[ad_1]

Mortgage charges forecast for Might 2021

Debtors who locked a mortgage in April had been completely satisfied to see charges take a tumble.

However will the pattern proceed in Might?

Doubtless not. Financial restoration is marching ahead, and with it, mortgage charges ought to proceed to rise.

Whereas we might see additional low-rate blips in Might, they’re prone to be brief and unimaginable to foretell.

So long as our financial outlook post-COVID is optimistic, rates of interest ought to go larger.

So, until you’re feeling pessimistic about restoration, now is a good time to lock your fee.

Find and lock a low mortgage rate (Apr 24th, 2021)

On this article (Skip to…)

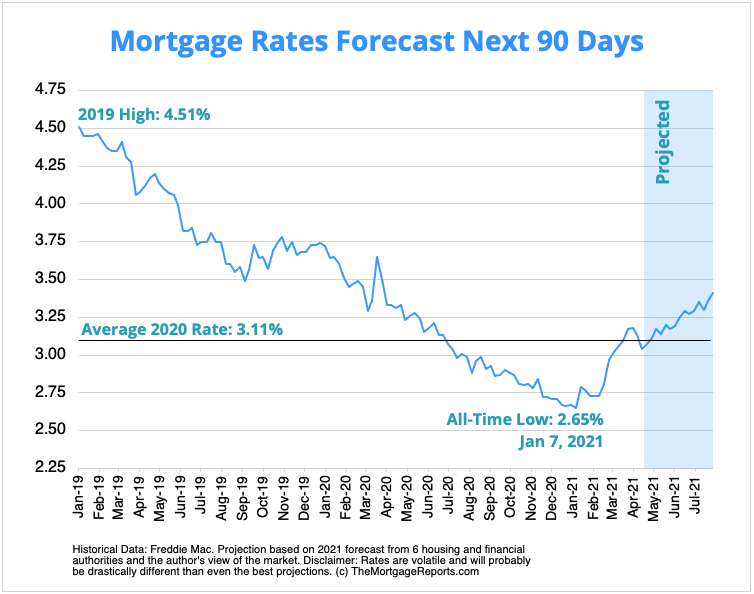

Mortgage charges forecast subsequent 90 days

This chart reveals previous mortgage fee traits, plus predictions for the subsequent 90 days primarily based on present occasions and 2021 forecasts from main housing authorities.

Lock in today’s rates before they rise (Apr 24th, 2021)

Predictions for Might 2021

Wish to keep forward of mortgage fee traits in Might? Right here’s what you need to be keeping track of within the coming month.

Will mortgage charges go down in Might?

Regardless of shock fee drops in April — 30-year mounted charges fell to three.04% on April 15 — mortgage charges appear sure to show again upwards quickly.

Why did rates of interest fall within the first place? The brief reply is that COVID remains to be driving uncertainty in monetary markets. (Extra element on this beneath.)

But restoration is forging on — making a push and pull between pandemic issues (which drive charges down) and financial optimism (which usually means larger charges).

So, do you have to anticipate decrease charges in Might?

Presumably — but when they do occur, it would possible be a blip in an total upward pattern. We wouldn’t advise banking on decrease charges for a sustained time.

In reality, charges for some debtors have already risen. Reports with extra up-to-date numbers than Freddie Mac put common charges above 3.20% on the identical day as Freddie’s current low.

Should you’re able to lock a fee, sooner is healthier than later.

Find and lock a low rate (Apr 24th, 2021)

Why did mortgage charges fall in April?

In April, we had been keeping track of various large financial stories: jobs and unemployment, inflation, and retail gross sales.

These stories are key indicators of how the financial system is faring. And so they can have a large influence on mortgage charges.

Stronger-than-expected financial readings are able to inflicting vital fee spikes.

Worse-than-expected information ought to sometimes drive charges down.

As predicted, this month’s stories have been booming.

Jobless claims are down; retail gross sales acquired their largest increase in a yr whereas the companies sector noticed its strongest development ever; and inflation rose greater than anticipated as demand for items and companies continued to speed up.

