[ad_1]

Our objective is to provide the instruments and confidence it is advisable to enhance your funds. Though we obtain compensation from our companion lenders, whom we are going to at all times establish, all opinions are our personal. Credible Operations, Inc. NMLS # 1681276, is referred to right here as “Credible.”

Should you’re a home-owner and 62 or older, you may be weighing your choices to entry your own home’s fairness. A reverse mortgage, residence fairness mortgage, or residence fairness line of credit score (HELOC) may present the money you want for residing bills, residence enhancements and repairs, medical payments, or nearly another goal.

A reverse mortgage doesn’t require you to make mortgage funds whilst you’re alive; HELOCs and residential fairness loans do. However reimbursement is just one of a number of components to think about when you’re considering these mortgage merchandise.

Learn the way every choice works to find out which one most closely fits your wants:

How residence fairness loans and HELOCs work

Residence fairness loans and HELOCs are each second mortgages. With both mortgage, you possibly can borrow cash primarily based on how a lot fairness you have got in your house. You’ll repay the cash in month-to-month installments.

Since these loans are secured by your own home, they’ve comparatively low rates of interest. Nevertheless, second mortgages are thought of riskier for lenders than first mortgages.

Because of this, you possibly can anticipate HELOC and residential fairness charges to be one or two share factors greater than present mortgage charges.

You’ll additionally must have a great chunk of residence fairness — most lenders will need you to have at the very least 15% fairness in your house.

Understanding residence fairness loans

Residence fairness loans will let you borrow towards the worth of your own home and obtain a lump sum at a hard and fast rate of interest. You may repay the cash over a time period so long as 30 years.

You’ll have to start out repaying each principal and curiosity inside a couple of month of getting your mortgage proceeds.

Understanding HELOCs

HELOCs will let you borrow any quantity as much as a longtime credit score restrict. As an alternative of borrowing the cash abruptly, you possibly can borrow smaller sums as you want them. On this approach, HELOCs are much like bank cards.

Not like a bank card, although, which lets you borrow and repay cash indefinitely, a HELOC limits borrowing to a particular draw interval — usually between 5 to 10 years.

Many lenders don’t require debtors to repay any principal through the draw interval; as a substitute, they solely ask that you simply pay curiosity on what you’ve borrowed.

Tip: Most HELOCs have variable rates of interest, however you would possibly be capable of discover a lender that provides a fixed-rate choice, which may also help you extra simply handle your funds and doubtlessly prevent cash in curiosity.

How reverse mortgages work

A reverse mortgage provides you money to spend nevertheless you need. Should you nonetheless owe cash in your first mortgage, you’ll have to make use of the reverse mortgage proceeds to pay it off, and the remaining proceeds are yours.

Nevertheless, it’s not a second mortgage, and it doesn’t require you to make month-to-month funds.

The quantity you possibly can borrow might be greater relying on:

- How previous you might be

- How a lot your own home is price

- How low present curiosity are

A reverse mortgage’s mortgage stability grows over time however isn’t due till you die or completely transfer out of your own home. Normally, the lender will get repaid by promoting the house. Alternatively, the proprietor’s heirs can repay the mortgage and maintain the house.

- Line of credit score: Much like a HELOC, you’ll borrow the quantity you want and solely pay curiosity and costs on what you borrow. Any credit score you don’t use in your credit score line will proceed to develop (as much as the utmost quantity of your mortgage).

- Fastened month-to-month funds: You’ll have two decisions for the way to obtain your fastened month-to-month funds. “Tenure” funds present funds for so long as you reside in your house. “Time period” funds present funds for a sure variety of years.

- Lump sum: You’ll obtain the entire funds at one and pay curiosity and costs on the complete mortgage quantity.

{Qualifications} for a reverse mortgage

You should meet these {qualifications} to be eligible for a HECM reverse mortgage:

- Be at the very least 62 years previous

- Personal and occupy an eligible property kind, comparable to single-family residence, as your major residence

- Be capable of afford ongoing property prices, together with owners insurance coverage, property taxes, and upkeep

- Personal your own home mortgage-free, or have at the very least 50% residence fairness

- Full a HUD-approved reverse mortgage counseling session

- Not be delinquent on any federal debt (comparable to taxes or scholar loans)

Professionals and cons of residence fairness loans and HELOCs

The primary advantages of residence fairness loans and HELOCs are their comparatively low rates of interest and the chance to borrow plenty of cash, whereas the principle downside is that these loans are secured by your own home, doubtlessly rising your threat of foreclosures.

Professionals and cons of a house fairness mortgage

| Professionals | Cons |

|---|---|

| Low, fastened rate of interest | Secured by your own home |

| Fastened month-to-month funds | Should have good credit score |

| Lengthy reimbursement interval | Curiosity provides up over time |

| Low closing prices | Should have sufficient revenue to qualify |

Professionals and cons of a HELOC

| Professionals | Cons |

|---|---|

| Borrow as wanted over as much as 10 years | Variable rate of interest |

| Fastened month-to-month funds | Not paying principal throughout draw interval can improve borrowing prices |

| Lengthy reimbursement interval | Should have good credit score |

| Low closing prices | Should have sufficient revenue to qualify |

Professionals and cons of a reverse mortgage

A reverse mortgage mortgage permits seniors to entry their residence’s worth even when they’ll’t afford month-to-month funds or qualify for different sorts of loans, however it comes with appreciable prices.

| Professionals | Cons |

|---|---|

| Credit score rating not a think about approval | Excessive closing prices |

| Revenue not a think about approval | Tougher to go away your own home to heirs |

| No reimbursement required so long as the house is your predominant residence | Mortgage insurance coverage premiums and month-to-month servicing charges |

| You’ll by no means owe greater than your own home is price | Variable rate of interest on most fee choices |

See: Reverse Mortgage Options: 5 Choices for Seniors

Which choice is best for you?

