[ad_1]

Whereas refinance purposes appear to be slowing, there are nonetheless some good reasons to refinance your mortgage, even when rates of interest aren’t presently at their greatest.

First off, let me preface this with the truth that mortgage charges are spectacular. Sure, the 30-year mounted was once within the mid-2% vary, however a fee of round 3% was comparatively exceptional till just lately (and remains to be accessible at present).

Sadly, the latest improve in charges has dented refinance purposes because the pool of eligible debtors (those that stand to profit) begins to dry up.

Final week, the Mortgage Bankers Affiliation (MBA) famous that refis slid one other 4%, pushing the refi share of complete mortgage exercise down to only under 62%.

Most trade contributors noticed this coming, which explains the latest pattern of mortgage firms cozying up with actual property brokers. However there are nonetheless alternatives for householders and mortgage lenders to select up the refi slack.

Refinancing Out of the FHA and Into Standard

- Mortgage insurance coverage should be paid for all times on most FHA loans (until you set 10% down)

- That is the case no matter how a lot you’ve paid down your mortgage

- Usually the one option to drop MI utterly is to refinance out of the FHA mortgage program totally

- Thankfully that is straightforward to do and a typical motive why householders refinance their mortgages

Even when charges are a bit larger than they as soon as have been, one alternative which will stay is refinancing an FHA mortgage into a traditional mortgage (akin to one backed by Fannie Mae or Freddie Mac).

The principle advantage of doing that is to take away the obligatory mortgage insurance coverage that should be paid on FHA loans.

Thanks (or not thanks) to the FHA’s stringent mortgage insurance coverage guidelines, the annual mortgage insurance coverage premium (MIP) should be paid month-to-month no matter whether or not the mortgage steadiness falls under 80% loan-to-value (LTV).

The one exception is that if the mortgage initially got here with a ten%+ down fee (or 10%+ fairness), or if it’s an older FHA mortgage that’s exempt from the newer guidelines.

In actuality, most FHA loans are 30-year mounted mortgages with minimal down funds, that means MIP typically stays in-force for all 30 years until you refinance out of the FHA.

This provides to an in any other case low month-to-month mortgage fee, making even an amazing mortgage fee rather less engaging.

Many people took out FHA loans a number of years in the past to make the most of the low 3.5% down payment requirement, coupled with the low FICO rating requirement.

As a result of residence costs have elevated a lot since then, a few of these debtors might have the required fairness to refinance into a traditional mortgage at 80% LTV or much less.

Doing so will enable them to ditch the MIP and keep away from PMI on the brand new typical mortgage, which may equate to substantial financial savings.

Let’s check out an instance of the potential financial savings:

Unique gross sales value: $300,000

Down fee: $10,500 (3.5%)

Mortgage quantity: $294,566 (contains upfront MIP of $5,066.25)

FHA month-to-month MIP: $205.06

Whole month-to-month fee: $1,407.60

Right this moment’s residence worth: $350,000

New refinance fee: $1,178.03 (based mostly on $275,000 mortgage quantity)

As an alternative of subjecting your self to ~$200 in month-to-month mortgage insurance coverage premiums, you may be capable to refinance to a conventional loan at 80% LTV or much less and rid your self of that burden.

This could possibly be the case no matter how a lot you’ve paid down your mortgage because it closed. Why? Surging residence costs, which might decrease your LTV considerably.

So even when you solely put down a paltry 3.5% a couple of years in the past, you may need the required 20% in fairness to lose the mortgage insurance coverage as soon as and for all.

Tip: Observe that the Upfront Mortgage Insurance coverage Premium (UFMIP) is non-refundable when you refinance out of the FHA to a traditional mortgage. It might be refundable when you refinance to a brand new FHA-insured mortgage.

Two Issues Have to Occur for the FHA-to-Standard Refinance to Make Sense

- You’ll want 20% fairness for this sort of refinance to make sense

- That’s the minimal to keep away from PMI (80% LTV or decrease) on a traditional mortgage

- And also you’ll desire a decrease or comparable mortgage fee as effectively

- This ensures your month-to-month fee drops sufficient to justify any closing prices concerned

Not simply anybody can make the most of this sort of refinance. Solely those that have gained sufficient fairness and who can get hold of a comparable (or higher) mortgage fee will win right here.