And but — mortgage charges fell.

That’s the precise reverse of what ought to occur in a ‘regular’ market. So what’s occurring?

Some businesses predict 30-year charges as excessive as 3.65% by the tip of summer season.

The easy reply is that this isn’t a traditional market. COVID remains to be within the driver’s seat.

Across the similar time we noticed these sturdy inflation numbers – which might have induced a fee spike – issues had been mounting round potential unwanted effects from the Johnson & Johnson vaccine.

Then the CDC and FDA formally put the J&J vaccine on pause, probably slowing vaccine rollout throughout the U.S. (Though President Biden nonetheless believes there’s sufficient provide to get each American vaccinated by the end of May.)

In the meantime, COVID instances are nonetheless excessive, even rising barely as states start to reopen extra broadly. And issues about new variants imply we’re removed from being out of the weeds totally.

Though the outlook has “brightened considerably,” as Fed Chair Powell mentioned on 60 Minutes, “the principal danger to our financial system proper now actually is that the illness would unfold once more.”

Anticipate the sudden — however don’t await it

Continued pandemic danger signifies that for the foreseeable future, we will’t anticipate markets to behave like regular.

We’re nonetheless anticipating larger charges all year long because the financial restoration is imminent.

Some businesses even predict 30-year charges as excessive as 3.65% by the tip of summer season.

Nevertheless, COVID has been and continues to be unpredictable. Additional vaccine delays or the unfold of variants might drag down financial development. And that might create spells of decrease charges within the short-term.

As we mentioned above, although — don’t rely on it. Charges are way more prone to go up in Might and the next months.

Lock in today’s rates. Start here (Apr 24th, 2021)

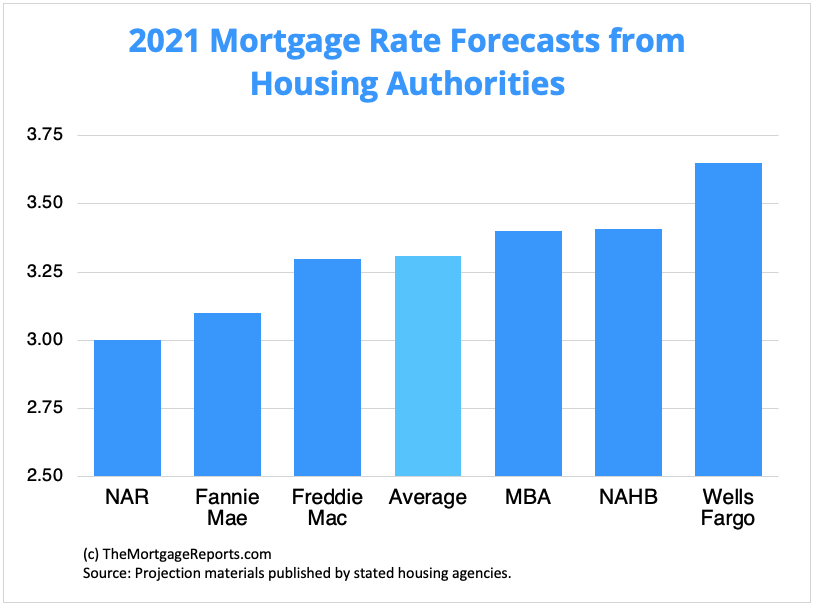

Mortgage fee traits as predicted by housing authorities

Housing businesses nationwide are calling for charges within the low- to mid-3s by the third quarter of 2021.

| Company | 30-Yr Fee Prediction |

| Nationwide Assoc. of Realtors | 3.00% |

| Fannie Mae | 3.10% |

| Freddie Mac | 3.30% |

| Mortgage Bankers Assoc. | 3.40% |

| Nationwide Assoc. of Dwelling Builders | 3.41% |

| Wells Fargo | 3.65% |

| Common of all businesses | 3.31% |

To sum it up, fee predictions differ extensively.

