[ad_1]

Are you at the moment being pursued by locum tenens recruiters and are questioning how taking an project would have an effect on your pupil mortgage compensation? We frequently obtain locum tenens pupil loans questions from new physicians in addition to CRNAs, PAs, or NPs. Listed below are the principle challenges I see when you’ve acquired a locum tenens way of life with loads of pupil debt:

- Incapability to entry Public Service Mortgage Forgiveness (PSLF)

- Problem verifying your revenue

- Uncertainty surrounding your long-term employment

- Probably tougher time refinancing

Fortunately these challenges might be simply handled by a sensible pupil mortgage plan. We specialise in serving to of us working in a locum tenens doctor function figure out their pupil mortgage debt, significantly if that debt is between $100,000 and $1 million.

Paying again medical faculty debt as a locum tenens physician presents alternatives that others don’t have. Right here’s a few of these:

- Lowering Adjusted Gross Revenue (AGI) extra simply than employed friends (good for 20-25 12 months mortgage forgiveness)

- Offering your personal advantages

- Revenue and site flexibility

We’ll start by addressing the challenges that locum tenens practitioners face earlier than displaying the alternatives which might be out there.

You may’t get PSLF with locum tenens

The most important disadvantage I see to working a locum tenens job is just like that confronted by personal apply physicians. You may’t make the most of the Public Service Mortgage Forgiveness program whereas engaged in a locum place. The explanation?

The definition of locum tenens is from a Latin time period that means “holding a spot.” Which means you’re a 1099 impartial contractor in a locum function. Solely full-time staff can make the most of the forgiveness supplied below the PSLF program.

Therefore, locum healthcare suppliers should pay again their medical faculty loans both by IDR mortgage forgiveness over 20-25 years or by utilizing an aggressive payback technique like refinancing.

How you can get mortgage forgiveness with a locum job

Although your locum tenens assignments don’t rely in direction of PSLF, you would possibly ultimately get a full-time job at a qualifying not-for-profit employer.

It will be a giant mistake to instantly refinance your federal loans or pay them again aggressively until you’re certain that this received’t be a chance for you.

I’ve seen loads of tales of physicians who do some locum work throughout residency, fellowship or early of their attending careers solely to modify to everlasting roles a few years later.

Needless to say qualifying PSLF month-to-month funds wouldn’t have to be consecutive. Which means you would make funds on the REPAYE or PAYE plan whereas doing locum tenens and when you change to an eligible job, you would possibly ultimately get PSLF.

Additionally, when you’re a fellow or doing a small quantity of locum work on the facet, you possibly can nonetheless qualify for PSLF in case your major job is full time at a 501c3 or authorities employer. In different phrases, a small quantity of locum tenens work doesn’t derail you.

Verifying your revenue with mortgage servicers is a ache with locum tenens

Do that you must embody your entire 1099 revenue as a locum tenens physician when making use of for income-driven compensation packages? The reply is sure in keeping with the definition the federal government makes use of of taxable revenue. In the event you have a look at the IDR verification type that you just’re required to submit yearly, right here’s what the federal government needs to know:

“You have to present documentation of all taxable revenue you and your partner (if relevant) at the moment obtain. Taxable revenue consists of, for instance, revenue from employment, unemployment revenue, dividend revenue, curiosity revenue, suggestions, and alimony.”

Clearly, revenue as an impartial contractor constitutes revenue from employment. Nonetheless, that revenue varies so much relying in your present employment association. For that cause, I recommend checking the field that claims “My revenue has not considerably modified” until you’re feeling a robust must say in any other case.

Utilizing your tax return to certify income-based funds as a locum tenens employee

Once you say that your revenue hasn’t considerably modified, you’ll be requested to offer your tax return to the mortgage servicer. They’ll then use your Adjusted Gross Revenue (AGI) to determine what your mortgage cost needs to be.

In the event you referred to as your mortgage servicer with updates each time your revenue modified whereas doing locum tenens, you’d be spending an enormous period of time doing so. Therefore, I view submitting tax returns solely as the perfect technique of certifying funds.

