[ad_1]

Will the Fed transfer to decrease rates of interest?

The Federal Reserve doesn’t management mortgage charges. Nevertheless it’s had an outsized influence on them in the course of the pandemic.

The Fed has bought billions of {dollars} price of shopper mortgages over the previous yr in a bid to maintain charges low throughout COVID. This — mixed with a common low-interest-rate coverage — helped hold mortgage charges at or close to file lows all through most of 2020 and the start of 2021.

However charges are starting to rise. And experts believe the Fed gained’t transfer to cease them.

Though it’s unwelcome information for debtors, charges are certain to rise because the economic system begins to enhance. And, as COVID turns into much less of a priority, the Fed will finally roll again its mortgage charge interventions and the 2 will resume a extra ‘regular’ relationship.

Find a low mortgage rate today (Mar 15th, 2021)

On this article (Skip to…)

What occurs at Federal Reserve conferences?

The Federal Open Market Committee (FOMC) sometimes meets each six weeks to debate rate of interest coverage.

The FOMC is a rotating, 12-person sub-committee inside the Federal Reserve, headed by Federal Reserve Chairman Jerome Powell.

The FOMC meets eight occasions yearly on a pre-determined schedule, and on an emergency foundation, when wanted, as was required between 2008-2011 when the U.S. economic system was staving off despair; and in 2013 when the U.S. authorities failed to boost its debt restrict.

The FOMC’s most well-known function worldwide is as keeper of the federal funds charge. However how precisely does the fed funds charge influence your pockets?

The Federal Reserve doesn’t management mortgage charges — normally

It’s a standard perception that the Federal Reserve “makes” shopper mortgage charges. The truth is, it doesn’t. Mortgage rates are made on Wall Street.

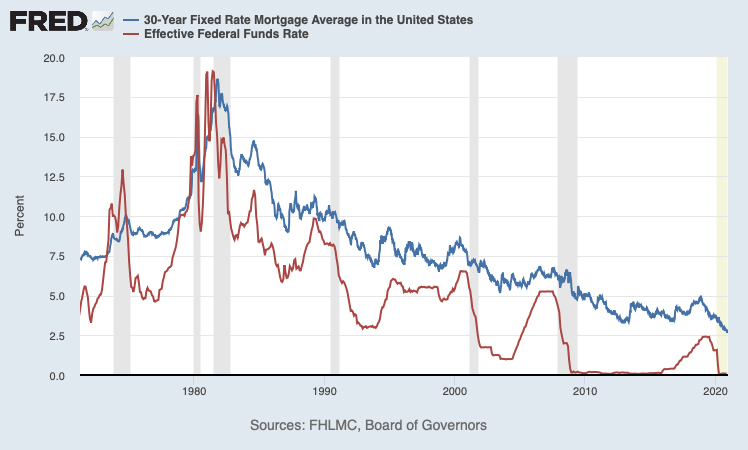

Right here’s proof: During the last twenty years, the fed funds charge and the common 30-year fastened mortgage charge have differed by greater than 5%, and by as little as 0.50%.

If the fed funds charge had been actually linked to U.S. mortgage charges, the distinction between the 2 charges could be linear or logarithmic — not jagged.

That mentioned, the Fed does affect at the moment’s mortgage charges.

After its scheduled conferences, the FOMC points a press launch to the general public which highlights the group’s financial opinions and consensus.

When the FOMC’s post-meeting press launch is usually “optimistic” on the U.S. economic system, mortgage charges are likely to rise. Conversely, when the Fed is usually unfavourable with its outlook, mortgage charges are likely to fall.

Financial information has been overwhelmingly unfavourable over the previous yr attributable to COVID. Consequently, rates of interest — together with mortgage charges — have stayed close to file lows.

However as an increasing number of Individuals get vaccinated, and the economic system begins to rebound because of this, these traits will reverse, and we’re prone to see mortgage charges rise.

Check your mortgage rates today (Mar 15th, 2021)

How the Fed has impacted mortgage charges these days

Usually, the Fed’s influence on mortgage charges is oblique at finest (as we’ll describe in additional element under).

However the Federal Reserve does have one avenue to instantly influence mortgage charges.

That’s by “quantitative easing” (QE).

QE occurs when the Fed injects cash into the U.S. economic system with a purpose to hold charges low — and by extension, hold shoppers borrowing cash and {dollars} circulating.

