150k+. Tiered 100 to 400 bonus for 25k to 149k.8

Undecided what to do together with your pupil loans?

Take our 11 query quiz to get a customized advice of whether or not it is best to pursue PSLF, IDR forgiveness, or refinancing (together with the one lender we predict may provide the finest charge).

All charges listed above characterize APR vary. 1Commonbond: In the event you refinance over $100,000 via this website, $500 of the money bonus listed above is offered straight by Pupil Mortgage Planner. Commonbond disclosure. 2Earnest: $1,000 for $100K or extra, $200 for $50K to $99.999.99. For Earnest, in case you refinance $100,000 or extra via this website, $500 of the $1,000 money bonus is offered straight by Pupil Mortgage Planner. Charge vary above contains non-obligatory 0.25% Auto Pay low costEarnest disclosures.

3Laurel Street: In the event you refinance greater than $250,000 via our hyperlink and Pupil Mortgage Planner receives credit score, a $500 money bonus will probably be offered straight by Pupil Mortgage Planner. If you’re a member of knowledgeable affiliation, Laurel Street would possibly give you the selection of an rate of interest low cost or the $300, $500, or $750 money bonus talked about above. Affords from Laurel Street can’t be mixed. Charge vary above contains non-obligatory 0.25% Auto Pay low cost. Laurel Road disclosures.

4Elfi: In the event you refinance over $150,000 via this website, $500 of the money bonus listed above is offered straight by Pupil Mortgage Planner. Elfi disclosure. 5Splash: In the event you refinance over $100,000 via this website, $500 of the money bonus listed above is offered straight by Pupil Mortgage Planner. Splash disclosure. 6Sofi: In the event you refinance $100,000 or extra via this website, $500 of the $1,000 money bonus is offered straight by Pupil Mortgage Planner. Charge vary above contains non-obligatory 0.25% Auto Pay low cost. Sofi disclosures. 7Credible: In the event you refinance over $100,000 via this website, $500 of the money bonus listed above is offered straight by Pupil Mortgage Planner. Credible disclosure.

8LendKey: In the event you refinance over $150,000 via this website, $500 of the money bonus listed above is offered straight by Pupil Mortgage Planner. Charge vary above contains non-obligatory 0.25% Auto Pay low cost.

[ad_2]

Source link

{kind=link}