[ad_1]

How a lot do it’s a must to put down on a home?

First issues first: The concept you have to place 20 p.c down on a home is a delusion.

The common first-time dwelling purchaser places simply 6% down, and sure mortgage packages permit as little as 3% or even zero down.

You shouldn’t suppose it’s conservative to make a big down fee on a house, or dangerous to make a small down fee. The correct quantity relies on your present financial savings and your house shopping for targets.

If you should buy a home with much less cash down and turn into a home-owner sooner, that’s typically the fitting selection.

Verify your low-down-payment loan eligibility (May 6th, 2021)

On this article (Skip to…)

How a lot is a down fee on a home?

How a lot down fee you want for a home relies on which sort of mortgage you get.

The preferred mortgage possibility, a traditional mortgage, begins at 3% to five% down. On a $250,000 home, that’s a $7,500-$12,500 down fee.

However to keep away from private mortgage insurance on one among these loans (which prices additional each month) you want 20% down. That’s $50,000 on a $250,000 dwelling.

FHA loans allow you to purchase with 3.5% down, which might be $8,750 on the identical home.

Some mortgage varieties will even allow you to purchase with zero down.

These embrace government-backed USDA and VA loans, which allow you to finance 100% of the house value and put $0 towards the acquisition value. Nonetheless, you’ll doubtless nonetheless need to cowl some or all your upfront closing costs with money.

So, you solely want to place down round 3-5% usually. However that begs the query: How a lot cash ought to you set down?

How a lot do you have to put down on a home?

Must you put 20% down on a home, although it’s not required? In lots of circumstances, the reply is not any. In actual fact, most individuals put solely 6-12% down. However the correct amount relies on your scenario.

For example: When you have some huge cash saved up within the financial institution, however comparatively low revenue, making the most important down fee potential will be sensible. That’s as a result of a big down fee shrinks your mortgage quantity and reduces your month-to-month mortgage fee.

Or perhaps your scenario is reversed.

Possibly you’ll have a superb family revenue however little or no saved within the financial institution. On this occasion, it could be greatest to make use of a low- or no-down-payment loan, whereas planning to cancel your mortgage insurance at some level sooner or later.

On the finish of the day, the “proper” downpayment relies on your funds and the house you intend to purchase.

Check your down payment options (May 6th, 2021)

Advantages of a 20% down fee

A big down fee helps you afford extra home with the identical month-to-month revenue.

Say a purchaser desires to spend $1,000 per thirty days for principal, curiosity, and mortgage insurance coverage (when required). Making a 20% down fee as an alternative of a 3% down fee raises their dwelling shopping for funds by over $100,000 — all whereas sustaining the identical month-to-month fee.

Right here’s how a lot home the homebuyer on this instance should purchase at a 4% mortgage price. The house value varies with the quantity the customer places down.

| Down Fee (%) | Down Fee ($) | Month-to-month Fee (Principal & Curiosity / PMI) | Residence Worth You Can Afford |

| 3% | $884 / $116 | $154,500 | |

| 5% | $8,780 | $896 / $104 | $175,500 |

| 10% | $91,310 | $913 / $87 | $193,000 |

| 20% | $52,370 | $1,000 / $0 | $261,500 |

Despite the fact that a big down fee can assist you afford extra, certainly not ought to dwelling patrons use their final greenback to stretch their down fee stage.