Mortgage charges might keep close to historic lows all year long. Or they might spike as much as pre-2020 ranges.

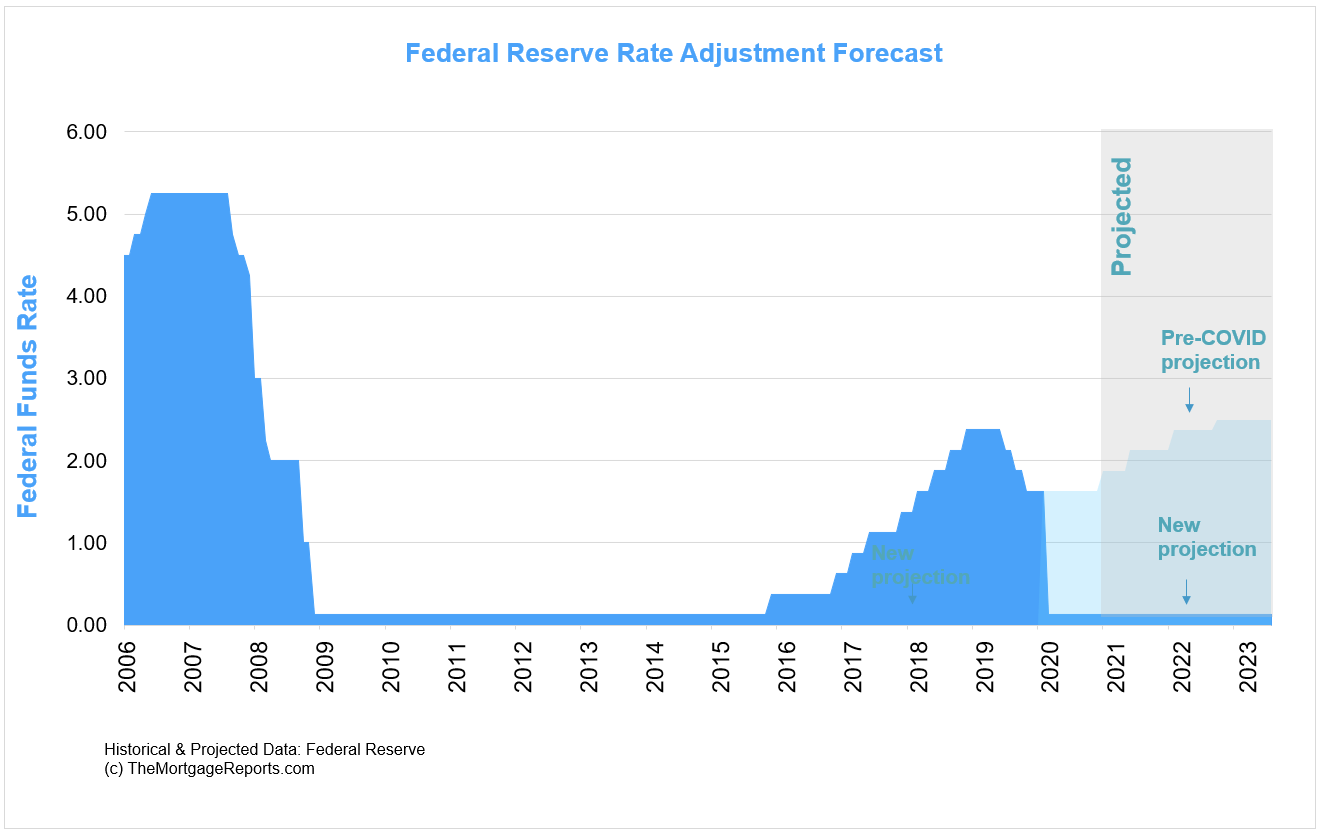

The Fed to maintain its benchmark fee low till 2023

The Federal Reserve has a number of levers with which to maintain charges low within the financial system.

Mortgage charges are most closely affected by the Fed’s bond buying program. All through the pandemic, the Federal Reserve has been shopping for $40 billion value of Mortgage Backed Securities (MBS) monthly.