The non permanent nature of locum jobs could make planning tough

In the event you’re not working ready for the long run, you may need a tough time planning your future.

The explanation this issues when you’ve got pupil loans and settle for a locum tenens alternative is that you could be or might not be employed full time by a not for revenue or authorities hospital sooner or later.

For instance, say you do locum tenens for 2 years. There’s a stable probability your full-time place whenever you depart may very well be at a not for revenue establishment. If that’s the case, you’d nonetheless be eligible for PSLF when you accomplished 10 years of service. Your whole compensation size, in that case, could be 12 years when you did 2 years of locums and 10 years of full-time service.

In the event you attempt to make a full plan earlier than you already know what your future will appear to be, you would possibly make the improper selections.

Generally, by no means refinance your pupil loans from med faculty till you’re certain a 501c3 or VA job just isn’t in your future.

How you can refinance in a locum tenens function

Most of the pupil mortgage refinancing companies I work with have a neater underwriting course of for W-2 staff. Worker incomes are typically extra steady than impartial contractors, in order that is smart. However it’s positively potential to qualify for refinancing as a locum tenens doc.

I reached out to Commonbond for this text (SLP readers get a money bonus by that referral hyperlink) on what documentation they would want from a borrower in a locum tenens job. Right here’s what they mentioned:

“Refinancing with a locum tenens employment scenario would depend upon the diploma kind that the borrower has. If the borrower obtained their MD, DO, DMD, or DDS then Commonbond ought to solely require a one-year historical past of revenue paperwork (1099 or a full tax return). Equally, if the borrower has a kind of diploma varieties and operates as an LLC, then we’d require a 1-year historical past of enterprise tax returns for them. Nonetheless, If they’ve a unique diploma kind, we are going to usually require a 2-year historical past of revenue paperwork.”

In the event you’re a dentist or a doctor, you’ll have the ability to qualify extra simply for pupil mortgage refinancing. Needing solely a single 12 months of tax returns is a fairly low bar to clear.

Additionally, remember that when you consolidate your loans instantly after commencement, you would get a $0 cost on REPAYE with an enormous curiosity subsidy the primary 12 months. Therefore, despite the fact that refinancing isn’t a cake stroll with a 1099 locum employment scenario, it may be performed.

Other people like PAs, NPs, and CRNAs can still refinance with locum tenens revenue historical past, but it surely feels like corporations would are inclined to want two years of tax returns.

Pupil mortgage forgiveness choices for locum tenens

Although locum jobs don’t qualify for PSLF, you possibly can nonetheless get pupil mortgage forgiveness whereas working locum tenens positions. You merely must have a excessive sufficient debt-to-income ratio to make the mathematics make sense.

For instance, 1099 contractors can begin a solo 401k and contribute as much as $58,000 pre-tax in 2021. Right here’s how this might work.