Should you can meet a lender’s revenue and credit score necessities, reverse mortgage alternate options like a house fairness mortgage or HELOC will most likely be higher choices. These loans have a lot decrease upfront prices and are simpler to know than reverse mortgages.

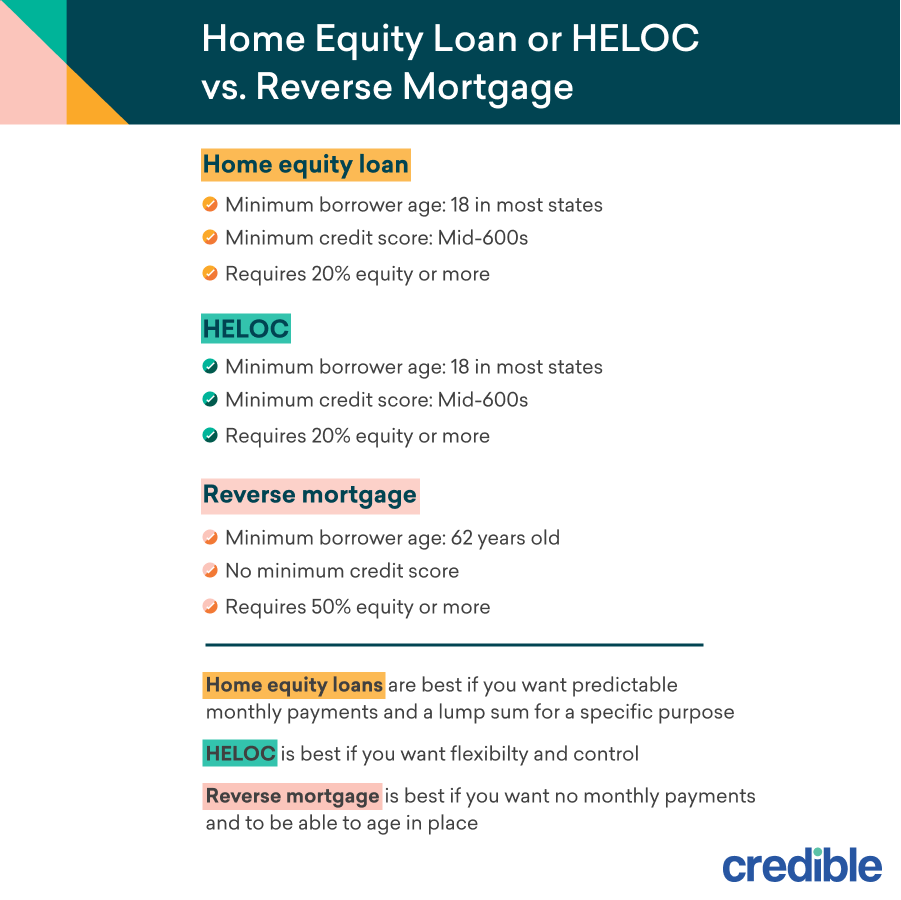

| Residence fairness mortgage | HELOC | Reverse mortgage | |

|---|---|---|---|

| Min. borrower age | 18 in most states | 18 in most states | 62 |

| Fund entry | Lump sum | As wanted | Lump sum, as wanted, or month-to-month |

| Rate of interest | Fastened | Normally variable however might be fastened | Normally variable however might be fastened |

| Required month-to-month funds | Principal and curiosity | Curiosity solely throughout draw interval; principal and curiosity throughout reimbursement interval | None |

| Min. credit score rating | Mid-600s | Mid-600s | None |

| Fairness required | Greater than 20% | Greater than 20% | Greater than 50% |

When to think about a house fairness mortgage

- You may meet credit score and revenue necessities

- You need predictable month-to-month funds

- You want a lump sum for a particular goal

- You wish to depart your own home to your heirs

When to think about a HELOC

- You may meet credit score and revenue necessities

- You need the flexibleness to determine when to borrow and the way a lot

- You wish to make interest-only funds for the primary a number of years of the mortgage

- You’re comfy with a variable rate of interest

- You wish to depart your own home to your heirs

When to think about a reverse mortgage

- Your house fairness is your greatest asset

- You wish to age in place

- You may have poor credit score

- You don’t wish to make month-to-month funds

- You’re an older retiree

- You’re okay with the lender promoting your own home to repay the mortgage as soon as you progress out or cross away

Tip: Even when you’re retired, you should still qualify for a second mortgage primarily based in your retirement revenue from sources comparable to Social Safety, annuities, a pension, or your retirement accounts.

An alternative choice to think about: Money-out refinancing

Older owners may be enthusiastic about cash-out refinancing in its place technique of tapping residence fairness.

With a cash-out refinance, you’re taking out a brand new first mortgage that’s bigger than the stability in your present mortgage. The proceeds out of your new mortgage repay your present mortgage and your closing prices. You then get to maintain the remainder of the cash to make use of nevertheless you need.

A cash-out refinance generally is a good choice when prevailing mortgage charges are decrease than the speed you’re presently paying, you have got good credit score, and also you’re able to affording the brand new month-to-month mortgage funds.

Credible may also help you get began together with your cash-out refinance. Checking refinance charges on our platform is straightforward and solely takes a couple of minutes — and it gained’t impression your credit score rating.

Discover My Mortgage

No annoying calls or emails from lenders!

In regards to the writer

[ad_2]

Source link

{kind=link}