[ad_1]

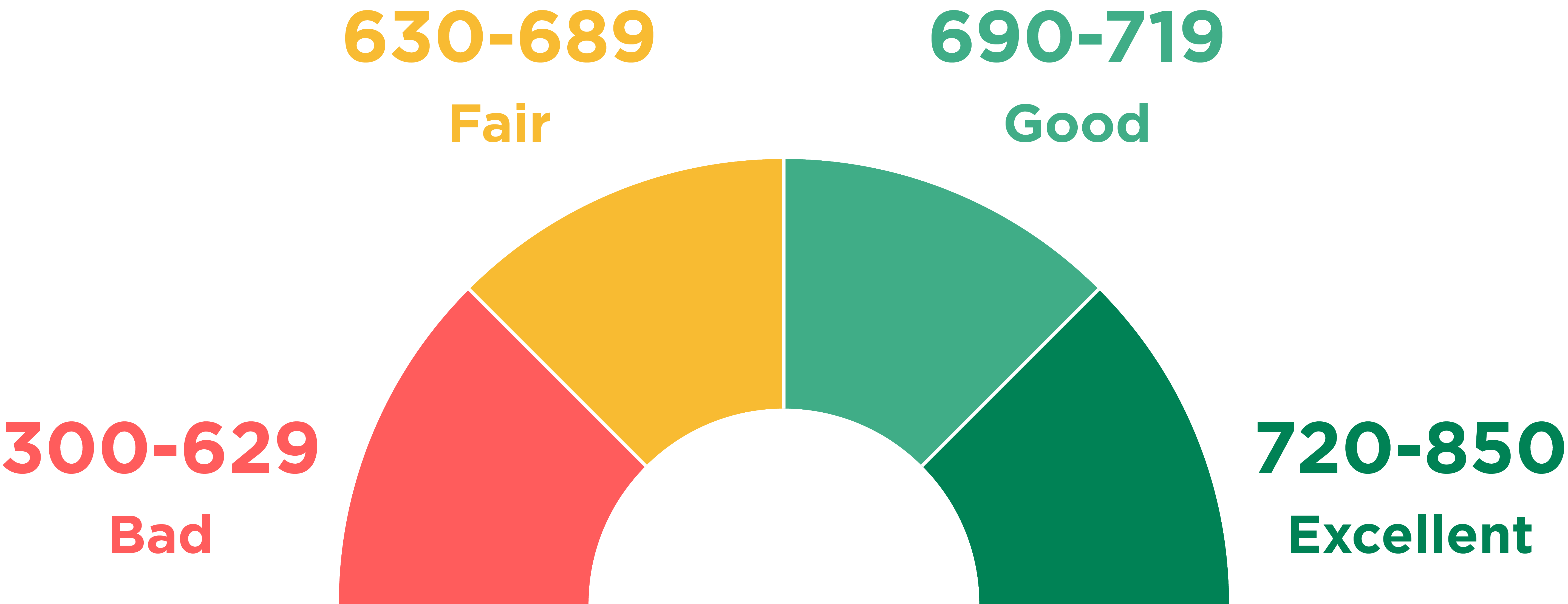

Credit score rating is a 3-digit quantity that calculates and charges your monetary situation based mostly in your credit score historical past. Lenders have a look at your credit score rating to determine whether or not to approve or reject your mortgage utility and what rate of interest must be levied in your mortgage. If you’re planning to use for a private mortgage, residence mortgage, enterprise mortgage, or every other mortgage product, examine your credit score rating first and be certain that it’s greater than 725. In any other case, the lender might understand you as an irresponsible borrower and reject your mortgage utility.

MUST-READ: 8 TIPS FOR GETTING THE BEST HOME LOAN EXPERIENCE WITH CLIX CAPITAL

Lenders rely closely in your credit score rating to offer you mortgage approval. Let’s discover out what your credit score rating says about you.