Utilizing our instance from above, the house should now be value X quantity to get that LTV all the way down to the place it must be. I say X as a result of it relies upon how lengthy you’ve had the mortgage.

A mix of residence value appreciation and the pure amortization of the mortgage will let you know what the worth must be.

Our hypothetical mortgage steadiness would drop to round $275,000 in simply three years by common month-to-month funds, requiring a home worth of about $344,000 to get the job achieved.

Thankfully, residence costs have skyrocketed prior to now a number of years, so for a lot of fortunate debtors the appreciation alone can push a comparatively younger mortgage to the magical 80% LTV mark upon refinancing.

Assuming you’re good to go there, you’ll want to think about the mortgage rate. That’s, your former mortgage fee and the refinance mortgage fee.

In case you beforehand had a fee of two.75% on a 30-year mounted, and the most effective accessible fee at present is 3.125%, it’s important to consider that .375% bump in fee.

The excellent news is that it shouldn’t have an effect on the mortgage fee by an excessive amount of.

The previous principal and mortgage fee was $1,202.54 plus $205.06 with MIP, making it $1,407.60 out the door (don’t overlook taxes and insurance coverage too!).

If the speed have been 3.125% as an alternative, the month-to-month P&I fee can be (based mostly on a barely decrease excellent steadiness of $275,000) $1,178.03.

Positive, it’s solely about $25 lower than the previous P&I fee, however you now not must pay the $200 in MIP. Collectively, that’s a major quantity of month-to-month financial savings.

In actuality, you may truly do even higher when you began out with the next mortgage fee because of a low credit score rating and/or excessive LTV, and have since improved upon these issues.

Usually, residence consumers flip to the FHA as a result of they’ve imperfect credit score, so assuming your credit score scores rise, you may save much more.

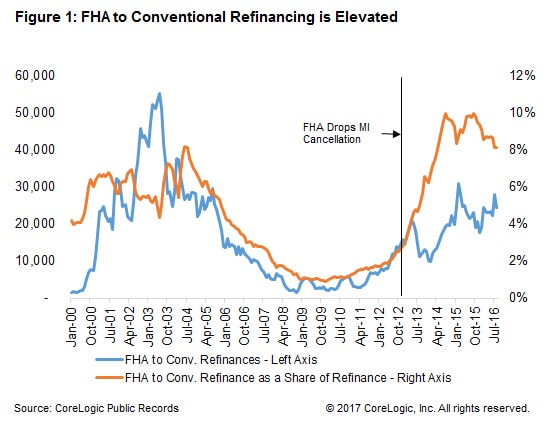

FHA-to-Standard Refinances Took Off When Mortgage Insurance coverage Grew to become Everlasting

- When the FHA dropped MI cancellation a lot of householders started making the change

- Because of wholesome residence value appreciation and continued low mortgage charges it’s a simple transfer to make

- It might be doable to drop the pesky annual MIP and rating a decrease rate of interest on the similar time

- Test your present LTV based mostly in your property’s present appraised worth to see when you can profit too!

When the FHA modified its coverage in 2013 to require mortgage insurance for life, FHA-to-conventional refinances soared.

In 2010, there have been solely about 4,000 FHA-to-conventional refis per 30 days, or only one % of complete refinance transactions at the moment.

In case you take a look at the chart above, you’ll discover FHA to standard refinance quantity jumped, as did its share of complete refinance quantity.

Since 2013, hundreds of thousands of debtors have taken out FHA loans, regardless of this unfavorable rule. Because of constantly rising residence costs, lots of of 1000’s of those debtors have gone typical every year.

Those that are presently in an FHA mortgage may wish to take into account a traditional mortgage as an alternative because the month-to-month (and mortgage time period) financial savings could possibly be appreciable.

Simply make sure to be aware of how lengthy your FHA mortgage insurance coverage will truly be in-force, and what the brand new rate of interest might be.

Some debtors with older FHA loans, 15-year mounted mortgages, or those that initially made massive down funds may need extra favorable insurance coverage necessities.

When inquiring a few refinance, additionally look into totally different mortgage phrases like a 15-year fixed if you wish to keep on monitor payoff-wise.

Lastly, there’s an opportunity the FHA might revisit its mortgage insurance coverage for all times coverage now that their coffers are much more full. However that gained’t apply to loans that already funded.

Learn extra: FHA vs. conventional loan

(picture: Phil Leitch)

[ad_2]

Source link

{kind=link}