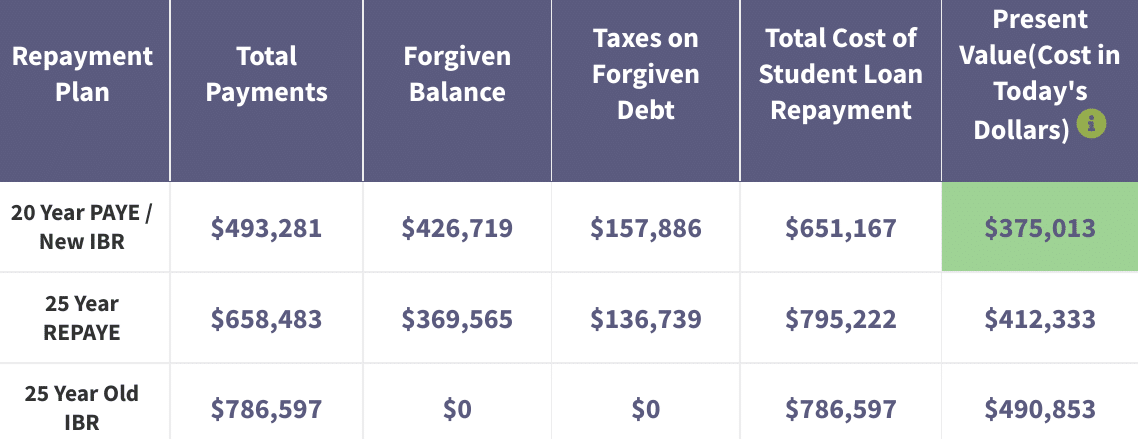

Timmy will do long run locum tenens work and earns $250,000 per 12 months as a 1099 contractor. He has $400,000 in federal pupil loans at a median rate of interest of 6.5% With out making any solo 401k contributions, right here’s how he would pay with the varied IDR plans:

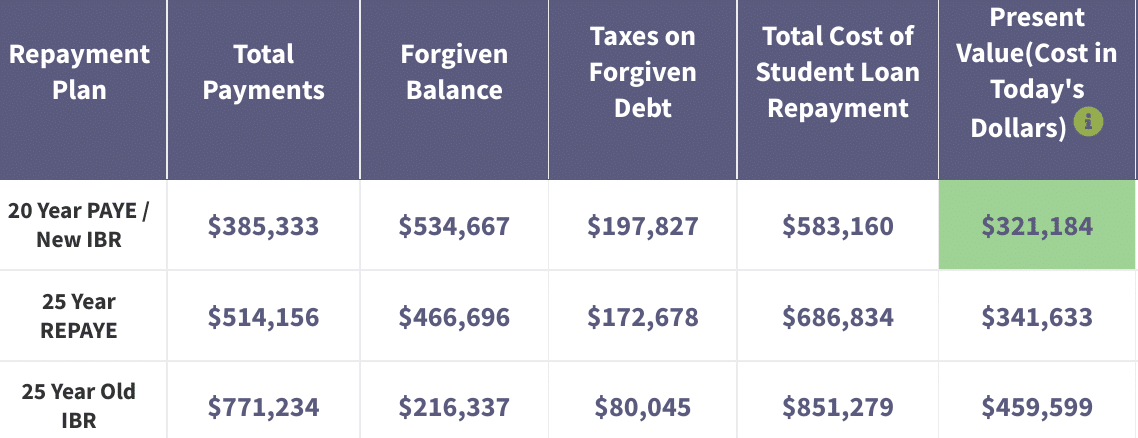

However Timmy decides to work with a CPA who units up an S company with a “locum tenens wage” of $120,000 per 12 months. He makes a contribution of $19,500 as an worker plus 25% of his wages. That lowers his AGI by $49,500.

Now, as a substitute of creating $250,000 for tax functions, he truly makes $200,500. Preserving the identical pupil debt numbers as earlier than, right here’s how the mathematics might look:

Discover how the price of paying the 20 years of funds on the Pay As You Earn plan (PAYE) plus the tax bomb offers a decrease value in right now’s {dollars} of over $50,000. That’s a decrease current worth, which implies you would come out even additional forward when you invested that cash and earned a 5% fee of return.

Most locum tenens pupil loans prep ought to contain working with someone like us and a CPA. The objective could be to determine if decreasing your taxable revenue might provide you with projected forgiveness with right now’s guidelines.

Employers is perhaps prepared to contribute in direction of your loans as nicely in change for particular service size.

Locum tenens advantages: revenue, location, and job flexibility

As a locum tenens physician, you’ll have usually have very low dwelling bills. Most often, your journey bills, housing, and even your malpractice premiums will likely be lined by your company. You may also deduct something your CPA says counts as a enterprise expense.

As well as, you’ve got extra freedom and suppleness. And geography doesn’t need to get in the way in which of you pursuing the roles that provide the very best potential revenue. You may take further shifts to spice up your pay even additional. Or when you’d fairly work much less, you are able to do that too (and depend on income-driven compensation plan forgiveness to make it financially viable).