Simply have a look at what the Fed did within the early phases of the COVID-19 pandemic. Since March 2020, it’s purchased billions of {dollars} price of shopper mortgages on the secondary marketplace.

Extra capital within the secondary market means decrease charges for debtors. Because of the Fed’s cash injection, mortgage charges hit — and stayed at — file lows for over 9 months.

The traditional chorus you’ll hear from mortgage professionals — “the Fed doesn’t management mortgage charges” — remains to be true. Mortgage rates of interest are usually not instantly tied to the Fed Funds charge.

However that assertion now comes with an enormous asterisk, because it’s turn out to be clear what a big effect the Federal Reserve can have on rates of interest when want be.

Check your mortgage rates. Start here (Mar 15th, 2021)

What does it imply when the Federal Reserve cuts rates of interest?

The fed funds charge is the prescribed charge at which banks lend cash to one another on an in a single day foundation.

When the fed funds charge is low, the Fed is trying to promote financial development. It is because the fed funds destiny is correlated to Prime Charge, which is the premise of most financial institution lending together with many enterprise loans and shopper bank cards.

For the Federal Reserve, manipulating the fed funds charge is one solution to handle its dual-charter of fostering most employment and sustaining steady costs.

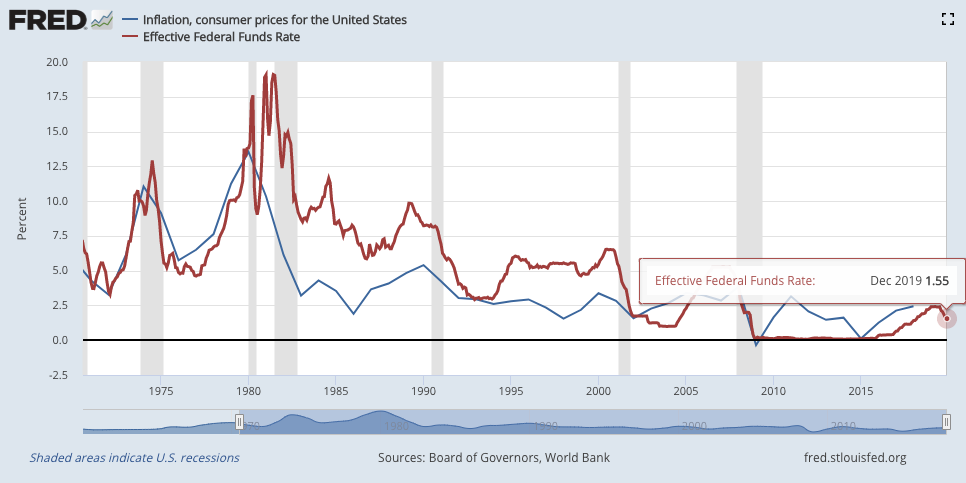

Federal funds charge and Shopper Worth Inflation, 1970-2018. Supply: St. Louis Fed

Nonetheless, a low fed funds charge creates wage strain and promotes risk-taking, each of which might rapidly result in inflation (rising costs).

For that reason, the Federal Reserve ended its zero-interest-rate coverage in December 2015, elevating charges by 25 foundation factors (0.25%) for the primary time in additional than a decade.

Nonetheless, the Fed transfer did not result in a rise in shopper mortgage charges. Quite the opposite, mortgage charges dropped greater than 50 foundation factors (0.50%) after the Fed’s late-2015 transfer.

It is because U.S. mortgage charges aren’t set or established by the Federal Reserve or any of its members. Relatively, mortgage charges are decided by the value of mortgage-backed securities (MBS), a safety bought on Wall Road.

The Federal Reserve can have an effect on at the moment’s mortgage charges, however it can not set them.

How Fed statements can influence mortgage charges

The Fed does extra than simply set the fed funds charge. It additionally provides financial steering to markets.

For charge buyers, one of many key messages to pay attention for is what the Fed says about inflation. Inflation is the enemy of mortgage bonds and, on the whole, when inflation pressures are rising, mortgage charges are rising.

The hyperlink between inflation charges and mortgage charges is direct, as owners within the early-Nineteen Eighties skilled.

Excessive inflation on the time led to the very best mortgage charges ever. 30-year mortgage charges went for over 17% (as a complete era of debtors will remind you), and 15-year loans weren’t a lot better.