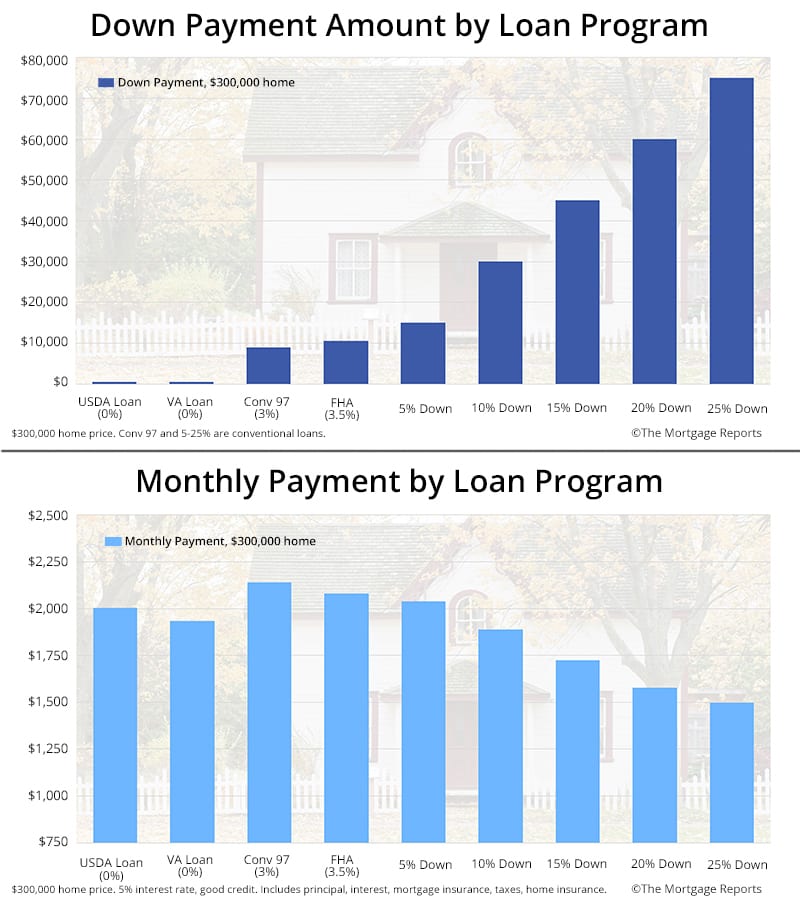

And, because the charts beneath present, you don’t save a ton of cash every month by placing lots down.

Making a $75,000 down fee on a $300,000 dwelling, you solely save $500 per thirty days in comparison with a zero-down mortgage.

Drawbacks of placing 20% down

As a house owner, it’s doubtless that your dwelling can be your largest asset. The property could even be price greater than all of your different investments mixed.

On this method, your house is each a shelter and an funding. And as soon as we view our dwelling as an funding, it may information the choices we make about our cash.

The riskiest resolution we are able to make when buying a brand new dwelling? Making too huge of a down fee.

A giant down fee will decrease your price of return

The primary purpose why conservative buyers ought to monitor their down fee measurement is that the down fee will restrict your dwelling’s return on funding.

Think about a house which appreciates on the nationwide common of close to 5 p.c.

In the present day, your house is price $400,000. In a 12 months, it’s price $420,000. No matter your down fee, the house is price twenty-thousand {dollars} extra.

That down fee affected your price of return.

- With 20% down on the house — $80,000 –your price of return is 25%

- With 3% down on the house — $12,000 — your price of return is 167%

That’s an enormous distinction.

Nonetheless! We should additionally think about the upper mortgage price plus necessary non-public mortgage insurance coverage which accompanies a traditional 3%-down mortgage like this. Low-down-payment loans can price extra every month.

Assuming a 175 foundation level (1.75%) bump from price and PMI mixed, we discover {that a} low-down-payment house owner pays an additional $6,780 per 12 months to stay in its dwelling.

With three p.c down, and making an adjustment for price and PMI, the speed of return on a low-down-payment mortgage is nonetheless 105 p.c.

The much less you set down, the bigger your potential return on funding.

Check your eligibility for a low down payment loan (May 6th, 2021)

When you make your down fee, you’ll be able to’t get the cash again simply

There are different down fee issues, too.

When you make a down fee, you’ll be able to’t entry that cash until you promote the home or take out a mortgage towards it.

It’s because, on the time of buy, no matter down fee you make on the house will get transformed instantly from money into a distinct kind of asset often called ‘dwelling fairness.’

Home equity is the financial distinction between what your house is price on paper, and what’s owed to the financial institution.

Not like money, dwelling fairness is an ‘illiquid asset,’ which signifies that it may’t be readily accessed or spent.

All issues equal, it’s higher to carry liquid belongings as an investor as in comparison with illiquid belongings. In case of an emergency, you should utilize your liquid belongings to alleviate among the strain.

It’s among the many the explanation why conservative buyers favor making as small of a down fee as potential.

While you make a small down fee, you retain your money in your pocket reasonably than tying it up in actual property.

In contrast, if you make a big down fee, these monies get tied up with the financial institution and you may solely entry them by promoting, refinancing, or taking out a house fairness mortgage.

It’s good to make a big down fee as a result of it lowers your month-to-month fee — you’ll be able to see that on a mortgage calculator. However if you make a big down fee on the expense of your personal liquidity, you could put your self in danger.

You’re in danger when your house worth drops

A 3rd purpose to think about a smaller down fee is the hyperlink between the economic system and U.S. dwelling costs.

Basically, because the U.S. economic system improves, dwelling values rise. And, conversely, when the U.S. economic system sags, dwelling values sink.

