[ad_1]

Scholar mortgage curiosity is usually a complicated matter. On the floor, pupil loans can appear to be every other installment mortgage, similar to a mortgage or automotive mortgage.

For personal pupil loans, that’s just about the case. However federal pupil mortgage curiosity can work otherwise than every other kind of mortgage as a consequence of distinctive subsidies and compensation plans.

On this information, we’ll take a deep dive into the mechanics of pupil mortgage curiosity for quite a lot of conditions. Right here’s how pupil mortgage curiosity truly works.

Understanding easy curiosity vs. compound curiosity

The nuances of pupil mortgage curiosity rely closely on the variations between easy curiosity and compound curiosity. Curiosity guidelines rely in your mortgage kind and your compensation plan. Let’s check out how the mathematics works for each forms of curiosity.

Notice that for the examples under we’ll assume that you’ve got a hard and fast rate of interest in your pupil loans. All federal loans include fastened charges. Nevertheless, your pupil loans might have variable charges in the event that they have been disbursed by a personal lender.

How easy curiosity works

With easy curiosity, the rate of interest is multiplied by the principal to seek out how a lot curiosity you’ll owe per 12 months.

For instance, with a $50,000 mortgage and a 5% easy rate of interest, you’d owe $2,500 in curiosity per 12 months ($50,000 x 0.05 = $2,500). And, over a 10-year interval, your whole curiosity accrual would equal $25,000.

Installment loans like mortgages, automotive loans, and private loans sometimes use easy curiosity formulation. So long as you pay the mortgage as agreed, curiosity solely accrues on the principal, not on accrued curiosity as nicely.

Learn how to calculate compound curiosity

Compound curiosity works otherwise than easy curiosity. With compound curiosity, the curiosity you accrue is added to your steadiness every month, day or no matter frequency the lender units. That is the method for calculating compound curiosity:

Compound curiosity = P [(1 + i)n – 1]

Let’s outline the varied phrases within the compound curiosity method:

- P stands for precept

- i stands for rate of interest

- n stands for the variety of compounding intervals

So let’s say you wished to calculate how a lot compound curiosity you’d accrue on $50,000 in pupil mortgage precept with 5% curiosity compounded yearly over 10 years. Right here’s the way you’d use the above method to seek out that quantity.

Compound curiosity = P [(1 + i)n – 1]

$50,000 [(1 + 0.05)10 – 1]

$50,000 [0.6289]

Compound curiosity = $31,445

So we see that utilizing a compound curiosity method resulted in an additional $6,000 of whole curiosity when in comparison with the easy curiosity calculation.

And, keep in mind, in our instance we assumed that curiosity would compound yearly. With extra frequent compounding schedules, the variations could be much more pronounced.

How pupil mortgage curiosity truly works

Scholar mortgage curiosity usually compounds every day. However, earlier than you panic, that doesn’t imply your steadiness will likely be rising every month (as can occur with bank cards).

In case you pay your federal loans in line with the 10-12 months Customary Compensation Mortgage or your personal loans in line with your mortgage phrases, your mortgage steadiness will solely go down over time and also you received’t accrue unpaid curiosity.

However what about instances that you simply’re not paying towards your pupil loans, like throughout college, throughout a grace interval, or throughout a interval of forbearance? In lots of circumstances, interest will continue to accrue throughout these intervals.

Once you start compensation, that accrued curiosity could capitalize, which implies it will get added to your principal steadiness. So, from that time ahead, you’ll be paying curiosity in your curiosity.

How pupil mortgage curiosity works on income-driven compensation plans

Federal pupil mortgage income-driven repayment (IDR) plans provide a novel profit that isn’t accessible with personal loans.

On an IDR plan, unpaid curiosity doesn’t capitalize so long as you’re on the plan. As a substitute, easy curiosity is charged in your excellent principal always.

This element is an enormous deal. Many debtors on IDR plans could not even be paying sufficient annually to cowl their curiosity expenses. With a typical compensation plan, this unpaid curiosity would capitalize and get added to your principal. However with IDR plans, your annual curiosity accrual doesn’t improve over time.