MBS prices drive mortgage rates, and the Fed’s injection of money into this market pushed charges to their lowest lows in 2020.

One other, oblique methodology of fee suppression is for the Fed to maintain its benchmark fee — the federal funds fee — close to zero.

This fee stage permits banks to borrow cash at practically no price, which has a trickle-down impact on shopper borrowing and rates of interest basically.

The Fed’s present rate-friendly stance is a boon for mortgage customers.

What does this imply for the private funds of the common

American shopper?

It means you’ll possible have entry to ultra-low charges for years. Maybe not as little as they’re now, however very low from a historic standpoint.

Verify your new rate (Apr 24th, 2021)

Mortgage methods for Might 2021

With mortgage charges on the rise, listed here are the methods we imagine to be most necessary for residence patrons and owners within the coming months.

Excessive credit score? Don’t be afraid to barter

Prime debtors — these with excessive credit score and 20% down — have an edge within the mortgage market.

You could have your choose of lenders, mortgage packages, and mortgage charges. That’s an enormous benefit you shouldn’t let go to waste.

One of many largest errors you can also make when refinancing or shopping for a home goes with the primary give you get.

On the day this was written, we noticed one main lender providing 3.25% for a 30-year fixed-rate mortgage, and one other providing 2.625% on the identical mortgage sort.¹

Fee procuring might prevent round $1,200 per yr on a $300,000 mortgage.

That’s a distinction of 62.5 foundation factors — over half a %!

Reducing your fee by 0.625% on a $300,000 mortgage might prevent $100 on every mortgage cost; $1,200 per yr; and $36,000 over 30 years.

In right now’s rising fee atmosphere, procuring in your finest fee is doubly necessary.

Some lenders are nonetheless providing near-record low charges for the most effective debtors, however you must hunt for them.

You could even get lenders to compete for your business by exhibiting a suggestion with a decrease rate of interest or charges and asking them to match it. However you received’t know till you attempt.

Find your lowest mortgage rate (Apr 24th, 2021)

Low credit score? Ensure you examine all of your choices

The previous yr has been robust for debtors with less-than-perfect credit score or non-traditional employment.

Lenders tightened up credit score and revenue necessities to reduce their danger throughout COVID, placing some otherwise-qualified debtors out of the working for financing.

Immediately’s mortgage market has even been described as a ‘no man’s land’ for these with credit score scores beneath 700 or unsure revenue.

Nevertheless, issues are starting to look again up.

Mortgage credit availability has increased for the reason that top of the pandemic — which implies qualifying for a house mortgage is getting simpler.

However not all lenders will return to pre-pandemic requirements on the similar tempo.

What does that imply for you?

Should you’re available in the market for a low-credit or low-down-payment home loan, you need to be ready to use with a number of lenders.

That’s very true for debtors with FICO scores beneath 700-720, or non-traditional revenue sources like self-employment.

Financing choices are on the market for certified debtors, however they might be tougher to search out.

So go in with the suitable mindset and don’t hand over till you’re certain you’ve checked all of your choices.

Verify your mortgage eligibility (Apr 24th, 2021)

Use low cost factors to your benefit

Rates of interest are rising, however savvy mortgage customers can nonetheless get an awesome deal.

Your first step is to buy with a number of mortgage lenders. Evaluating fee quotes from at the least 3 corporations is the one ‘actual’ strategy to discover the most effective pricing.

However there are different methods to decrease your fee, too.

Discount points provide the energy to ‘purchase down’ your mortgage fee by paying further at closing.

Doing so isn’t low cost. You’ll sometimes pay 1% of your mortgage quantity to decrease your fee by 0.25%.

However the total financial savings can far outweigh the price of low cost factors when you plan to remain in your house for five years or extra.

Have your lender present you mortgage choices with and with out low cost factors so you’ll be able to evaluate the upfront price vs. long-term financial savings and see if shopping for down your fee is value it.

Consumers: It’s time to up the ante on affords

Low mortgage charges have made residence shopping for extra reasonably priced for the common American. However they’re a double-edged sword.

