[ad_1]

Will mortgage charges go up in 2022?

Because the U.S. financial system continues to climb out of its Covid droop, and as inflation places upward strain on rates of interest, most consultants agree mortgage charges will climb greater in 2022.

Simply how excessive will they go? Trade sources are cut up on that. However they principally agree on 30-year charges within the high-3% to low-4% vary by the top of subsequent yr.

Meaning it’s in your finest curiosity to purchase or refinance early in 2022 for those who’re banking on as we speak’s low charges that will help you save.

Get started shopping for mortgage rates (Dec 1st, 2021)

On this article (Skip to…)

Overview of 2022 mortgage charges forecast

We interviewed eight mortgage, housing, and finance professionals to get their mortgage charge forecasts for 2022.

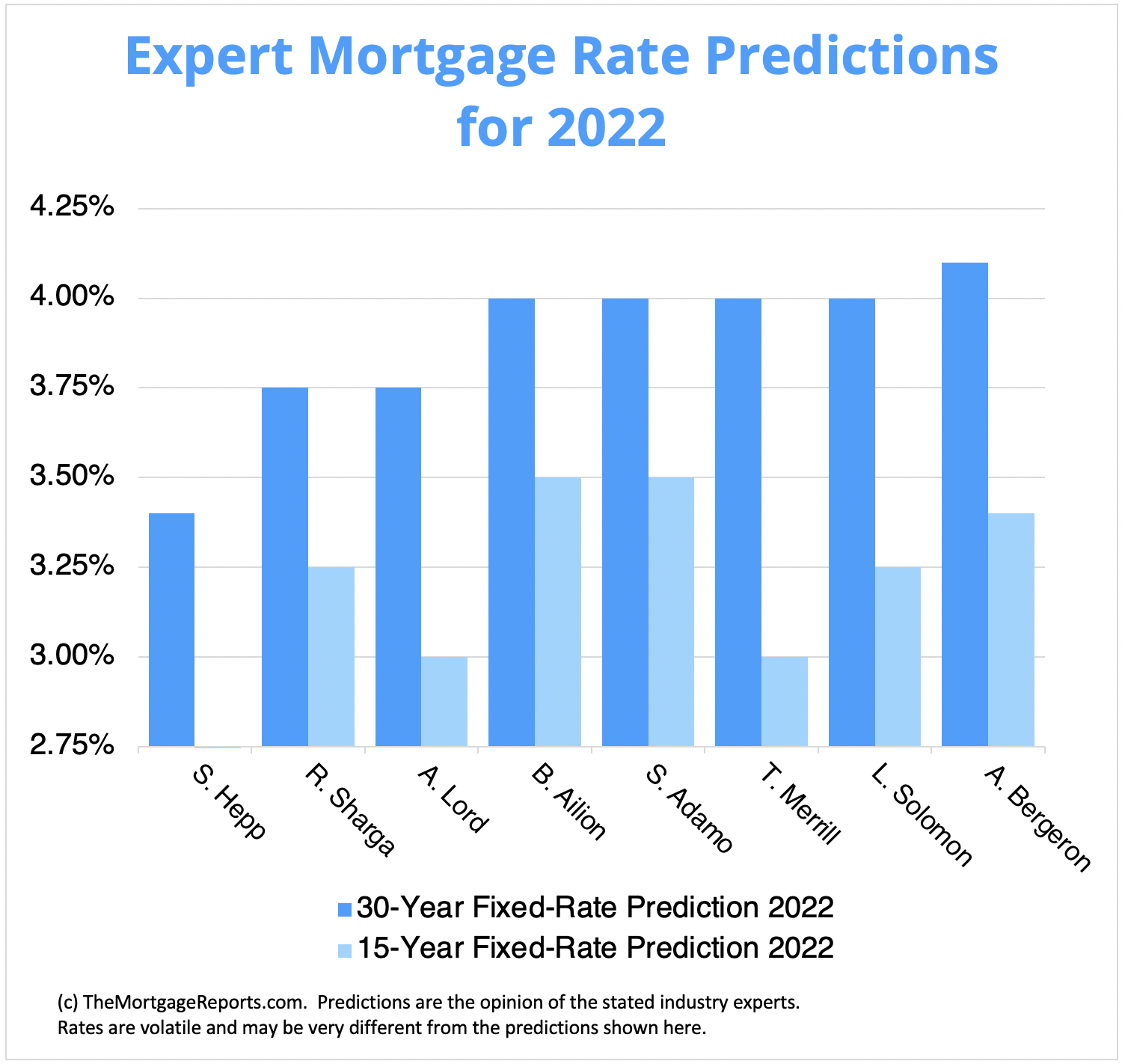

By the top of subsequent yr, these trade consultants predict 30-year mounted mortgage charges might rise to between 3.4% and 4.1%. With regards to 15-year mortgage charges, they predict a mean between 3.0% and three.5%.

