[ad_1]

Posted on June twenty first, 2021

Assuming you want to become a homeowner, it’s in all probability finest to go to school, even when it’s a must to take out expensive scholar loans within the course of.

You will have learn articles over the previous a number of years that discuss snowballing scholar mortgage debt and the shortcoming to afford a mortgage because of this.

Whereas this may be true in some circumstances, it seems you’re nonetheless extra seemingly to purchase a house should you receive not less than a bachelor’s diploma.

The Advantages Outweigh the Prices

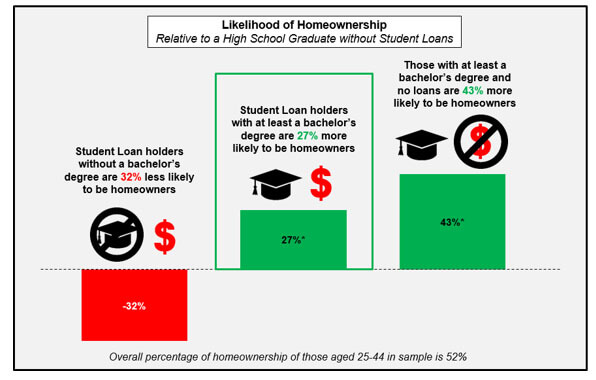

A commentary (since eliminated) from mortgage financier Fannie Mae revealed that those that go to school usually tend to change into owners than those that merely graduate from highschool.

Probably the most possible owners are these with a university training and no scholar loans, with a chance of homeownership that’s 43% greater than highschool graduates with out scholar loans.

In the meantime, scholar mortgage holders with bachelor’s levels are nonetheless 27% extra prone to change into owners relative to these debt-free highschool graduates.

There’s a catch although – should you don’t really full your bachelor’s diploma and easily wind up with scholar loans, you’re really worse off than those that merely known as it quits after highschool.

This final group is 32% much less prone to personal a house than a debt-free highschool graduate. They’re additionally extra prone to be behind on scholar mortgage funds, which isn’t very shocking.

The takeaway right here is that it pays to go to school, even when it prices and arm and a leg.

The concept being that faculty grads receives a commission extra and are ultimately able to qualify for mortgages to buy properties.

Don’t Be Discouraged If You Have Pupil Loans and Want a Mortgage

As famous, scholar mortgage debt has elevated considerably in recent times and its results could not but be evident within the homeownership numbers.

Moreover, nearly all of these surveyed by Fannie Mae had scholar mortgage debt that accounted for 10% or much less of their month-to-month earnings. Others won’t be so fortunate.

If in case you have excellent scholar loans, you may nonetheless get authorized for a mortgage. It simply would possibly have an effect on how much you can afford as a result of it is going to be factored into your DTI ratio.

Many scholar loans are deferred to assist current graduates rise up and working earlier than they’re gainfully employed. Nonetheless, mortgage lenders know these people will ultimately need to repay their loans.

Because of this, lenders should nonetheless account for the coed mortgage reimbursement when qualifying you for a mortgage to make sure your own home mortgage is definitely reasonably priced.

In fact, it will depend on the type of mortgage you apply for.

Fannie Mae Pupil Mortgage Pointers

In relation to Fannie Mae (conforming loans), if the coed mortgage fee quantity is listed on the credit score report, it may be used for qualifying functions. Finish of story.

If the fee isn’t listed on the credit score report, or reveals $0, or is deferred, totally different guidelines apply.

For these in an income-driven fee plan, and documentation reveals the precise month-to-month fee is zero, the lender could qualify the borrower with a $0 fee.

For scholar loans which can be deferred or in forbearance, a fee equal to 1% of the excellent steadiness can be utilized to find out the month-to-month fee.

So if there’s a $25,000 scholar mortgage, $250 is added to your month-to-month liabilities to calculate your DTI, even when it’s decrease than the precise fully-amortizing fee.

Lenders are additionally in a position to calculate a fee that can totally amortize the mortgage based mostly on the documented mortgage reimbursement phrases, which can end in a decrease month-to-month legal responsibility.

Whereas this may occasionally appear harsh, it was once 2%, or $500 in our instance above.