With charges low and Individuals returning to work, the market is oversaturated with patrons and undersupplied with houses.

Housing stock fell to a file low on the finish of February. And houses that hit the market are promoting in file time — simply 20 days on common.

That doesn’t imply it is best to hand over hope, although.

It simply means you have to get sensible about making a suggestion.

Consumers in right now’s actual property market must be knowledgeable and well-prepared in the event that they need to get a suggestion accepted on their dream residence.

How are you going to enhance your probabilities?

- Get pre-approved for a mortgage earlier than you make a suggestion. That is an absolute should, as most sellers and brokers received’t even have a look at a suggestion and not using a pre-approval letter

- Don’t bid your total pre-approved quantity instantly. You may suppose it is best to make your strongest supply proper off the bat. But when your first bid is in your total pre-approved mortgage quantity, you received’t have any wiggle room to counter with a better supply

- Don’t embrace too many contingencies. Contingencies decelerate actual property transactions. In a scorching market, sellers usually tend to settle for a suggestion with fewer contingencies, so restrict yours to what’s completely crucial

- Don’t skip the house inspection. This might sound tempting because it might assist you transfer sooner in your buy. However when you skip a home inspection, you may suppose you’re shopping for a turn-key residence solely to finish up with a fixer-upper

Start your mortgage pre-approval today (Apr 24th, 2021)

Mortgage product fee updates

Many mortgage customers don’t notice there are various kinds of charges in right now’s mortgage market.

However this data can assist residence patrons and refinancing households discover the most effective worth for his or her state of affairs.

Following are updates for particular mortgage sorts and their corresponding charges.

Standard mortgage charges

Conventional refinance rates and people for residence purchases are transferring away from record-low territory, though they’re nonetheless at a low level traditionally.

In line with mortgage software program firm Black Knight, the 30-year mortgage fee averaged 3.34% in March (the newest knowledge out there), up considerably from round 2.9% in February.

Remember, although, common charges account for all types of debtors.

One of many benefits of a traditional mortgage is that debtors with larger credit score and greater down funds are rewarded with decrease charges.

So even in a rising fee atmosphere, ‘prime’ debtors can typically nonetheless discover nice offers.

Decrease-credit-score debtors can use typical loans, too. However these loans are finest suited to these with first rate credit score and at the least 3% down.

5 % down is preferable as a consequence of larger charges that include decrease down funds.

Twenty % fairness is most popular when refinancing.

With sufficient fairness within the residence, a traditional refinance can repay any mortgage sort. Received an Alt-A, subprime, or high-PMI mortgage? A conventional refi can care for it.

For example, say you bought a house three years in the past with an FHA loan at 3.5 % down. Since then, residence costs have skyrocketed.

Due to your larger residence worth, you now have 20 % fairness, which implies you could possibly refinance into a traditional mortgage and eliminate FHA mortgage insurance.

This may very well be a financial savings of

a whole bunch of {dollars} monthly, even when your rate of interest goes up.

Eliminating mortgage insurance coverage is an enormous deal in any mortgage market. This mortgage calculator with PMI estimates your present mortgage insurance coverage price. Enter a 20 % down cost to see your new cost with out PMI.

Find a low conventional loan rate. Start here (Apr 24th, 2021)

FHA mortgage charges

FHA is at present the go-to program for residence patrons who might not qualify for typical loans.

The excellent news is that you’re going to get an identical fee — and even decrease — with an FHA mortgage mortgage than you’d with a traditional one.

In line with Black Knight’s Origination Market Monitor, FHA mortgage charges averaged 3.33% in March, a hair beneath the common typical fee.

One other fascinating stat from the report: The typical FICO rating for FHA residence patrons is at present simply 666, in comparison with 751 for conforming mortgage debtors.

Associated: Learn extra about FHA prices and necessities on our FHA loan calculator page.

FHA loans include mortgage

insurance coverage. However the total price is just not far more than for typical loans.

