[ad_1]

Mortgage necessities are loosening

There’s excellent news for residence patrons: It’s lastly getting simpler to get a mortgage mortgage.

After tightening their lending requirements through the pandemic, it appears mortgage lenders are beginning to loosen the reins a bit.

The truth is, in response to the Mortgage Bankers Association, mortgages had been about 2.2% simpler to come back by in April than in March. And on some sorts of loans? Mortgage availability was up as a lot as 12.6%.

Right here’s what the change means for home buyers (and refinancers).

Verify your mortgage eligibility today (May 25th, 2021)

Why did mortgage necessities get harder throughout COVID?

Final 12 months was a dangerous time for lenders to mortgage out cash. Unemployment hit record-breaking ranges, many individuals misplaced jobs and wages, and full sections of the economic system had been shut down for months.

To guard themselves from these added dangers, many mortgage lenders raised mortgage necessities. Some even stopped providing sure mortgage packages altogether (specifically FHA loans, HELOCs, and non-QM loans).

For essentially the most half, lenders required larger credit score scores and bigger down funds over the past 12 months.

For instance, at one level Chase raised its credit score rating requirement to a whopping 700 and requested for 20% down funds on all buy loans. (Usually, it’s potential to get a conventional mortgage with a credit score rating of 620 and solely 3% down.)

Different mortgage lenders added a second employment verification — one simply earlier than the time limit — as an additional layer of safety as effectively.

Mortgage necessities are actually loosening once more

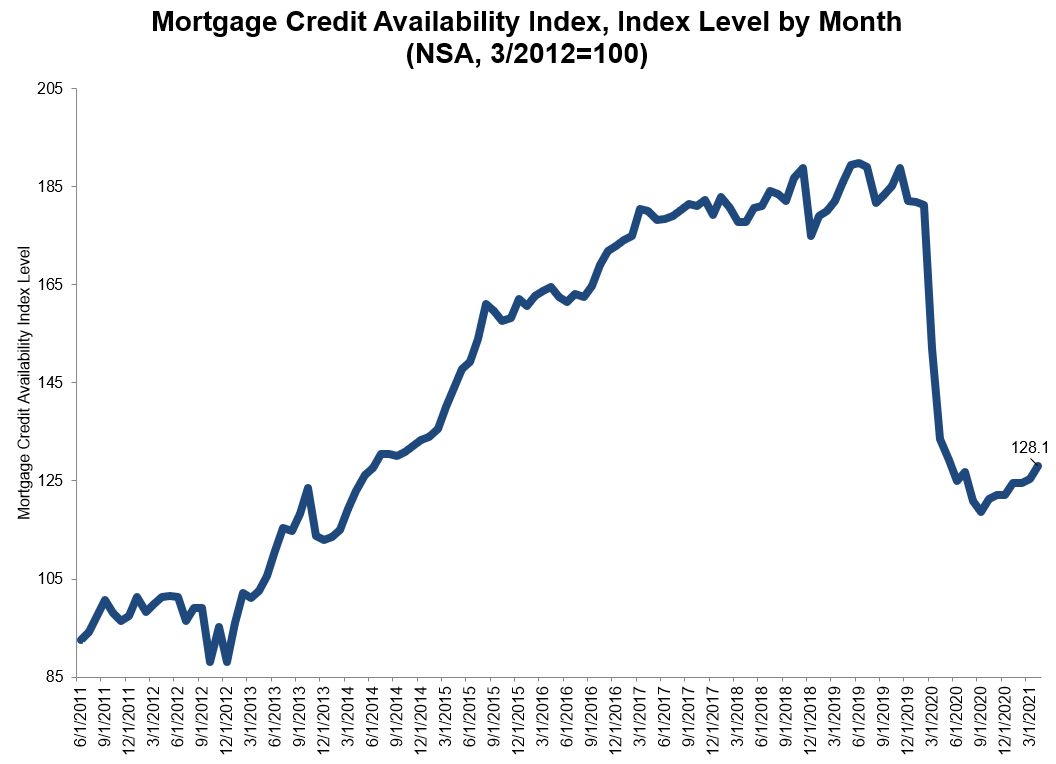

In response to the Mortgage Credit score Availability Index from MBA, these excessive requirements are lastly beginning to ease up.

The MCAI elevated by 2.2% general in April, which signifies requirements are getting much less strict.

Conforming mortgage necessities

Requirements for credit score rating, down cost, and different standards loosened essentially the most on conforming loans, with a 12.6% leap over the month.

Conforming loans are those who meet requirements set by Freddie Mac and Fannie Mae. The businesses permit credit score scores beginning at 620 and down funds of 3-5% or larger.

Nonetheless, lenders are allowed to set their very own, stricter necessities on prime of Fannie and Freddie’s (referred to as ‘overlays’). These overlays are the explanation mortgage necessities differ a lot from one lender to the subsequent — and the explanation some lenders are re-opening to lower-credit debtors sooner than others.

In case you assume it’s best to qualify however get turned down by one lender, it’s value making use of with just a few others to see if their completely different pointers can work in your favor.

Compare mortgage options. Start here (May 25th, 2021)

Necessities for different mortgage varieties

Jumbo loans — that are reserved for higher-priced property purchases — additionally noticed an enormous availability improve of practically 7%.

Authorities loans, which embrace FHA, USDA, and VA mortgages, aren’t seeing the identical pattern, in response to MBA’s information.

The MCAI for these packages elevated a mere 0.1% from March to April, indicating lending requirements are largely holding regular.

Credit score availability nonetheless not again to 2020 highs

Total, mortgage credit score availability is enhancing. That is making it simpler for a lot of People to buy a house or refinance.

Nonetheless, mortgage necessities haven’t recovered to pre-pandemic ranges — and even close to them, actually.

Beforehand, the mortgage credit score index was effectively into the 170s and 180s. At this time, it’s simply 128.1.

Because the economic system picks up extra post-pandemic steam — and as soon as fewer mortgage loans are in forbearance — credit score availability ought to proceed to enhance.

So if you happen to don’t qualify for a house mortgage at the moment, don’t lose hope. Requirements ought to proceed to ease up because the 12 months goes on.

In case you’re undecided whether or not you’d qualify now or within the close to future, see:

How you can qualify in at the moment’s market

Regardless of the uptick, it’s nonetheless tougher to get a mortgage than it was just a few years in the past.

In case you’re fearful chances are you’ll not qualify for a mortgage, be sure you work in your credit score earlier than making use of for a mortgage.

You also needs to save up a strong down cost, and store round with a minimum of three to 5 completely different lenders. Each mortgage lender has completely different qualifying requirements, so buying round can assist you discover the best choice in your distinctive state of affairs and price range.

In response to Freddie Mac, evaluating mortgage affords may prevent critical money (about $3,000 if you happen to get a minimum of 5 quotes!)

[ad_2]

Source link

{kind=link}