However Fannie decided that precise month-to-month funds had been usually lower than 2% of the overall steadiness.

The outdated coverage additionally required lenders to make use of the better of the particular month-to-month fee or 1% of the steadiness, except the payment was fully-amortized and never topic to any future changes. However this made no sense both.

Freddie Mac Pupil Mortgage Guidelines

If the coed mortgage(s) is in reimbursement, deferment, or forbearance, Freddie Mac breaks it down into two choices.

For loans with a month-to-month fee better than zero, the precise fee quantity discovered on the credit score report or different file documentation can be utilized.

If the month-to-month fee quantity reported on the credit score report is $0, the lender should use 0.5% of the excellent mortgage steadiness because the fee for qualifying functions.

So utilizing our similar instance from above, a $125 fee could be factored into your DTI to find out should you qualify.

This might make it simpler to qualify for a Freddie Mac-backed mortgage versus a Fannie Mae mortgage.

Moreover, it may be doable to exclude the coed mortgage fee out of your DTI ratio if there are 10 or much less month-to-month funds remaining.

FHA Pupil Mortgage Pointers

HUD simply introduced new modifications on June 18th, 2021 which will make it simpler to qualify for an FHA loan when you have scholar mortgage debt.

No matter fee standing, when the fee is above $0 the lender should use the fee quantity reported on the credit score report or the precise documented fee.

If the fee quantity listed is zero, 0.5% of the excellent mortgage steadiness is used to calculate the fee, much like Freddie Mac.

So once more, it’d be a fee of $125 utilizing our instance of $25,000 in debt.

Previous to this modification, the FHA used 1% of the steadiness, so the $25,000 mortgage would have resulted in a $250 per thirty days legal responsibility on your DTI ratio.

Clearly this may have an enormous impact on what you may afford. And apparently greater than 80% of FHA-insured mortgages are for first-time home buyers.

Moreover, the FHA estimates that almost half (45%) of those debtors have scholar mortgage debt, with individuals of shade essentially the most impacted.

This explains the easing of the rule, and pales compared to the outdated requirement of two% of the excellent steadiness if no fee was discovered!

VA Pupil Mortgage Guidelines

In relation to VA loans, scholar mortgage funds might be ignored if funds gained’t start for greater than 12 months from mortgage closing.

This could be a enormous benefit in case your liabilities would push you over the allowable max DTI ratio.

But when scholar mortgage reimbursement has began or is scheduled to start inside 12 months from the date of the VA mortgage closing, the lender should depend the precise or anticipated month-to-month fee.

They use a formulation that calculates every mortgage at a price of 5 % of the excellent steadiness divided by 12 (months).

So utilizing our $25,000 instance, it’d be $104.17. Nonetheless, if a better fee quantity is listed on the credit score report, akin to $150, it have to be used.

If the fee listed on the credit score report is decrease than the brink fee calculation above, an announcement from the coed mortgage servicer that displays the precise fee could also be permitted.

USDA Pupil Mortgage Pointers

For USDA loans, the precise scholar mortgage fee can be utilized if it’s fastened (and has a hard and fast time period) with out future fee changes.

If no fee is reported or it’s deferred, 0.5% of the mortgage steadiness is used except there’s proof that it’s a hard and fast fee.

Utilizing our $25,000 instance, it’d be $125, much like the opposite mortgage sorts listed above.

In the event you’re near maxing out with regard to DTI, an experienced mortgage broker or lender would possibly have the ability to get you authorized utilizing a mortgage that has a extra forgiving coverage with regard to scholar mortgage debt.

Don’t surrender till you contemplate a number of eventualities and exhaust all of your choices.

But additionally be sure you consider any scholar mortgage debt early on within the mortgage discovery course of so that you don’t overlook this key qualification side.

A very good rule of thumb may be to calculate your DTI utilizing 1% of your scholar mortgage steadiness for the month-to-month fee, even when it seems you should utilize a decrease documented fee. This fashion you’ll nonetheless qualify within the worst-case situation.

Additionally be careful for lender overlays that decision for greater minimal month-to-month funds than the rules really require.

[ad_2]

Source link

{kind=link}