A little bit-known program, known as the FHA streamline refinance, enables you to convert your present FHA mortgage into a brand new one at a decrease fee if charges are actually decrease.

An FHA streamline mortgage software requires

no W2s, pay stubs, or tax returns. And also you don’t want an appraisal, so residence

worth doesn’t matter.

Find low FHA rates. Start here (Apr 24th, 2021)

VA mortgage charges

VA loans include the bottom charges of all mortgage sorts in line with Black Knight.

In March, (the newest knowledge out there), 30-year VA mortgage charges averaged simply 2.97% whereas typical loans averaged 3.34%, representing an enormous low cost when you’re a veteran or service member.

Owners with a present VA mortgage could also be eligible for the ever-popular VA streamline refinance.

No revenue, asset, or appraisal documentation is required.

Should you’ve skilled a lack of revenue or diminished financial savings, a VA streamline can get you right into a decrease fee and higher monetary state of affairs. That is true even whenever you wouldn’t qualify for the standard refinance.

Don’t overlook the VA mortgage for residence shopping for. It requires zero down cost.

However don’t overlook the VA loan for home buying. It requires zero down cost.

Which means when you have the money for closing prices, or can get them paid for by the vendor, you should purchase a house with out saving any extra funds.

VA mortgages are supplied by native and nationwide lenders, not by the federal government instantly. Most active-duty members or veterans of the US army can qualify.

This public-private partnership affords customers the most effective of each worlds: sturdy authorities backing and the comfort and pace of a non-public firm.

Most lenders will settle for credit score scores all the way down to 620, and even decrease. Plus, you don’t pay excessive rates of interest for low scores.

Verify your month-to-month cost with this VA loan calculator.

There’s unbelievable worth in VA loans.

Check today’s VA loan rates. Start here (Apr 24th, 2021)

USDA mortgage charges

Due to their backing from the U.S. Division of Agriculture, USDA mortgage charges are ‘below-market.’ Which means you’ll sometimes get a decrease fee with USDA than typical financing.

And there are different advantages, too.

Like FHA and VA, present USDA mortgage holders can refinance by way of a “streamlined” course of.

With the USDA streamline refinance, you don’t want a brand new appraisal. You don’t even should qualify utilizing your present revenue. The lender will solely just remember to are nonetheless inside USDA revenue limits.

Dwelling patrons are additionally studying the advantages of the USDA loan program for home buying.

No

down cost is required, and charges are ultra-low.

Dwelling funds may be even decrease than lease funds, as this USDA loan calculator reveals.

Qualification is less complicated as a result of

the federal government desires to spur homeownership in rural areas. Dwelling patrons may

qualify even when they’ve been turned down for an additional mortgage sort up to now.

Like FHA and VA loans, the USDA program is for individuals who

need to purchase or refinance a main residence; these mortgage packages aren’t for

actual property builders.

Find a lock a low USDA rate (Apr 24th, 2021)

Mortgage charges right now

Whereas monitoring month-to-month mortgage fee forecasts and weekly averages may be useful, it’s necessary to know that charges change day by day.

You may get 3.00% right now, and three.125% tomorrow. Many elements alter the course of present mortgage charges.

To get a synopsis of what’s taking place right now, go to our daily rate update. You will discover stay charges and lock suggestions.

Might financial calendar

The subsequent 30 days maintain no scarcity of market-moving information. Usually, information that factors to a strengthening financial system might imply larger charges, whereas dangerous information from economists could make charges drop.

- Friday, Might 7: Nonfarm Payrolls, wages, unemployment fee

- Wednesday, Might 12: Inflation Fee

- Friday, Might 14: Retail Gross sales

- Monday, Might 17: NAHB Housing Market Index

- Tuesday, Might 18: Housing Begins, Constructing Permits

- Wednesday, Might 19: April FOMC Minutes

- Tuesday, Might 25: Current Dwelling Gross sales

- Thursday, Might 27: GDP Progress Fee, Pending Dwelling Gross sales

- Friday, Might 28: Private Revenue, Private Spending

Now may very well be the time to lock in a fee in case these occasions push up charges this month.