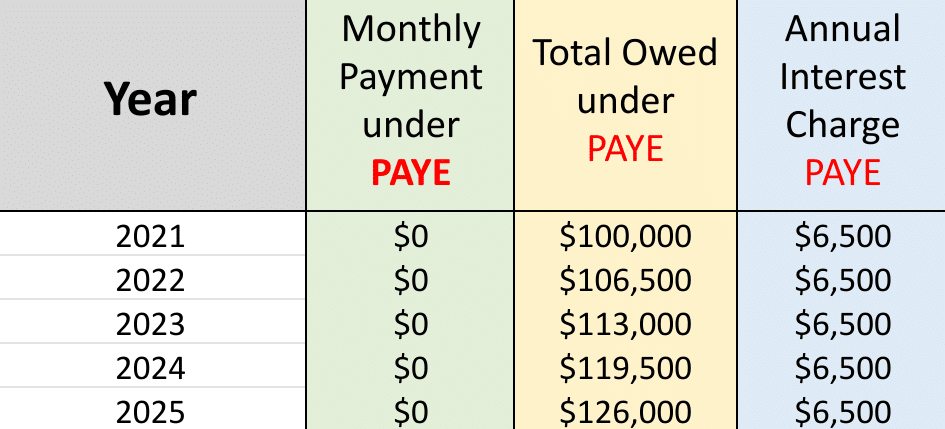

Your efficient rate of interest can lower over time

For instance, think about that you’ve got $100,000 in pupil loans at a 6.5% rate of interest. You’re on the PAYE plan, and your month-to-month cost quantity is $0. In 12 months 1, you’d accumulate $6,500 in curiosity. And that’s precisely the identical quantity of curiosity you’d accumulate in 12 months 5.

So, although your steadiness could be rising, your annual curiosity expenses would stay the identical.

Because of this your efficient rate of interest truly goes down as your pupil mortgage steadiness goes up on an IDR plan.

How pupil mortgage curiosity works in case you qualify for a subsidy

In sure conditions, college students could qualify for subsidies that may scale back their pupil mortgage curiosity accrual. Listed below are the 2 commonest forms of pupil mortgage curiosity subsidies:

1. Subsidies for particular pupil loans

Some pupil loans don’t accumulate curiosity whereas the coed is at school. For instance, with Direct Sponsored Loans, the Division of Schooling pays your student loan interest for you whilst you’re at school and through your six-month grace interval.

Notice that solely undergraduate college students are eligible for backed loans. And even undergrads might want to exhibit monetary want on their Free Utility for Federal Scholar Help (FAFSA) to qualify. Sponsored pupil loans even have decrease borrowing limits than different federal pupil mortgage choices.

Some loans which might be particularly designed for sure skilled college students may additionally provide this profit. The Well being Professions Scholar Mortgage Program is a outstanding instance. These loans don’t start to accrue curiosity till after the coed has graduated and a one-year grace interval has elapsed.

Scholar mortgage curiosity on different federal pupil loans

You received’t obtain the profit described above on a Direct Unsubsidized Mortgage, PLUS Mortgage, or Direct Consolidation Mortgage. With these pupil loans, curiosity will start accruing instantly, even in case you aren’t required to make funds till after you graduate.

That accrued curiosity will likely be added to your steadiness as soon as compensation begins. You’ll be able to keep away from this potential monetary influence by making interest-only funds whilst you’re at school.

2. Subsidies for particular compensation plans

Some IDR plans provide pupil mortgage curiosity subsidies as nicely. With the PAYE, IBR, and REPAYE plans, the federal government can pay the entire unpaid curiosity in your backed pupil loans for the primary three years of your compensation.

Curiosity subsidies on the REPAYE plan

The REPAYE plan is the actual star of the coed mortgage curiosity subsidy present. For debtors on the REPAYE plan, the federal government will proceed to pay 50% of the unpaid curiosity in your backed loans after your preliminary three-year interval finish. And it’ll at all times pay half of your unsubsidized pupil loans’ unpaid curiosity throughout all intervals as nicely.

This particular profit makes REPAYE an excellent possibility for debtors who want to maximize IDR pupil mortgage forgiveness. As a result of, keep in mind, debtors on IDR plans will more than likely owe tax on their forgiven quantities.

With REPAYE, you possibly can scale back the quantity of curiosity that’s added to your steadiness annually by 50%. And that might have a major influence in your IDR forgiveness student loan tax bomb.

Scholar mortgage curiosity FAQs

How typically is curiosity added to pupil mortgage balances?

College students loans usually accrue curiosity every day.

Once you’re paying down your loans, the quantity of curiosity you pay every month will go down. However during times of non-payment, your pupil mortgage curiosity can compound every day.

How a lot of my mortgage cost is curiosity?

The quantity of your cost that goes towards curiosity is highest at the start of your amortization schedule. However it goes down over time.

Debtors can accrue unpaid curiosity throughout forbearance or deferment intervals. In case you’ve accrued unpaid curiosity, your cost will likely be utilized towards that excellent principal steadiness. For that reason, 100% of your pupil mortgage cost might go towards curiosity in some circumstances.

How can I keep away from paying curiosity on pupil loans?

