[ad_1]

Whether or not you’ve already refinanced your student loans to save cash on curiosity otherwise you’re desirous about it, you would possibly surprise — “How typically are you able to refinance scholar loans?”

The reply is as many occasions as you need. You may proceed your quest to attain the bottom price doable till your whole debt is gone. Whether or not refinancing scholar loans a number of occasions is a technique you ought to do is a distinct story.

On this information, we’ll cowl some examples of when it is smart to refinance a number of occasions, when it is best to maintain off and tips on how to get began.

Are you able to refinance a refinanced scholar mortgage?

Our February 2021 scholar mortgage refinancing survey confirmed that consciousness round refinancing a number of occasions is growing with 69% of respondents saying that they knew refinancing scholar loans a number of occasions was doable. In distinction, our December 2019 refinancing survey discovered that solely 60% of respondents knew they might refinance greater than as soon as.

Once you refinance a scholar mortgage, you’re taking out a brand new personal mortgage with a selected refinancing lender. Meaning if in case you have federal scholar loans, you forego borrower advantages throughout reimbursement, akin to forgiveness and income-driven reimbursement, in change for decreasing your rates of interest. In decreasing your rate of interest, you may shave off years of reimbursement and save a great chunk of cash.

However refinancing your scholar mortgage doesn’t need to be a one-and-done technique. Refinancing scholar loans a number of occasions is feasible and, actually, we suggest it.

Often refinancing scholar loans could make monetary sense

By the refinancing ladder strategy, you begin out with a long term and refinance a number of occasions extra with shorter reimbursement phrases. This technique works for those who use that saved cash in curiosity and throw extra towards your principal steadiness.

Pupil mortgage refinancing is the one significant option to considerably cut back your rate of interest (autopay reductions can account for a 0.25% discount). Let’s check out some examples:

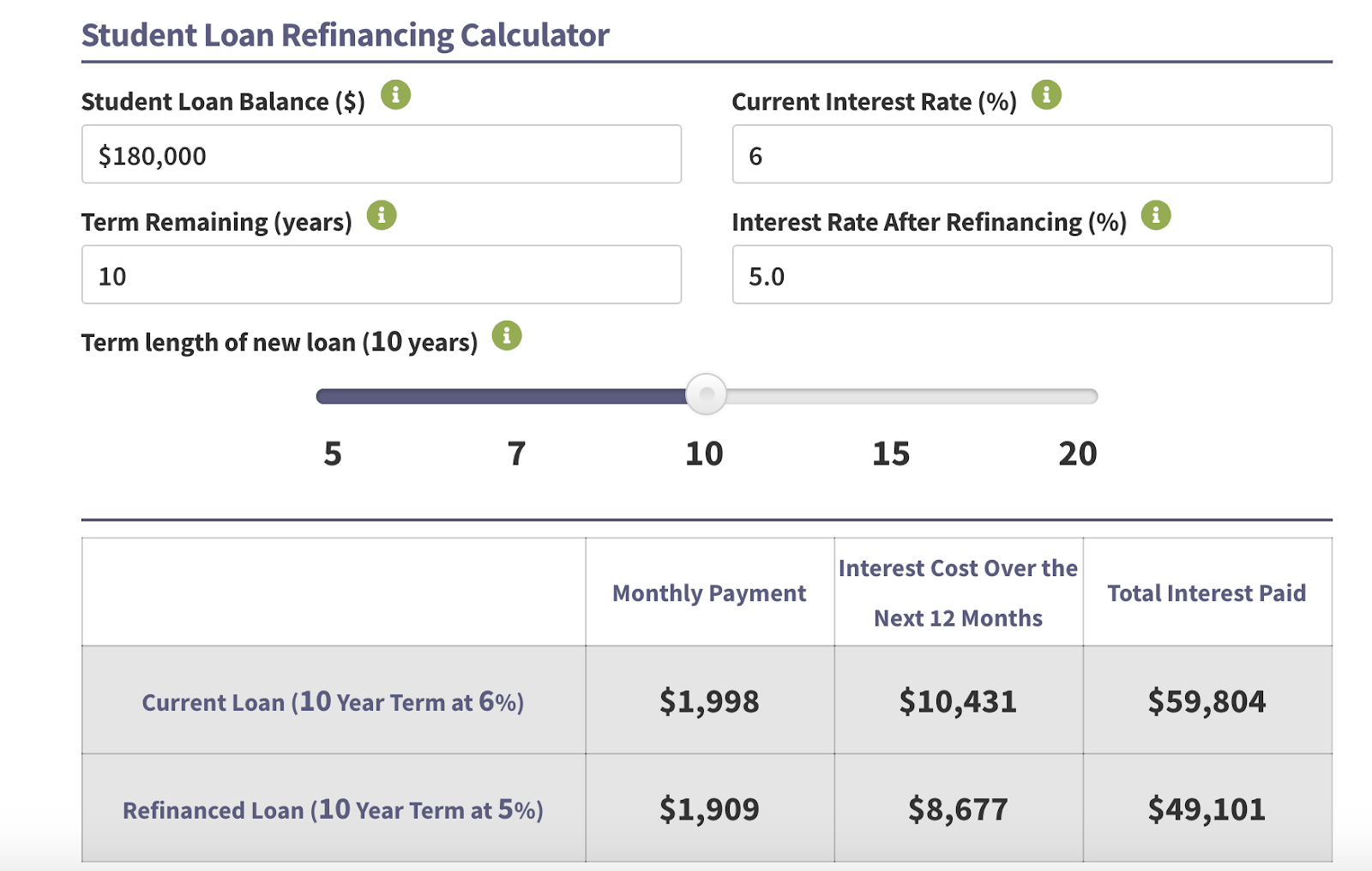

Let’s assume you may have $300,000 in scholar mortgage debt with a 7% rate of interest and 10 years to repay your mortgage. You get accepted for a refinancing mortgage with a lender like CommonBond. You’re provided a 5% rate of interest due to your robust credit score rating of 700, and also you select a 10-year reimbursement time period.

By refinancing alone, your month-to-month fee is lowered by $300. Think about what you might do with that sum of money every month. Paying down your debt quicker is only one possibility. Over the lifetime of your mortgage, you’ll save greater than $36,000.

In our newest refinancing survey, we discovered that 80% of respondents would wish an rate of interest discount of a minimum of 1% to make refinancing price it.

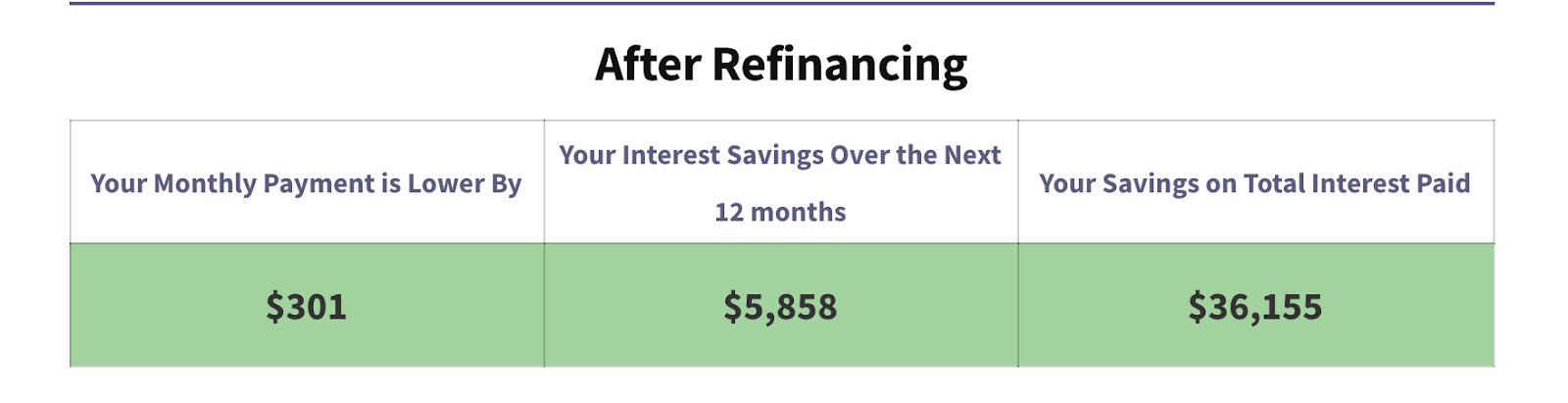

Let’s say you owe $180,000 with an rate of interest of 6% and had 10 years to pay it off. Throughout a refinance, you select a reimbursement time period of 10 years at 5% curiosity. Not solely will your month-to-month fee lower, however you’ll save almost $10,000 general.

We surveyed over 3,200 respondents and plenty of of them owe greater than six figures of scholar mortgage debt (56%), whereas 40% of respondents had a six-figure earnings.

What’s attention-grabbing is that many respondents mentioned they’d be okay with refinancing scholar loans a number of occasions due to money bonuses. At Pupil Mortgage Planner, we provide profitable money again bonuses of as much as $1,000 or extra throughout all of our refinancing companions.