Common rate of interest predictions put 30-year mounted charges at 3.88% and 15-year mounted charges at 3.27% in 2022.

| Trade Professional | 30-Yr Mounted-Charge Prediction 2022 | 15-Yr Mounted-Charge Prediction 2022 |

| Selma Hepp (CoreLogic) | 3.40% | N/A |

| Rick Sharga (RealtyTrac) | 3.75% | 3.25% |

| Al Lord (Lexerd Capital Administration) | 3.75% | 3% |

| Bruce Ailion (Realtor) | 4% | 3.50% |

| Stephen Adamo (Embrace House Loans) | 4% | 3.50% |

| Than Merrill (FortuneBuilders) | 4% | 3% |

| Lyle Solomon (Oak View Legislation Group) | 4% | 3.25% |

| Andreis Bergeron (Awning.com) | 4.10% | 3.40% |

| Common Prediction | 3.88% | 3.27% |

Put in perspective, it’s vital to keep in mind that mortgage rates of interest have remained comparatively reasonably priced. And for the foreseeable future, they shouldn’t stray too removed from all-time lows.

Ponder that, 40 years in the past, mortgage rates of interest were close to 17%. With that in thoughts, a rise to even 4% by the top of 2022 doesn’t appear too scary.

Find your lowest mortgage rate. Start here (Dec 1st, 2021)

Professional mortgage charge predictions for 2022

Trade consultants typically agree that mortgage charges will rise in 2022. However they’re cut up on simply how excessive charges will go. Listed here are 30- and 15-year mortgage charges forecasts from the eight professionals we interviewed, together with the reasoning behind their predictions.

Selma Hepp, deputy chief economist, CoreLogic

30–yr mortgage charges forecast: 3.4%

15–yr mortgage charges forecast: N/A

Selma Hepp, deputy chief economist for CoreLogic, says it’s straightforward to see the elements that can most likely drive mortgage charges greater in 2022.

“Inflation, authorities intervention within the housing market, the availability of properties on the market, and shopper debt will all play an element,” she says. “Additional gradual will increase in mortgage charges will likely be pushed by the broadening of inflation and inflationary expectations in addition to the continued provide shortages of labor, supplies, and power.”

With rather less demand and a bit extra provide subsequent yr, Hepp expects properties on the market will stay in the marketplace a bit longer with fewer competing bidders, which ought to average house value progress.

“CoreLogic’s House Value Index Forecast has the annual common rise in our nationwide value index slowing from about 15% in 2021 to five% in 2022,” she says.

Rick Sharga, govt vice chairman, RealtyTrac

30–yr mortgage charges forecast: 3.75%

15–yr mortgage charges forecast: 3.25%

“I believe it’s possible we’ll see mortgage charges improve in 2022,” says Rick Sharga, govt vice chairman at RealtyTrac.

He explains, “The largest query is whether or not as we speak’s excessive inflation is transitory, because the Biden Administration claims, or will likely be extra pervasive. Greater inflation virtually all the time ends in greater mortgage rates of interest. If the Federal Reserve Financial institution decides it must do one thing extra forceful to decelerate the speed of inflation, it is going to most likely elevate the Fed Funds charge, which creates a better charge atmosphere general.”

“If the Federal Reserve Financial institution decides it must do one thing extra forceful to decelerate the speed of inflation, it is going to most likely elevate the Fed Funds charge, which creates a better charge atmosphere general.”

Think about that the unfold between the yields on 10-year Treasuries and 30-year fixed-rate mortgages is beneath its historic stage of about 2 factors, so mortgage charges might transfer up a number of foundation factors if that relationship have been to easily revert to traditionally regular ranges subsequent yr, he provides.

“A number of elements might drive mortgage charges down in 2022. First, returns on many funding merchandise are nonetheless traditionally low. Central banks in numerous international locations deployed adverse rates of interest in 2021. Second, many worldwide economies are nonetheless pretty risky, and that usually drives investments towards US Treasuries in a flight to security, driving down yields, which might have an identical influence on mortgage charges,” Sharga says.