Perhaps you’re not excited by working for large healthcare services. So you employ locum tenens to go to a bunch of distant places you wouldn’t see in any other case. In truth, locum tenens businesses have been know to supply bonuses to medical professionals who work for an prolonged time frame briefly provide areas.

Get a plan that displays why you’re doing locum tenens work

Most healthcare professionals are going to maneuver on to a everlasting function in some unspecified time in the future. Till them, make certain the way in which you handle your pupil loans displays what you’re considering.

For fast debt payoff, you would possibly take into consideration the Revised Pay As You Earn (REPAYE) plan or refinancing. In the event you’re not sure however would possibly need to do PSLF, preserve your choices open and your debt with the federal authorities.

Do you assume you need to do non permanent roles long-term as a way of life play? If that’s the case, you would possibly need to take into consideration going for taxable forgiveness.

No matter what path you’re taking, have enjoyable and don’t stress about your loans. We might help you navigate what to do if you would like the skilled steering since no person else is considering locum tenens and mortgage methods the way in which we’re.

What are your ideas about locum tenens work? Do you suggest it or is there one thing you would like you had performed in a different way?

Refinance pupil loans, get a bonus in 2021

$1,050 BONUS1For 100k+. $300 bonus for 50k to 99k.1

$1,000 BONUS2 For 100k or extra. $200 for 50k to $99,9992

$1,050 BONUS3For 100k+. $300 bonus for 50k to 99k.3

$1,275 BONUS4 For 150k+. Tiered 300 to 575 bonus for 50k to 149k.4

$1,000 BONUS5For 100k+. $300 bonus for 50k to 99k.5

$1,000 BONUS6For $100k or extra. $200 for $50k to $99,9996

$1,250 BONUS7 For 100k+ or $350 for 5k to 100k.7

$1,250 BONUS8For 150k+. Tiered 100 to 400 bonus for 25k to 149k.8

Undecided what to do along with your pupil loans?

Take our 11 query quiz to get a customized suggestion of whether or not you must pursue PSLF, IDR forgiveness, or refinancing (together with the one lender we predict might provide the finest fee).

All charges listed above symbolize APR vary. 1Commonbond: In the event you refinance over $100,000 by this web site, $500 of the money bonus listed above is supplied instantly by Pupil Mortgage Planner. Commonbond disclosure. 2Earnest: $1,000 for $100K or extra, $200 for $50K to $99.999.99. For Earnest, when you refinance $100,000 or extra by this web site, $500 of the $1,000 money bonus is supplied instantly by Pupil Mortgage Planner. Price vary above consists of optionally available 0.25% Auto Pay low costEarnest disclosures.

3Laurel Highway: In the event you refinance greater than $250,000 by our hyperlink and Pupil Mortgage Planner receives credit score, a $500 money bonus will likely be supplied instantly by Pupil Mortgage Planner. In case you are a member of an expert affiliation, Laurel Highway would possibly give you the selection of an rate of interest low cost or the $300, $500, or $750 money bonus talked about above. Affords from Laurel Highway can’t be mixed. Price vary above consists of optionally available 0.25% Auto Pay low cost. Laurel Road disclosures.

4Elfi: In the event you refinance over $150,000 by this web site, $500 of the money bonus listed above is supplied instantly by Pupil Mortgage Planner. Elfi disclosure. 5Splash: In the event you refinance over $100,000 by this web site, $500 of the money bonus listed above is supplied instantly by Pupil Mortgage Planner. Splash disclosure. 6Sofi: In the event you refinance $100,000 or extra by this web site, $500 of the $1,000 money bonus is supplied instantly by Pupil Mortgage Planner. Price vary above consists of optionally available 0.25% Auto Pay low cost. Sofi disclosures. 7Credible: In the event you refinance over $100,000 by this web site, $500 of the money bonus listed above is supplied instantly by Pupil Mortgage Planner. Credible disclosure.

8LendKey: In the event you refinance over $150,000 by this web site, $500 of the money bonus listed above is supplied instantly by Pupil Mortgage Planner. Price vary above consists of optionally available 0.25% Auto Pay low cost.

[ad_2]

Source link

{kind=link}