Eighty % of respondents with personal loans mentioned they’d refinance once more for a $1,000 money bonus, however an identical proportion would solely refinance in the event that they scored a minimum of a 1% rate of interest discount.

However right here’s the factor. A discount of simply 0.5% may prevent much more than the bonus, illustrating that many individuals are lured in by short-term bonuses relatively than long-term beneficial properties.

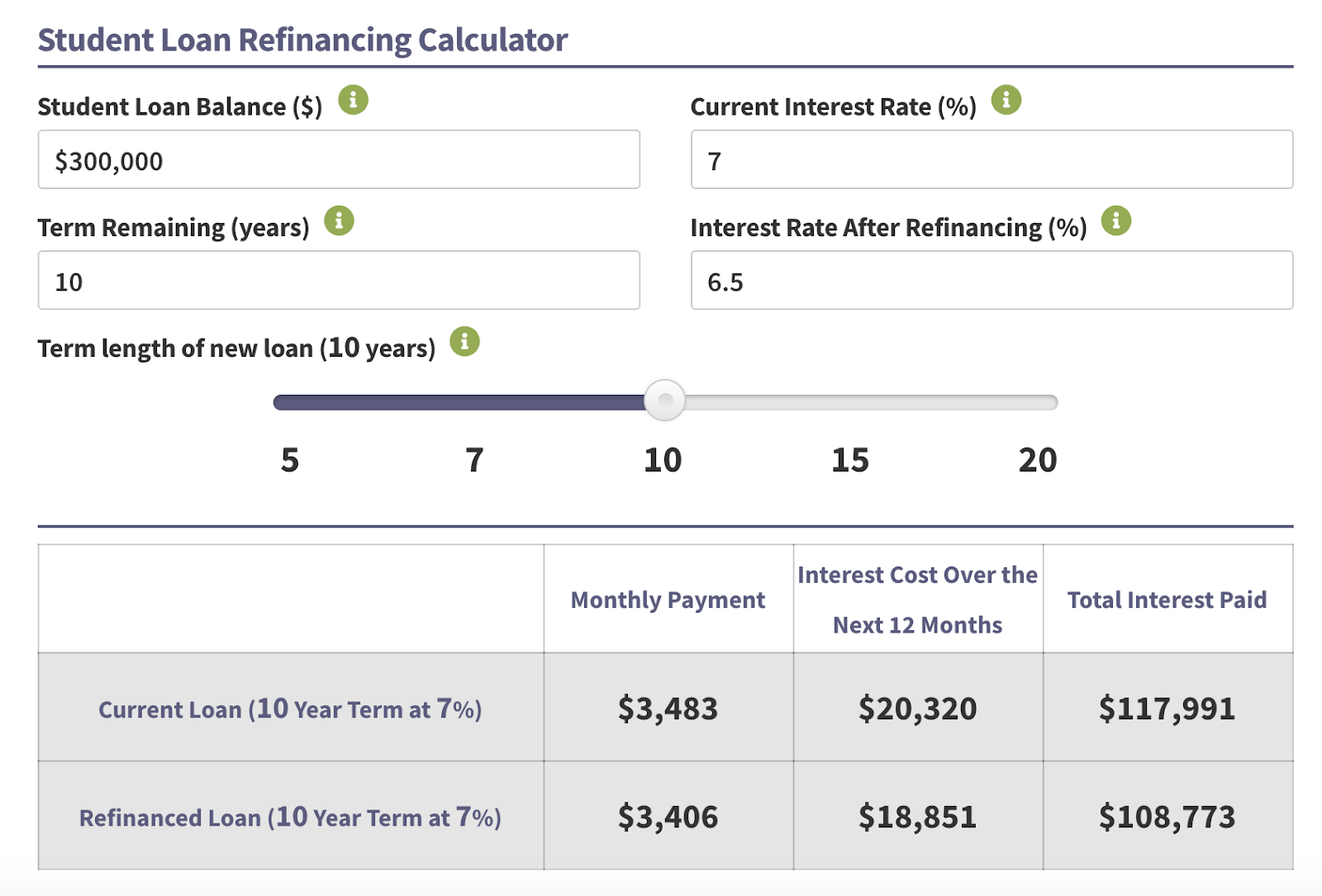

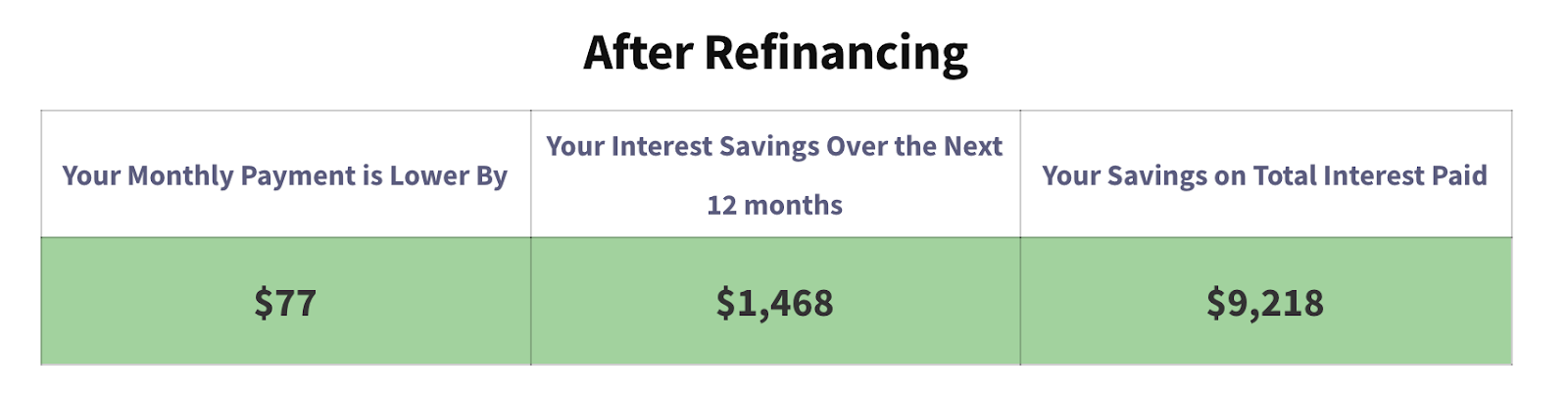

Let’s return to our instance of a high-debt scholar mortgage borrower with $300,000 of debt at a 7% price. Refinancing at a 6.5% price with a 10-year reimbursement time period leads to greater than $1,000 financial savings within the first 12 months alone. Over the lifetime of the mortgage, that’s almost $10,000!

Need to take a look at your personal scholar mortgage refinance financial savings calculations? Take a look at our student loan refinancing calculator your self.

What to know earlier than refinancing scholar loans a number of occasions

Though refinancing scholar loans a number of occasions is feasible, it’s greatest to keep away from refinancing too ceaselessly. You don’t wish to refinance your scholar loans each month, for instance.

However a great refinancing benchmark is each two years or so, with a minimal of 1 12 months. A lot of this has to do together with your credit score. Once you take out a brand new mortgage, your credit score rating takes a small hit as there’s a ‘arduous inquiry’ in your credit score report.

In line with the credit bureau Experian, a tough inquiry will fall off your report in two years and can now not have an effect on your credit score after one 12 months.

You wish to hold tabs in your credit score and ensure it’s the identical or improved by the point you refinance once more. You may overview your credit score report without spending a dime at AnnualCreditReport.com and verify your credit score rating together with your monetary establishment, bank card or a third-party credit score rating platform like Credit score Karma.