Al Lord, founder, Lexerd Capital Administration

30–yr mortgage charges forecast: 3.75%

15–yr mortgage charges forecast: 3%

Al Lord, founding father of Lexus Capital Administration, say two broadly talked about elements will affect the route of mortgage charges in 2022.

“The primary is the Fed’s tapering of the asset repurchases program. Decreasing asset repurchases creates much less cash provide available in the market and will increase curiosity and mortgage charges,” he says.

“Second is the scarcity of properties on the market and restricted new building exercise. The excessive house costs and the restricted provide of properties, both from resale or new building, will preserve the demand for mortgages decrease in comparison with 2021. Because of this, mortgage charges will have a tendency to stay close to the identical or marginally decline, I imagine. The results of these two counteracting elements will result in greater mortgage charges by the center of 2022, if not earlier.”

Anticipate inflation to speed up in 2022 whereas house costs proceed to escalate.

“That’s why my recommendation to owners is to buy a property prior to later and lock in nonetheless average mortgage charges,” provides Lord.

Bruce Ailion, actual property legal professional and Realtor

30–yr mortgage charges forecast: 4%

15–yr mortgage charges forecast: 3.5%

Bruce Ailion, a Realtor and actual property legal professional, isn’t very optimistic that 2022 charges will stay as enticingly low as they’ve been this yr.

“When inflation first appeared, it was hoped that it might be transitory. Right this moment, it’s thought-about baked into the long run,” he cautions. “The 2022 inflation charge is predicted to settle at 4.5%, hopefully receding to three.5% in 2023. Anticipated greater rates of interest will place strain on the Fed to gradual the financial system by rate of interest will increase.”

He reminds readers that the Fed has signaled the intent to extend charges by slowing their buy of presidency bonds, which can trigger charges general to extend subsequent yr.

“However charges might go lower-than-expected subsequent yr if we see a shopper backlash and unwillingness to pay greater costs. The labor pool that has been sitting on the sidelines of this restoration could reenter the workforce, as properly, slowing down wage inflation. These and different actions are unlikely to happen, nonetheless,” he explains.

Stephen Adamo, president of Nationwide Retail Manufacturing, Embrace House Loans

30–yr mortgage charges forecast: 4%

15–yr mortgage charges forecast: 3.5%

Stephen Adamo of Embrace House Loans additionally believes charges are more likely to improve in 2022, particularly with the Fed already starting its tapering of month-to-month bond purchases.

“That mentioned, a macroeconomic downside might gradual the rise in charges and probably even convey charges barely decrease. The information across the pandemic has improved, despite the fact that the nation is now seeing a rise in COVID instances. If the pandemic creates extra challenges subsequent yr, we might see charges lower from the place there are as we speak,” notes Adamo.

It’s extra possible that, by late subsequent yr, we’ll see a average charge improve of not less than 50 foundation factors greater than as we speak, he says.

Than Merrill, CEO, FortuneBuilders

30–yr mortgage charges forecast: 4.0%

15–yr mortgage charges forecast: 3.0%

The excellent news? Borrowing prices are nearly as engaging as they’ve ever been, in keeping with Than Merrill of FortuneBuilders. The dangerous information? “Inflation caused by authorities stimuli within the wake of a worldwide pandemic has pressured the Fed’s hand to extend borrowing prices,” he says.

For these and different causes, he predicts that charges usually tend to head north than go south by this time subsequent yr.

“If inflation proves to be transitory, it’s secure to imagine that rates of interest will improve at a quicker tempo than they did in 2021. It needs to be famous, nonetheless, that the Fed can’t improve rates of interest quicker than the financial system can strengthen. So whereas rates of interest are anticipated to rise, they almost definitely received’t improve dramatically,” Merrill explains.

Lyle Solomon, principal legal professional, Oak View Legislation Group

30–yr mortgage charges forecast: 4%

15–yr mortgage charges forecast: 3.25%

For Lyle Solomon, legal professional at Oak View Legislation Group, the equation is straightforward: “When shoppers can spend extra, which is true as we speak, they’ll afford to purchase properties. That will increase the demand for mortgages, which is more likely to occur in 2022,” he says.

Anticipated stronger financial progress, which can result in greater treasury yields, is the largest cause why Solomon anticipates a 4% common charge for a 30-year mortgage subsequent yr.

“Then again, if inflation will get beneath management, mortgage charges will go down,” he provides.

