[ad_1]

Our aim is to provide the instruments and confidence that you must enhance your funds. Though we obtain compensation from our companion lenders, whom we are going to all the time establish, all opinions are our personal. Credible Operations, Inc. NMLS # 1681276, is referred to right here as “Credible.”

Should you’re wanting to economize on a house mortgage, you is likely to be intrigued by the low preliminary charges on an adjustable-rate mortgage (ARM). However whereas charges on ARMs begin low, they will additionally rise over the lifetime of the mortgage.

Rate of interest caps shield you in opposition to a runaway charge improve, and it’s necessary to grasp how they work should you’re looking for adjustable-rate mortgages.

Right here’s what that you must find out about rate of interest caps:

What’s an rate of interest cap?

An rate of interest cap limits how a lot your rate of interest can rise on an adjustable-rate mortgage. With an ARM, the rate of interest begins at a low, fastened charge after which goes up or down periodically.

And when the speed adjustments, your month-to-month mortgage fee adjustments, too. Rate of interest caps can shield debtors from the shock of a bigger mortgage fee as a result of they hold charges from growing above a sure restrict.

Should you’re in search of an awesome mortgage charge, Credible’s streamlined course of will help. We make evaluating a number of mortgage lenders simple. In only a few minutes, you’ll be able to see prequalified charges from our companion lenders — it’s easy and it gained’t have an effect on your credit score rating.

Discover Charges Now

How ARM rate of interest caps are structured

An adjustable-rate mortgage often has some sort of cap construction, which exhibits how a lot the rate of interest can improve at totally different factors within the house mortgage time period.

Adjustable-rate mortgage caps are set by the lender. They’re sometimes offered in a sequence of three numbers — resembling 2/2/5 — that signify every cap: preliminary cap, periodic cap, and lifelong cap.

Right here’s how these caps work:

Preliminary adjustment cap

The preliminary adjustment cap limits how a lot the mortgage charge can rise the primary time it adjustments after the fixed-rate interval expires.

Your lender units this curiosity cap, however the Client Monetary Safety Bureau says it often falls between 2% and 5%.

For instance, say you get a 5/1 ARM with an preliminary fastened charge of three.5% and a cap construction of two/2/5. Your rate of interest may rise as much as 5.5% within the sixth 12 months of the mortgage time period.

Subsequent adjustment cap

The following adjustment cap limits how a lot the mortgage charge can rise in every adjustment interval after the primary one.

This cover is mostly set at 2%, although it varies by lender and mortgage. Check out your 5/1 ARM with the two/2/5 cap construction. Your charge elevated to five.5% within the sixth 12 months, and within the seventh 12 months, it might improve to no larger than 7.5%.

See Extra: 30 Mortgage Phrases to Know: Final Glossary for Homebuyers

Lifetime adjustment cap

The lifetime adjustment cap limits how a lot your mortgage charge can improve total all through the lifetime of the mortgage.

The lifetime cap is mostly 5%, although some lenders set a better cap. Within the instance of a 5/1 ARM that begins at 3.5% and has a cap construction of two/2/5, the rate of interest can by no means go larger than 8.5%.

Learn how to examine charge caps when selecting an ARM

Whenever you’re looking for an adjustable-rate mortgage, two lenders could provide the identical preliminary rate of interest however totally different charge caps. One could find yourself being costlier, so it’s necessary to go over the curiosity cap and determine how excessive the rate of interest could improve.

Tip: Ask the lender to calculate the best fee you’d must make on the mortgage, and determine in case your finances can soak up that elevated fee.

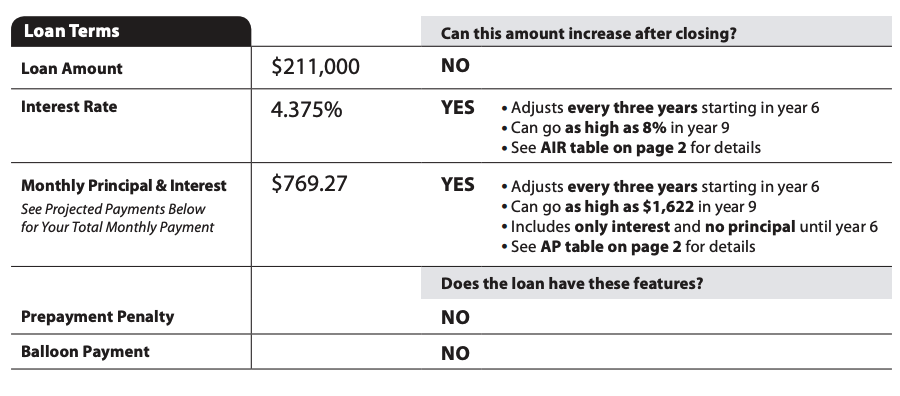

You can too examine your mortgage estimate, a doc the lender offers inside three enterprise days after you apply for a mortgage mortgage. Take a look at web page 1 below “Mortgage Phrases.”

Subsequent to the rate of interest, the doc will say whether or not the speed can improve after closing. It should additionally inform you how lengthy the speed is fastened, how usually the speed can improve, and the way excessive it might stretch.

Is an ARM best for you?

When selecting a mortgage, you’ll must determine between an adjustable and a hard and fast charge. Usually, adjustable-rate mortgages profit homebuyers who plan to promote their home or refinance the mortgage earlier than the fixed-rate interval ends.

Tip: An ARM might also make sense should you will pay extra towards the principal in the course of the fixed-rate interval.

A hard and fast charge, then again, would possibly profit somebody who’s planning to remain within the house long run and prefers a predictable month-to-month mortgage fee. In case your finances is already tight, then you definitely won’t have the ability to climate a charge improve.

Listed below are the professionals and cons of an ARM you must take into account:

| Professionals | Cons |

|---|---|

| Smaller month-to-month mortgage funds at first | Your month-to-month mortgage fee could rise |

| Decrease curiosity expense initially | Bigger curiosity expense in the long run |

| Charges can go down, which interprets to decrease month-to-month mortgage funds. | ARMs are usually extra difficult |

| It’s possible you’ll pay down the mortgage principal quicker | Funds may turn out to be unaffordable |

When selecting between an ARM vs. a fixed-rate mortgage, ask your self these questions:

- What’s occurring with mortgage charges? Rates of interest are all the time altering, however you’ll be able to observe their normal trajectory over time. An adjustable-rate mortgage may make sense if mortgage charges have been rising. That’s as a result of the distinction between adjustable and glued charges is extra pronounced, so that you would possibly discover an awesome deal on an ARM.

- Can I make additional funds in the course of the fixed-rate interval? When you will have a mortgage with a low rate of interest, extra of your month-to-month fee goes towards paying down the principal. If you can also make additional funds whereas your charge is low, then you would repay extra of your debt and save more cash on curiosity in the long term.

- How lengthy do I plan to dwell within the house? An ARM could possibly be possibility should you’re planning to maneuver earlier than the fastened charge interval ends. As an illustration, individuals who ceaselessly relocate for work would possibly profit from an adjustable-rate mortgage. However there’s some threat concerned right here since you won’t have the ability to promote the house once you plan to.

Be taught extra about ARMs:

In regards to the creator

[ad_2]

Source link

{kind=link}