[ad_1]

Lately, it appears as if you happen to can insure absolutely anything. Your automotive, your own home, your canine, your telephone, and perhaps even your hair?

At one time, there was a type of home down payment insurance, which finally look seems to not exist.

Whereas all these new coverage choices could also be perceived as “nice information!” by overzealous insurance coverage brokers, for particular person shoppers it’s usually simply more cash down the drain.

In any case, paying for insurance coverage at all times looks like a chump’s sport till you truly must file a declare, which by no means appears to occur if you happen to even have insurance coverage in place.

And if you happen to do file a declare, your insurance coverage charges will go up! What a deal!

While you buy a house, your insurance coverage wants will definitely rise, which is able to put much more pressure in your already-strained checkbook.

Let’s take a look at two frequent types of insurance coverage tied to homeownership, and discover what every truly supplies.

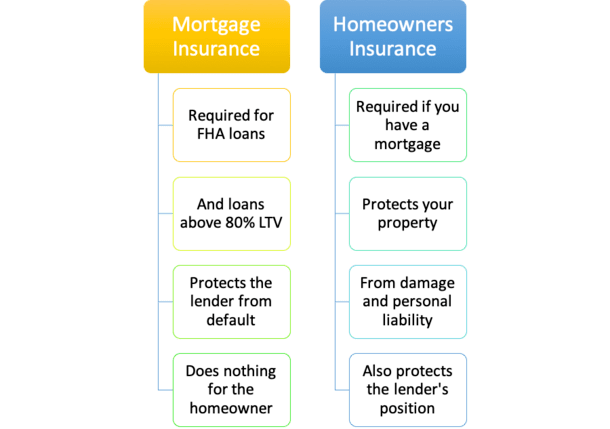

Mortgage Insurance coverage Protects the Financial institution/Lender

- Mortgage insurance coverage doesn’t defend householders

- It protects the mortgage lender from cost default

- It exists as a result of they’re taking a much bigger threat by providing you a house mortgage with little or no down

- The trade-off is you get a mortgage regardless of having a large down cost

When you’ve been shopping for a home (and a house mortgage) these days, you might have heard about mortgage insurance coverage.

At first look, it would sound like one thing that protects you within the occasion you may’t pay the factor.

However opposite to what you would possibly imagine, mortgage insurance coverage doesn’t do something to guard the house owner.

Conversely, it serves to guard mortgage lenders within the occasion of borrower default, one thing deemed essential if you put down lower than 20% on a house buy.

In brief, you pay additional for the extra threat you current to the lender. And till your loan-to-value ratio (LTV) dips under 80%, you’ll proceed to pay that premium.

When you take out a standard mortgage above 80% LTV, you’ll want private mortgage insurance (PMI), which your lender will facilitate when going by means of the mortgage course of.

When you take out an FHA loan, you’ll get mortgage insurance coverage by means of the FHA. And it’s not avoidable, even if you happen to’re in a position to put down 20% or extra.

So we all know a bit extra about mortgage insurance coverage, however let’s discuss what it isn’t.

It isn’t insurance coverage that protects you within the occasion you may’t make your mortgage payment.

For instance, if you happen to lose your job or fall sick and are unable to make funds, mortgage insurance coverage doesn’t cowl you.

That’s a wholly totally different product generally known as “mortgage protection insurance.” Sure, there’s insurance coverage for each single attainable scenario people!

It additionally doesn’t cowl you if your own home worth falls, or if anything nasty occurs to your own home or your mortgage. Once more, it’s not for YOU. It’s for the lender! And also you pay for it!

That is but one more reason to put 20% down when buying property. The opposite cause is a decrease mortgage rate, which are sometimes cheaper at decrease LTVs.

Householders Insurance coverage Protects You

- It’s important to purchase householders insurance coverage you probably have a mortgage

- However this sort of coverage truly protects you within the occasion of property injury or legal responsibility

- So the protection is helpful to the house owner if one thing catastrophic takes place

- It not directly protects the lender too as a result of the house serves as collateral for the mortgage

I assume a whole lot of people get homeowners insurance and mortgage insurance coverage confused, and for good cause.

They sound fairly related, however don’t share a lot in frequent.

Householders insurance coverage is definitely in place to guard YOU, the house owner, from perils that exist and will trigger injury and financial loss.

So if a hearth burns down your own home, or a tree crashes by means of your roof, your householders insurance coverage ought to be triggered.

And the insurance coverage firm ought to pay to repair any damages, much less your deductible.

In different phrases, householders insurance coverage serves the proprietor of the house, not the lender. It additionally has nothing to do with your own home mortgage, although there may be some overlap.

Technically, if you happen to personal your own home outright, you don’t NEED to get householders insurance coverage. However you’d be fairly silly to not buy it if your own home has any vital worth.

With out it, you possibly can expose your self to main monetary threat, which clearly isn’t sensible with insurance coverage premiums comparatively low-cost within the grand scheme of issues.

And also you actually wouldn’t need to jeopardize your means to make mortgage funds if all of your cash was caught up in dwelling repairs.

Householders Insurance coverage Additionally Protects the Lender’s Curiosity

Whereas householders insurance coverage does certainly profit the house owner, it additionally protects lenders (though you pay for it).

Why? As a result of most people don’t truly personal their houses free and clear, or wherever near it.

Keep in mind how mortgage insurance coverage is required if you happen to put little or no down on a house buy? Effectively, lots of people put little or no down!

The typical down cost ranges from like 6-12% relying on the survey/information set, so most houses throughout America are majority-owned by banks and mortgage lenders.

This additionally explains why you MUST take out a householders insurance coverage coverage you probably have a mortgage, to guard the lender’s curiosity.

At this level, you could be considering it’s all concerning the lender. However when it comes right down to it, you’ve received an enormous mortgage on the property, so it’s actually the financial institution’s greater than it’s yours.

And with out insurance coverage in place, within the occasion of a significant loss, most householders would in all probability run, not stroll, away from the property.

Lenders know this, which is why they demand that you simply purchase householders insurance coverage.

The excellent news is mortgage insurance coverage is completely avoidable. Simply convey more cash to the closing desk or take a look at lender-paid mortgage insurance.

You may also be capable of discover a lender that doesn’t cost it. Simply know if you happen to put lower than 20% down they usually aren’t charging it, it’s baked into your (greater) mortgage charge.

[ad_2]

Source link

{kind=link}