It’s vital to know how your reimbursement time period impacts your complete month-to-month fee and the way a lot curiosity you’ll pay over time. The longer the reimbursement time period, the smaller the fee quantity due, however you’ll pay the worth in curiosity long run.

The shorter the reimbursement time period, the upper your month-to-month fee is, however you’ll pay much less in curiosity. Additionally, take a look at every refinancing lender’s particular perks. For instance, SoFi provides options like profession teaching whereas CommonBond has a social promise to assist educate underserved communities.

Is it unhealthy to refinance scholar loans a number of occasions?

Refinancing scholar loans a number of occasions isn’t unhealthy in and of itself. After all, whether or not it’s a good suggestion depends upon your private scenario. In case your credit score is shot otherwise you’re coping with unemployment or underemployment, now won’t be the time to refinance once more.

Additionally, our survey discovered that many individuals are holding off on paying again their loans till the federal payment freeze expires. A complete of 25% of respondents are ready to see if President Biden will cancel scholar loans or provide scholar mortgage forgiveness.

One other 18% of debtors are holding off due to income-driven reimbursement forgiveness and one other 18% is holding off due to Public Service Mortgage Forgiveness (PSLF). At the moment, the federal deferment on scholar mortgage funds nonetheless counts towards mortgage forgiveness, so this method is smart.

Should you’re contemplating refinancing for the primary time and have federal scholar loans, it’s smart to attend till the coed mortgage fee pause is over to reassess your scholar mortgage scenario. Pupil mortgage refinancing isn’t a good suggestion if you wish to pursue mortgage forgiveness or go for income-driven reimbursement.