Know About Credit score Rating

Credit score rating ranges from 300 to 900, which you get based mostly in your invoice and EMI repayments and credit score historical past. A credit score rating above 725 is taken into account good and is sufficient to get your mortgage approval. The upper rating you could have, the larger probability it’s important to get mortgage approval with decrease rates of interest. Lenders have a look at your credit score rating to evaluate your credit score threat and get an concept of your compensation habits.

What Does Your Credit score Rating Reveal?

Your credit score rating says rather a lot about you when it comes to your credit score historical past. It reveals the next parameters relying on which the lender understands what sort of borrower you might be:

Fee Historical past

When the lenders approve your mortgage utility, the very first thing they need to guarantee is will they get again their cash simply or not. They take the next components into consideration whereas your credit score historical past:

-

- Do you pay your bank card payments and present mortgage EMIs on time? Late and missed funds are detrimental to your credit standing.

- If you happen to paid late, how late had been you? 30, 60, 90 days, or much more? The extra delay you make in your funds, the more serious your credit score rating will get.

- Have you ever acquired any assortment accounts? Lenders usually take it as a crimson flag, seeing that you simply didn’t pay again your mortgage quantity.

Quantities You Owe

The quantities that you simply owe are the second most important half that lenders have a look at. These embody the next issues:

-

- How a lot do you owe within the type of accounts like residence loans, mortgages, bank cards, fee accounts, and so on.?

- What’s the whole quantity you owe and the way a lot quantity you pay each month in direction of EMIs?

- What proportion of usable credit score did you really use? Your credit score rating signifies how accountable you might be in direction of your funds and are you financially safe to repay your mortgage quantity if permitted.

Length of Your Credit score Historical past

Your credit score rating reveals how lengthy you could have been utilizing credit score issues rather a lot to your credit score rating. What number of years have you ever been in commitments? What’s the age of all of your accounts on a median? How outdated is your oldest account?

New Credit score Accounts

Your credit score rating can be based mostly on what number of new credit score accounts you could have. The lender appears to be like at what number of new accounts you could have utilized for and opened over the previous couple of months.

Types of Credit score in Use

Your credit score rating reveals what number of completely different types of credit score you could have, similar to retailer accounts, bank cards, mortgages, revolving loans, and so on. The extra numerous your credit score profile is, the extra reliable you seem like as a borrower, that when you handle all of them nicely.

Contemplating Making use of for a Mortgage? Listed here are a Few Tricks to Observe

-

- Attempt to pay all of your bank card payments and mortgage EMIs on time. Whether it is inevitable, don’t be later than 30 days.

- Don’t open too many new accounts inside 12 months, as it might pose you as a credit-hungry borrower.

- If you’re planning to take a house mortgage or one other mortgage for a giant buy, examine your credit score rating not less than 6 months upfront. This offers you sufficient time to enhance the rating whether it is lower than 725.

- Use solely 15-25% of your whole obtainable credit score, as a low credit score utilization ratio will allow you to get a mortgage simply.

All in all, your credit score rating performs an important function in getting mortgage approvals at one of the best rate of interest. Lenders need to see a excessive credit score rating of minimal 725 to get an concept of your creditworthiness. If it’s lower than that parameter, use the information talked about right here to enhance your credit score rating earlier than making use of for a mortgage. A low credit score rating might result in outright mortgage rejection, which might additional cut back your rating and make it much more tough so that you can get a mortgage sooner or later.

In search of a private mortgage, residence mortgage, or enterprise mortgage? Clix Capital will be your greatest credit score supplier. Nonetheless, examine your credit score rating and be certain that it’s greater than 725. A excessive rating will say rather a lot about you whether or not you’ll be able to deal with your credit score with accountability or not.

For any queries, discover us on Fb, Instagram, LinkedIn, Twitter, or WhatsApp

You too can attain out to us at good day@clix.capital or name us at 1800 200 9898

[ad_2]

Source link

{kind=link}