Due to this hyperlink between the economic system and residential values, patrons who make a big down fee discover themselves over-exposed to an financial downturn as in comparison with patrons whose down funds are small.

We are able to use a real-world instance from final decade’s housing market downturn to focus on this sort of connection.

Think about the acquisition of a $400,000 dwelling and two dwelling patrons, every with totally different concepts about the right way to purchase a house.

One purchaser is makes a twenty p.c down fee to be able to keep away from paying non-public mortgage insurance coverage to their financial institution. The opposite purchaser desires to remain as liquid as potential, selecting to make use of the FHA mortgage program, which permits for a down fee of simply 3.5%

On the time of buy, the primary purchaser takes $80,000 from the financial institution and converts it to illiquid dwelling fairness. The second purchaser, utilizing an FHA mortgage, places $14,000 into the house.

Over the subsequent two years, the economic system takes a flip for the more serious. Residence values sink and, in some markets, values drop as a lot as twenty p.c.

The patrons’ houses are actually price $320,000 and neither house owner has a lick of dwelling fairness to its identify.

Nonetheless, there’s an enormous distinction of their conditions.

To the primary purchaser — the one who made the big down fee –$80,000 has evaporated into the housing market. That cash is misplaced and can’t be recouped besides via the housing market’s restoration.

To the second purchaser, although, solely $14,000 is gone. Sure, the house is “underwater” at this level, with extra money owed on the house than what the house is price, however that’s a threat that’s on the financial institution and never the borrower.

And, within the occasion of default, which house owner do you suppose the financial institution could be extra prone to foreclose upon?

It’s counter-intuitive, however the purchaser who made a big down fee is much less prone to get aid throughout a time of disaster and is extra prone to face eviction.

Why is that this true? As a result of when a home-owner has no less than some fairness, the financial institution’s losses are restricted when the house is offered at foreclosures. The house owner’s twenty p.c dwelling fairness is already gone, in any case, and the remaining losses will be absorbed by the financial institution.

Foreclosing on an underwater dwelling, in contrast, can result in nice losses. All the cash misplaced is cash lent or misplaced by the financial institution.

A conservative purchaser will acknowledge, then, that funding threat will increase with the dimensions of down fee. The smaller the down fee, the smaller the chance.

What’s a down fee?

In actual property, a down fee is the amount of money you set in the direction of the acquisition of dwelling.

Down funds range in measurement and are usually described in share phrases as in comparison with the sale value of a house.

For instance, when you’re shopping for a house for $400,000, you’re bringing $80,000 towards the acquisition, your down fee is 20 p.c.

Equally, when you introduced $12,000 money to your closing, your down fee could be 3%.

The time period “down fee” exists as a result of only a few individuals decide to pay for houses utilizing money. Their down fee is the distinction between they purchase and what they borrow.

Down fee necessities for mortgage loans

You’ll be able to’t simply select your down fee measurement at random.

Relying on the mortgage program for which you’re making use of, there’s going to be a specified minimal down fee quantity.

For right now’s most widely-used mortgage packages, down fee necessities are:

- FHA Mortgage (backed by the Federal Housing Administration): 3.5% down fee minimal

- VA Mortgage (backed by the Division of Veterans Affairs): No down fee required

- Fannie Mae HomeReady Mortgage: 3% down minimal

- Typical Mortgage (with PMI): 3% minimal

- Typical Mortgage (with out PMI): 20% minimal

- USDA Mortgage (backed by the U.S. Division of Agriculture): No down payment required

- Jumbo Mortgage: 10% down

Bear in mind, although, that these necessities are simply the minimal. As a mortgage borrower, it’s your proper to place down as a lot on a house as you want and, in some circumstances, it may make sense to place down extra.

Purchasing a condo with typical mortgage is one such situation.

Condominium mortgage charges are roughly 12.5 foundation factors (0.125%) decrease for loans the place the loan-to-value ratio (LTV) is 75% or much less.

Placing twenty-five p.c down on a rental, due to this fact, will get you entry to decrease rates of interest. So when you’re placing down twenty p.c, think about a further 5 and also you’ll doubtless get a decrease mortgage price.

Making a bigger down fee can shrink your prices with FHA loans, too.

Underneath the brand new FHA mortgage insurance rules, if you use a 30-year fastened price FHA mortgage and make a down fee of three.5 p.c, your FHA mortgage insurance coverage premium (MIP) is 0.85% yearly.

Nonetheless, if you improve your down fee to five p.c, FHA MIP drops to 0.80%. This might prevent cash every month and over the lifetime of the mortgage.

