[ad_1]

What precisely is a doctor mortgage mortgage?

Doctor loans, additionally known as “physician loans”, have particular advantages for MDs and different medical professionals.

A doctor mortgage may prevent cash by decrease charges and mortgage prices. Or, it’d make it simpler for brand spanking new medical doctors to qualify for a mortgage recent out of medical faculty with a brand new job and scholar mortgage debt.

Some physicians will do nicely with a specialised mortgage mortgage, whereas others might discover their greatest wager is a standard mortgage program. Discover what’s accessible and select one of the best deal for you.

Find the right loan for you. Start here (Dec 1st, 2021)

On this article (Skip to…)

Advantages of doctor loans

Some differentiate between physicians and surgeons. However mortgage lenders don’t. After they speak about doctor loans, or physician mortgage loans,, they imply ones for medical doctors, typically. Some rely different healthcare professionals, too, together with veterinarians, dentists and orthodontists with DMV, DPM, DDS and DMD levels.

These loans can ship some very particular privileges to these within the occupation, together with:

- No personal mortgage insurance coverage (PMI), even when your down fee is small or zero

- Low charges on closing

- Inexpensive entry to jumbo mortgages – often these over $

- Approval based mostly on a signed employment contract fairly than pay stubs

- Fewer hassles over scholar debt

- Could also be simpler to get a self–employed mortgage with a shorter job historical past

However some mortgage insiders warn there are cons with doctor loans in addition to professionals. So learn on to find the essential information about the physician mortgage.

How do doctor loans work?

Doctor loans permit medical doctors and medical professionals to buy a house sooner than they might with a standard mortgage.

You may qualify for a doctor mortgage with no cash down, versatile employment historical past, or a better than regular debt–to–earnings ratio – with none main mortgage insurance coverage requirement.

Since PMI is mostly round 0.5% to 1% of your mortgage quantity per 12 months, the PMI waiver profit can save householders 1000’s of {dollars}.

Who qualifies for a doctor mortgage?

Most doctor mortgage applications are aimed toward medical residents, medical medical doctors, attendings, fellows, and first care physicians. However it’s as much as every lender to determine who qualifies. Many embody dentists and optometrists, and a few embody veterinarians.

The checklist of eligible medical specialists who qualify for a doctor mortgage depends on the mortgage lender, so you’ll want to speak to your mortgage officer about eligibility.

Typically, these medical professionals usually qualify for doctor mortgage applications:

- Medial medical doctors (MD)

- Nurse Practitioners (NP)

- Docs of Chiropractic (CD)

- Docs of Dental Drugs (DMD)

- Docs of Dental Surgical procedure (DDS)

- Docs of Optometry (OD)

- Docs of Pharmacy (PharmD)

- Docs of Podiatric Drugs (DPM)

- Docs of Veterinary Drugs (DVM)

It’s additionally as much as lenders to decide on the opposite standards they’ll use when deciding whether or not to lend and the mortgage charge they’ll cost.

Many lenders shall be additional–lenient on physicians – even these and not using a conventional two–12 months employment historical past – as a result of their excessive incomes potential makes lending a really secure prospect.

Certainly, some estimate that physicians default on loans at a charge of 0.2% whereas shoppers typically accomplish that about six occasions as usually.

However bear in mind, earnings isn’t the one factor that issues.

The golden rule nonetheless applies: The upper your credit score rating and down fee, and the extra secure your funds, the higher the rate of interest you’re more likely to be provided.

Find the right loan for you. Start here (Dec 1st, 2021)

Credit score rating

To get the perfect charges, you’re more likely to want a credit score rating north of 750.

However don’t fear when you don’t have that. There’s an inexpensive likelihood of discovering a doctor mortgage even when your rating’s down at 680 or so. You’ll simply pay a bit extra for it.

Two different elements could be taken under consideration in case your credit score rating is decrease than you’d like:

- If the remainder of your mortgage utility is powerful: You probably have a chunky down fee and only a few different money owed, your lender could also be much less fearful about your rating

- In case your credit score rating is low as a result of you’ve got a “skinny file”: In lender communicate, a “skinny file” arises since you haven’t borrowed a lot up to now, leaving your credit score document a bit sparse. That’s much more forgivable than your having “earned” your low rating by monetary mismanagement

Mortgage lenders could also be extra indulgent with regards to physicians. However they nonetheless anticipate you to satisfy fundamental credit score necessities.

Down fee

It’s completely doable to seek out physician house loans that require no cash down in any respect. Sure, you may want some money for closing, although some help you roll these prices up inside your mortgage.

Others are pleased to lend you 80%, 90%, 95% or extra of the house’s appraised worth.

Avoiding mortgage insurance coverage when your down fee is low or zero is without doubt one of the largest benefits provided by doctor mortgage mortgage applications.