When a pupil mortgage is in regular compensation, it’s inconceivable to keep away from curiosity expenses utterly. However debtors can scale back the curiosity they pay over the lifetime of the mortgage by refinancing to a lower interest rate.

College students also can make interest-only funds during times of non-payment, like throughout tutorial deferment and style intervals. This will reduce curiosity capitalization later after the coed graduates and begins regular compensation.

How do I calculate my pupil mortgage curiosity?

To calculate your pupil mortgage curiosity, comply with these steps:

- Divide your annual rate of interest by 365 to seek out your day by day rate of interest.

- Subsequent, multiply your day by day rate of interest by your principal to seek out your day by day curiosity cost.

- Subsequent, multiply that quantity by your billing cycle (sometimes 30 days).

- Lastly, multiply that quantity by 12 to get your annual curiosity value.

How do pupil mortgage curiosity subsidies work?

Scholar mortgage subsidies permit debtors to keep away from unpaid curiosity being added to their principal.

With Direct Sponsored Loans, the Division of Schooling pays unpaid curiosity on the coed’s behalf. And debtors could qualify for pupil mortgage curiosity subsidies by getting on an IDR plan.

Get solutions to extra questions on your pupil loans

Scholar mortgage curiosity works like a traditional mortgage in case you’re making funds (both to the federal government or a personal lender) in line with the traditional schedule. Nevertheless, there are essential variations that don’t exist with other forms of debt.

You might be coping with easy curiosity, compound curiosity, or backed curiosity relying on what sort of compensation plan you’re utilizing and what your revenue is.

In case you take a look at conventional debt compensation recommendation, it’s worthwhile to perceive the distinctive pupil mortgage guidelines or you might make a mistake.

We’re the coed mortgage consultants. Speak to our professionals for recommendation on tips on how to reduce your curiosity value. Book a consultation today.

Refinance pupil loans, get a bonus in 2021

$1,050 BONUS1For 100k+. $300 bonus for 50k to 99k.1

$1,000 BONUS2 For 100k or extra. $200 for 50k to $99,9992

$1,050 BONUS3For 100k+. $300 bonus for 50k to 99k.3

$1,275 BONUS4 For 150k+. Tiered 300 to 575 bonus for 50k to 149k.4

$1,000 BONUS5For 100k+. $300 bonus for 50k to 99k.5

$1,000 BONUS6For $100k or extra. $200 for $50k to $99,9996

$1,250 BONUS7 For 100k+ or $350 for 5k to 100k.7

$1,250 BONUS8For 150k+. Tiered 100 to 400 bonus for 25k to 149k.8

Unsure what to do together with your pupil loans?

Take our 11 query quiz to get a personalised advice of whether or not you must pursue PSLF, IDR forgiveness, or refinancing (together with the one lender we expect might provide the finest price).

All charges listed above characterize APR vary. 1Commonbond: In case you refinance over $100,000 by this website, $500 of the money bonus listed above is supplied instantly by Scholar Mortgage Planner. Commonbond disclosure. 2Earnest: $1,000 for $100K or extra, $200 for $50K to $99.999.99. For Earnest, in case you refinance $100,000 or extra by this website, $500 of the $1,000 money bonus is supplied instantly by Scholar Mortgage Planner. Charge vary above consists of elective 0.25% Auto Pay low costEarnest disclosures.

3Laurel Street: In case you refinance greater than $250,000 by our hyperlink and Scholar Mortgage Planner receives credit score, a $500 money bonus will likely be supplied instantly by Scholar Mortgage Planner. If you’re a member of an expert affiliation, Laurel Street would possibly give you the selection of an rate of interest low cost or the $300, $500, or $750 money bonus talked about above. Gives from Laurel Street can’t be mixed. Charge vary above consists of elective 0.25% Auto Pay low cost. Laurel Road disclosures.

4Elfi: In case you refinance over $150,000 by this website, $500 of the money bonus listed above is supplied instantly by Scholar Mortgage Planner. Elfi disclosure. 5Splash: In case you refinance over $100,000 by this website, $500 of the money bonus listed above is supplied instantly by Scholar Mortgage Planner. Splash disclosure. 6Sofi: In case you refinance $100,000 or extra by this website, $500 of the $1,000 money bonus is supplied instantly by Scholar Mortgage Planner. Charge vary above consists of elective 0.25% Auto Pay low cost. Sofi disclosures. 7Credible: In case you refinance over $100,000 by this website, $500 of the money bonus listed above is supplied instantly by Scholar Mortgage Planner. Credible disclosure.

8LendKey: In case you refinance over $150,000 by this website, $500 of the money bonus listed above is supplied instantly by Scholar Mortgage Planner. Charge vary above consists of elective 0.25% Auto Pay low cost.

[ad_2]

Source link

{kind=link}