Verify your low down payment loan eligibility (May 6th, 2021)

What if I can’t afford the down fee?

Not everybody qualifies for a zero-down mortgage. Most debtors want no less than 3% down for a traditional mortgage or 3.5% down for an FHA mortgage.

However what when you can’t fairly afford the minimal down fee? Three p.c down on a $300,000 dwelling continues to be $9,000 — a substantial amount of cash.

Fortunately there are packages that may assist.

For instance, each state has a number of down payment assistance programs (DPA). These packages — typically funded by state and native governments and nonprofits — provide cash to make homeownership extra accessible for lower-income or deprived dwelling patrons.

DPA funds can come within the type of a grant or mortgage, and the loans are sometimes forgiven when you stay within the dwelling for a sure time period.

To seek out out whether or not you’re eligible for help, ask your Realtor or lender that will help you discover and apply for packages in your space.

20 p.c down fee FAQ

You would not have to place 20 p.c down on a home. In actual fact, the typical down fee for first-time patrons is simply 7 p.c. And there are mortgage packages that allow you to put as little as zero down. Nonetheless, a smaller down fee means a costlier mortgage long-term. With lower than 20 p.c down on a home buy, you’ll have a much bigger mortgage and better month-to-month funds. You’ll doubtless additionally need to pay for mortgage insurance coverage, which will be costly.

The “20 p.c down rule” is mostly a delusion. Sometimes, mortgage lenders need you to place 20 p.c down on a house buy as a result of it lowers their lending threat. It’s additionally a “rule” that almost all packages cost mortgage insurance coverage when you put lower than 20 p.c down (although some loans keep away from this). But it surely’s NOT a rule that it’s essential to put 20 p.c down. Down fee choices for main mortgage packages vary from 0% to three, 5, or 10% p.c.

It’s not at all times higher to make a big down fee on a home. In the case of making a down fee, the selection ought to rely by yourself monetary targets. It’s higher to place 20 p.c down if you would like the bottom potential rate of interest and month-to-month fee. However if you wish to get right into a home now and begin constructing fairness, it could be higher to purchase with a smaller down fee — say 5 to 10 p.c down. You may also need to make a small down fee to keep away from draining your financial savings. Bear in mind, you’ll be able to at all times refinance right into a decrease price with no mortgage insurance coverage afterward down the street.

It’s potential to keep away from PMI with lower than 20% down. If you wish to keep away from PMI, search for lender-paid mortgage insurance coverage, a piggyback mortgage, or a financial institution with particular no-PMI loans. However bear in mind, there’s no free lunch. To keep away from PMI, you’ll doubtless need to pay a better rate of interest. And plenty of banks with no-PMI loans have particular {qualifications}, like being a first-time or low-income dwelling purchaser.

The most important advantages of placing 20 p.c down on a home are having a smaller mortgage measurement, decrease month-to-month funds, and no mortgage insurance coverage. For instance, think about you’re shopping for a home price $300,000 at a 4% rate of interest. With 20 p.c down and no mortgage insurance coverage, your month-to-month principal and curiosity fee comes out to $1,150. With 10 p.c down and mortgage insurance coverage included, funds leap to $1,450 per thirty days. Right here, placing 20 p.c down as an alternative of 10 saves you $300 per thirty days.

It’s completely alright to put 10 p.c down on a home. In actual fact, first-time patrons put down solely 6 p.c on common. Simply be aware that with 10 p.c down, you’ll have a better month-to-month fee than when you’d put 20 p.c down. For instance, a $300,000 dwelling with a 4% mortgage price would price about $1,450 per thirty days with 10 p.c down, and simply $1,150 per thirty days with 20 p.c down.

The most important downside to placing 10 p.c down is that you just’ll doubtless need to pay mortgage insurance coverage. Although when you use an FHA mortgage, a ten p.c or larger down fee shortens your mortgage insurance coverage time period to 11 years as an alternative of the complete mortgage time period. Or you’ll be able to put simply 10% down and keep away from mortgage insurance coverage with a “piggyback mortgage,” which is a second, smaller mortgage that acts as a part of your down fee.

What are right now’s mortgage charges?

In the present day’s mortgage charges are nonetheless at historic lows, even for debtors with lower than 20% down. In actual fact, debtors with low-down-payment authorities loans typically get entry to below-market charges.

So don’t write off dwelling shopping for since you’re ready to avoid wasting 20% down. Many patrons can qualify right now and don’t even realize it.

[ad_2]

Source link

{kind=link}