Andreis Bergeron, founding member/head of brokerage, Awning.com

30–yr mortgage charges forecast: 4.1%

15–yr mortgage charges forecast: 3.4%

Andreis Bergeron of Awning.com sees 30-year rates of interest shifting barely above 4% in 2022. Along with Federal Reserve coverage, the Fed Funds charge, and inflation, Bergeron factors the finger on the bond market, gross home product, and housing tendencies among the many parts that can influence mortgage rates of interest in 2022.

“Charges are anticipated to rise within the coming years pushed by the most important year-over-year inflation progress in 30 years and the truth that the Fed Funds are anticipated to hike charges,” he says.

Contemplating that inflation progress is principally double the place present mortgage charges sit, lenders will likely be pressured to extend charges to make a revenue margin on their merchandise subsequent yr, he continues.

Find your lowest mortgage rate. Start here (Dec 1st, 2021)

Do you have to wait to purchase a house till 2022?

Are you on the fence about buying a property? Remember the fact that low mortgage charges are useful, however they shouldn’t be your deciding issue. Think twice earlier than committing to a mortgage mortgage and locking in a charge till you might be financially prepared.

“Don’t make a nasty determination and rush into a house buy strictly to make the most of an rate of interest that’s, say, 0.5% higher than lately,” recommends Sharga.

“Nevertheless,” he provides, “it’s vital to remember that house costs are additionally more likely to proceed to rise in 2022, so ready to see if costs are rates of interest drop might value you when it comes to a better house value and a higher-priced mortgage.”

“Potential patrons ought to strongly contemplate shopping for at as we speak’s costs and charges as a result of they’re solely anticipated to go greater for the foreseeable future.”

Merrill seconds these sentiments.

“The present market atmosphere suggests borrowing prices and residential values will improve. Potential patrons ought to strongly contemplate shopping for at as we speak’s costs and charges as a result of they’re solely anticipated to go greater for the foreseeable future,” he says.

Think about one instance.

Say you’re shopping for a $300,000 house at as we speak’s common 30-year charge of three.10% (per Freddie Mac). With a 20% down cost, your month-to-month principal and curiosity cost would come out to $1,025.

Now think about you’re shopping for in late 2022 with a 3.75% rate of interest. The identical mortgage would value you $1,100 per thirty days, including $75 to your cost. And also you’d pay a further $31,190 in curiosity over 30 years.

To get one of the best rate of interest doable, remember to get your monetary home so as first, suggests Hepp.

“Paying down your excellent debt on bank cards, auto loans, and scholar debt will allow you to receive approval for a mortgage mortgage,” says Hepp.

Moreover, verify your credit score rating and work to enhance a low quantity.

“In case your rating is excessive, you might be more likely to qualify for decrease rates of interest. So work to spice up your credit score rating by decreasing your credit score utilization ratio, eradicating adverse objects out of your credit score report, and paying off your money owed,” advises Solomon.

Do you have to wait to refinance?

The consultants agree: The perfect transfer is to refinance sooner reasonably than later if you wish to reset your mortgage and capitalize on as we speak’s low rates of interest. With charges possible on the rise in 2022, potential financial savings for owners trying to refinance might be diminished.

“Attempt to refinance by the early months of 2022, not later,” says Lord.

Solomon says that rising rates of interest are anticipated to lower the variety of refinancing functions in 2022. It stands to cause, then, that there’s no time like the current to lock in a low refi charge.

“It’s most likely time to cease contemplating and begin shifting on that mortgage refinance utility,” agrees Sharga.

Get started on your home loan refinance (Dec 1st, 2021)

The underside line

With many consultants all forecasting charge hikes, chances are you’ll come to the conclusion that it’s higher to lock in a mortgage charge prior to later.

However always remember that even essentially the most educated consultants can’t forecast the long run with 100% accuracy. Mortgage rates of interest subsequent yr could go greater, might drop decrease, or could mirror what we see as we speak.

You will need to keep in mind that subsequent yr might produce completely different outcomes in charges — even downward motion.

When you purchase or refinance as we speak, you may all the time make the most of decrease charges once more sooner or later.

The ethical of the story? Don’t put your entire eggs in a single basket or take pointless dangers based mostly on hunches. Weigh your charge lock determination fastidiously and don’t attempt to completely time the market.

Crunch your financials, seek the advice of carefully with an skilled mortgage lending skilled, and strategize your short-and long-term homeownership plans earlier than pulling the set off.

[ad_2]

Source link

{kind=link}