The Fed doesn’t management mortgage charges, however the hyperlink between inflation and mortgage charges is direct.

Inflation is an financial time period describing the lack of buying energy. When inflation is current inside an economic system, extra of the identical forex is required to buy the identical variety of items.

We expertise inflation on the grocery retailer.

A gallon of milk used to value $2. At the moment, it prices $3. Extra cash is required to buy the identical quantity of milk as a result of every greenback holds much less worth.

In the meantime, mortgage charges are based mostly on the value of mortgage-backed securities (MBS) and mortgage-backed securities are U.S. dollar-denominated. Which means that a devaluation within the U.S. greenback will consequence within the devaluation of U.S. mortgage-backed securities as nicely.

When inflation is current within the economic system, then, the worth of a mortgage bond drops, which results in increased mortgage charges.

For this reason the Fed’s feedback on inflation are carefully watched by Wall Road. The extra inflationary pressures the Fed fingers within the economic system, the extra seemingly it’s that mortgage charges will rise.

Lock in rates before today’s Fed announcement (Mar 15th, 2021)

Federal Reserve FAQ

The Federal Reserve is the central financial institution of the U.S. It’s an impartial physique (not managed by the federal government) tasked with managing the nation’s forex and financial coverage and preserving the economic system steady. In additional relatable phrases, the Federal Reserve influences issues just like the rates of interest you pay on a bank card or enterprise mortgage. The Fed additionally has affect over the costs you pay for on a regular basis items and companies, because it helps handle inflation.

In broad strokes, the Fed’s job is to maintain American financial development steady. It does this by managing U.S. forex, setting rates of interest for lending, and preserving inflation in examine by quite a lot of financial insurance policies. Total, the Fed tries to maintain inflation and curiosity low sufficient that shopper companies and spending keep sturdy — however excessive sufficient that the economic system doesn’t stagnate.

The Federal Reserve was created in 1913, with the signing of the Federal Reserve Act. Within the Federal Reserve’s personal phrases, it was created to “present the nation with a safer, extra versatile, and extra steady financial and monetary system.” Put otherwise, the Fed makes use of its affect over financial coverage and banks to assist make sure the economic system doesn’t develop or shrink too rapidly. The aim is to maintain costs steady sufficient that buyers can afford to spend and borrow, and companies can keep afloat and supply regular employment.

Periodically, the Fed raises rates of interest. Extra particularly, it raises the federal funds charge, which in flip impacts debtors’ rates of interest on issues like bank cards and residential fairness loans, and, extra not directly, fixed-rate residence loans. So why does the Fed increase rates of interest in any respect? As a result of it helps hold inflation in examine. When charges are too low, low-cost borrowing can overheat an economic system. Costs rise as demand for items and companies goes up. However the Fed can counteract inflation by growing charges, thereby curbing consumption. Conversely, the Fed can struggle deflation by reducing rates of interest. Low cost cash spurs spending and demand for items, serving to to extend costs in an economic system.

The federal funds charge or “fed funds charge” is the rate of interest banks cost to lend cash to at least one one other in a single day. Why do you have to care what charge banks are charging one another? As a result of the fed funds charge impacts shopper borrowing, too. Take the fed funds charge, add 3% to it, and also you usually get the “prime charge” — which is the premise for setting charges on shopper credit score strains like auto loans, bank cards, and residential fairness loans. Not all rates of interest are in lock-step with the fed funds charge (mortgage charges are usually not, for instance), however they’re all influenced by it.

Importantly, no department of presidency controls the Federal Reserve. It’s an impartial physique made up of a Board of Governors and 12 Federal Reserve Banks throughout the nation. The seven board members, in addition to a rotating solid of Federal Reserve Financial institution presidents, make up the FOMC (Federal Reserve Open Market Committee) — the Fed’s governing physique. The FOMC meets each 8 weeks to guage rate of interest coverage.

What are at the moment’s mortgage charges?

The Federal Reserve adjourns from its scheduled assembly on Wednesday afternoon.

Present mortgage pricing isn’t predicted to vary, however there aren’t any ensures on the subject of rates of interest.

Check out at the moment’s actual mortgage charges now. Mortgage quotes are available and you can begin in minutes.

[ad_2]

Source link

{kind=link}