[ad_1]

Your lender requested for a letter of rationalization. What now?

Whenever you apply for a house mortgage, your lender will do a deep dive into your monetary historical past. Relying on what it finds in your financial institution statements or credit score report, further documentation could also be crucial.

It’s possible you’ll be requested for a “letter of rationalization” throughout the utility course of. Worry not. Letters of rationalization are pretty customary and nothing to fret about.

Nevertheless, you wish to ensure you write this letter accurately, because it may very well be essential to your mortgage approval.

Right here’s all the pieces it’s essential to know so you’ll be able to hit a house run together with your letter of rationalization.

Start your mortgage application today (Jul 20th, 2021)

On this article (Skip to…)

What’s a mortgage letter of rationalization?

Generally known as an ‘LOE’ or ‘LOX,’ letters of rationalization are sometimes requested by lenders to achieve extra particular data on a mortgage borrower and their scenario.

An LOX can crucial when there may be inconsistent, incomplete, or unclear data on a mortgage utility.

Letters of rationalization could also be required if any purple flags flip up throughout the underwriting course of, similar to:

- Declining earnings

- Gaps in your employment historical past

- Differing names in your credit score report

- Giant deposits or withdrawals in your checking account

- Current credit score inquiries

- An tackle discrepancy in your credit score report

- Derogatory objects in your credit score historical past

- Late funds on bank cards or different money owed

- Overdraft charges on an account

There are lots of different conditions the place an LOX could also be requested, too.

If it’s essential to write one, be sure you ask your mortgage officer what precisely the underwriter needs to see, and whether or not it’s essential to present any supporting documentation together with the letter.

Easy methods to write a letter of rationalization to your mortgage lender

On the subject of mortgage letters of rationalization, much less is often extra.

An excessive amount of pointless data could result in confusion, or at minimal, further questions on your file — questions that will have been prevented if it weren’t for a number of the particulars in your letter.

An important parts of your letter of rationalization ought to embrace the next:

- Information — Be sincere. By no means be tempted to jot down a letter based mostly on solely on what it’s possible you’ll suppose your lender needs to listen to. You shouldn’t fabricate any facet of your letter. Embody appropriate dates, greenback quantities, and another pertinent particulars to your scenario

- Decision — Your lender needs to know the way and when the scenario that led as much as sure occasions was resolved. For example, for those who had been quickly furloughed throughout COVID, however you’ve since returned to full employment, it’s best to be capable to doc your latest paystubs and have your employer confirm that you just’ll proceed working full time for the foreseeable future

- Acknowledgement — This one is vital and shouldn’t be not noted of your letter. Mortgage underwriters wish to know why it’s that one thing occurred, and the way or why it gained’t occur once more sooner or later

Keep in mind that a letter of rationalization is an expert doc that can go into your mortgage file.

Be aware of issues like spelling, grammar, and punctuation. Create a letter that’s visually interesting, correctly formatted, and communicates the related data.

Offering further documentation together with your letter might be useful. For instance, if hospitalization was the perpetrator behind some missed funds in your credit score report, it could be useful to incorporate hospital payments.

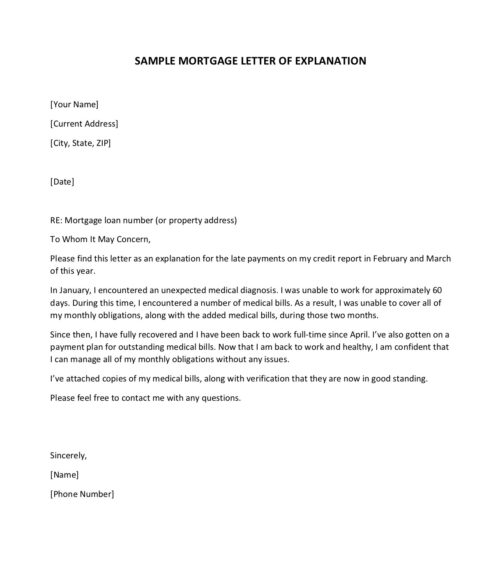

Pattern letter of rationalization and template

Bear in mind to be sincere, formal, and concise when writing a letter of rationalization to your mortgage lender.

The precise content material will range based mostly in your scenario, however right here’s a basic letter template you should utilize as a information. (Click on the picture to open a PDF model.)

Bear in mind to incorporate your mailing tackle, telephone quantity, and the variety of your mortgage mortgage utility (or the property tackle for which you’re making use of).

Closing recommendation on writing a letter of rationalization

You’ll be requested to submit a pile of documentation throughout the mortgage mortgage course of, together with financial institution statements, tax returns, pay stubs, and extra.

Relying in your monetary scenario, your lender can also request a letter of rationalization. Many first-time house patrons suppose being requested to supply a letter of rationalization means their mortgage utility could also be doomed.

Bear in mind, one of these request is normally a superb factor. The underwriter could also be in search of this final merchandise earlier than signing off in your closing approval.

When your lender requests a mortgage letter of rationalization, keep in mind this primary: don’t panic.

Subsequent, double-check together with your lender on precisely what’s being requested.

Then write a transparent, concise letter that’s freed from emotional language, negativity, or extreme element. There’s a superb probability that the subsequent time you hear out of your lender, it will likely be to let you already know you’re absolutely authorized.

[ad_2]

Source link

{kind=link}