Information to refinancing scholar loans a number of occasions

Should you’ve already refinanced scholar loans, you seemingly know a bit concerning the course of. However right here’s a great guidelines of what to do when refinancing scholar loans a number of occasions.

- Examine your debt-to-income ratio (DTI). Every lender has its personal earnings necessities. An vital quantity to know is your debt-to-income ratio which ought to be lower than 50%. To calculate your DTI, add your complete month-to-month funds and divide it by your month-to-month earnings. For instance, in case your earnings is $5,000 per 30 days and your complete debt funds equal $2,000, your DTI is 40%.

- Assessment your credit score rating. Once more, every refinancing lender has totally different credit score necessities however a great benchmark is 650 or above.

- Have a look at charges and money again bonuses. To get the very best deal, review multiple student loan refinancing lenders to match charges and cash-back bonuses.

- Collect your private and mortgage data. Have your pay stubs, tax returns, handle, and Social Safety quantity helpful when making use of for one more refinancing mortgage. Assessment how a lot scholar mortgage debt you may have, so you know the way a lot you must borrow for a refinance.

- Get quotes from a number of lenders. Our survey discovered {that a} third of respondents utilized with one refinancing lender. Be sure to request quotes from a number of refinancing lenders to make sure you’re getting the very best charges and phrases.

SoFi, Laurel Road and Earnest make up roughly 50% of the refinancing market. Should you’re on the lookout for a place to begin, these are good choices to take a look at.

Backside line

Now, you may cease questioning how typically you can refinance scholar loans. There’s no restriction.

Refinancing scholar loans a number of occasions could be a good monetary technique when finished proper, particularly with the refinancing ladder method we talked about above. However in fact, all of it depends upon your private monetary scenario.

Do you may have any questions or issues about refinancing (once more)? Get in touch for a student debt consult.

Refinance scholar loans, get a bonus in 2021

$1,000 BONUS1For 100k or extra. $200 for 50k to $99,999¹

$1,250 BONUS2For 250k+, tiered 300 to 500 bonus for 50k to 250k.2

$1,275 BONUS3For 150k+. Tiered 300 to 575 bonus for 50k to 149k.3

$1,000 BONUS4For $100k or extra. $200 for $50k to $99,9994

$1,050 BONUS5For 100k+. $300 bonus for 50k to 99k.5

$1,250 BONUS6For 100k+ or $350 for 5k to 100k.6

$1,250 BONUS7For 150k+. Tiered 100 to 400 bonus for 25k to 149k.7

Undecided what to do together with your scholar loans?

Take our 11 query quiz to get a personalised suggestion of whether or not it is best to pursue PSLF, IDR forgiveness, or refinancing (together with the one lender we expect may provide the greatest price).

1Earnest: $1,000 for $100K or extra, $200 for $50K to $99.999.99. For Earnest, for those who refinance $100,000 or extra by way of this website, $500 of the $1,000 money bonus is supplied instantly by Pupil Mortgage Planner. Charge vary above contains elective 0.25% Auto Pay low costEarnest disclosures. 2Laurel Highway: Should you refinance greater than $250,000 by way of our hyperlink and Pupil Mortgage Planner receives credit score, a $500 money bonus shall be supplied instantly by Pupil Mortgage Planner. In case you are a member of knowledgeable affiliation, Laurel Highway would possibly give you the selection of an rate of interest low cost or the $300, $500, or $750 money bonus talked about above. Provides from Laurel Highway can’t be mixed. Charge vary above contains elective 0.25% Auto Pay low cost. Laurel Road disclosures.3Elfi: Should you refinance over $150,000 by way of this website, $500 of the money bonus listed above is supplied instantly by Pupil Mortgage Planner. Elfi disclosure. 4Sofi: Should you refinance $100,000 or extra by way of this website, $500 of the $1,000 money bonus is supplied instantly by Pupil Mortgage Planner. Charge vary above contains elective 0.25% Auto Pay low cost. Sofi disclosures.5Commonbond: Should you refinance over $100,000 by way of this website, $500 of the money bonus listed above is supplied instantly by Pupil Mortgage Planner. Commonbond disclosure. 6Credible: Should you refinance over $100,000 by way of this website, $500 of the money bonus listed above is supplied instantly by Pupil Mortgage Planner. Credible disclosure.

7LendKey: Should you refinance over $150,000 by way of this website, $500 of the money bonus listed above is supplied instantly by Pupil Mortgage Planner. Charge vary above contains elective 0.25% Auto Pay low cost.

[ad_2]

Source link

{kind=link}