Mortgage charges Q&A

Beneath are a number of the commonest questions on mortgage charges.

Mortgage charges as an entire are nonetheless at historic lows. However particular person charges fluctuate primarily based on market situations and your particular state of affairs. For example, somebody with a excessive credit score rating will get a decrease fee than somebody with a low rating.

Mortgage charges usually tend to rise than fall all through the remainder of 2021. In line with our survey of main housing authorities similar to Fannie Mae, Freddie Mac, and the Mortgage Bankers Affiliation, the 30-year fixed-rate mortgage will common round 3.31% by 2021.

Sure. Lenders have the flexibleness to drop their charges and costs. Usually, you need to strategy a lender with a greater supply in writing earlier than they’ll decrease their fee.

Traditionally, it’s a improbable mortgage fee. However, charges are at present hovering decrease than this for well-qualified candidates. The typical fee since 1971 is greater than 8% for a 30-year mounted mortgage. To see if 3.5% is an efficient fee proper now and for you, get 3-4 mortgage quotes and see what different lenders supply. Charges differ vastly primarily based in the marketplace and your profile (credit score rating, down cost, and extra).

Most corporations have comparable charges. Nevertheless, some supply ultra-low charges to realize market share. Others have decrease charges for FHA than typical, or vice versa. The one strategy to know if your organization is providing the bottom fee is to get quotes from numerous lenders.

A degree is a payment equal to 1 % of your mortgage quantity, or $1,000 for each $100,000 borrowed. Your rate of interest might drop 1 / 4 to a half a proportion level or extra for every level paid. Nevertheless, that may differ relying on the lender, mortgage traits, and borrower profile.

You’ll be able to 1) request a lender credit score; 2) request a vendor credit score (if shopping for a house); 3) enhance your mortgage fee to keep away from factors; 4) get a down cost reward (which can be utilized for closing prices); 5) get down cost help.

Treasury yields and mortgage charges aren’t instantly linked, however they’re strongly correlated. 10-year Treasury yields and 30-year mounted mortgage rates of interest have a tendency to maneuver in lock step with each other. That’s as a result of each merchandise are purchased on the secondary market by the identical forms of traders.

Mortgage charges are larger than Treasury yields as a result of mortgages are inherently extra dangerous. Rates of interest for mortgages are primarily based on costs for mortgage-backed securities (MBS). The identical elements that drive MBS up or down normally drive Treasuries up or down, therefore the widespread false impression that Treasuries drive mortgage charges.

The Fed doesn’t set mortgage charges, however its financial insurance policies affect mortgage markets. In instances of financial uncertainty, the Fed promotes decrease rates of interest to encourage extra borrowing which helps stimulate the financial system. Decrease charges may increase residence values which bolsters many Individuals’ web value.

Should you entered into mortgage forbearance due to the coronavirus pandemic, you might be able to qualify for a refinance after exiting your forbearance plan. Should you missed funds throughout forbearance, you’ll should make three consecutive on-time funds earlier than qualifying for a traditional refinance, in line with FHFA’s guidelines.

What are right now’s mortgage charges?

Low mortgage charges are nonetheless out there. You may get a fee quote inside minutes with only a few easy steps to begin.

Verify your new rate (Apr 24th, 2021)

Chosen sources:

- https://www.blackknightinc.com/data-reports/

- https://tradingeconomics.com/united-states/calendar

- https://www.federalreserve.gov/monetarypolicy/fomccalendars.htm

- http://www.freddiemac.com/analysis/datasets/refinance-stats/index.web page

¹Source: http://www.mortgagenewsdaily.com/mortgage_rates/evaluate/ Date: April 15, 2021. Quicken Loans marketed 30-year mounted fee of three.250% with 2.0 factors. AmeriSave marketed 30-year mounted fee of two.625% with 1.556 factors. These charges are for pattern functions solely. Your personal fee will differ.

[ad_2]

Source link

{kind=link}