Crucially, physicians might have entry to those low– or zero–down loans with out mortgage insurance.

That insurance coverage is an actual burden for non–doctor debtors with small down funds. They will find yourself paying lots of of {dollars} each month to guard their lenders from the danger of their defaulting.

So avoiding mortgage insurance coverage when your down fee is low or zero is without doubt one of the largest benefits provided by doctor mortgage mortgage applications.

Debt–to–earnings ratio

We’ve coated two of the three issues that mortgage lenders take a look at most carefully when deciding whether or not to give you a mortgage and the way good a deal you’re due.

The third is your debt–to–income ratio or “DTI.”

DTI is “an individual’s month-to-month debt load as in comparison with their month-to-month gross earnings.”

To get the “debt” quantity, you add up your month-to-month debt funds (minimal month-to-month funds on bank cards, scholar mortgage funds, alimony, youngster help …) plus your inescapable housing costs, equivalent to new mortgage fee, housing affiliation charges, and property taxes.

How large a piece of your pretax month-to-month earnings does that characterize?

If it’s lower than 43%, most lenders will suppose that’s effective. If it’s extra, many debtors have issues, although some lenders permit as much as 50% for sure kinds of mortgages. Nonetheless, physicians might get some additional leeway.

[cta-link linktext=”Check today’s best rates. Start here”]

Can medical doctors get mortgages and not using a two–12 months employment historical past?

One widespread situation new medical doctors face when attempting to get a standard mortgage is a scarcity of employment historical past.

Whether or not you’re a salaried worker or a self–employed contractor, mortgage lenders sometimes need to see a two–12 months historical past of regular earnings to qualify you for a standard house mortgage.

Docs recent out of medical faculty, or model new to their very own apply, received’t have that two–12 months documentation to again them up. That is often grounds to disclaim somebody a mortgage.

It could be doable to get a doctor mortgage mortgage on the energy of a contract or supply letter alone, or with as little as 6 months self–employment historical past.

That’s the place physician house loans are available.

Lenders are sometimes pleased to approve physicians and different medical professionals with little employment historical past, because of their excessive incomes potential.

Thus, it could be doable to get a doctor mortgage on the energy of a contract or supply letter alone. And self–employed medical doctors may have the ability to get a mortgage based mostly on as little as six months’ self–employment historical past.

Which banks supply doctor mortgage applications?

Scores of banks and credit score unions throughout the nation have doctor mortgage mortgage applications. Some are comparatively small, however a quantity are bigger names you’ll have heard of.

Right here’s a sampling of banks that provide particular mortgage applications for physicians.

- Bank of America

- Arbor Monetary Credit score Union

- Chemical Financial institution

- Fairway Unbiased Mortgage

- Fifth Third Financial institution

- First Nationwide Financial institution

- Huntington Nationwide Financial institution

- KeyBank

- Lake Michigan Credit score Union

- loanDepot

- Areas Financial institution

- US Bank

- SunTrust Mortgage (together with BB&T Financial institution. Now, collectively, Truist Financial institution)

- TD Financial institution

- College Federal Credit score Union

You’ll see they’re in alphabetical order. And that’s as a result of we’re not attempting to rank them. However hyperlinks to lender reviews are offered the place accessible.

Down fee help for medical doctors

There are literally thousands of down payment assistance programs (DPAs) throughout the nation. Nearly all of these are designed to assist decrease–earnings or deprived house consumers obtain their targets of homeownership, so excessive–incomes physicians might not qualify for assist.

However when you want it, you might qualify for a grant, or a low– or zero–curiosity mortgage to assist together with your down fee. And a few loans are forgivable after you’ve spent a sure size of time in residence (main residence within the house, not the hospital).

Additionally take a look at the “Nurse Next Door” program, which is open to medical doctors in addition to nurses, medical workers, and help workers. It presents grants of as much as $6,000 and down fee help of as much as a bit over $10,000.

Downsides of a doctor mortgage

In case you learn across the topic of doctor house loans, you’ll discover some dire warnings. Whether or not they need to hassle you’ll rely in your private circumstances and the lender and program you select.

The next are some issues to look out for.

Potential for increased charges

Since you’re a low–danger borrower, lenders ought to have the ability to give you a decrease charge with out ripping you off. However some might hope you’re higher at medication or surgical procedure than cash.

So be careful for increased charges than regular. It’s possible you’ll discover that some lenders supply seemingly low closing prices by growing your month-to-month mortgage funds over the lifetime of your mortgage.

And think twice about whether or not or not an adjustable mortgage charge fits you.

Many medical doctors profit from these in the event that they know they’ll be shifting to a brand new job in a number of years. And lots of different debtors have saved by adjustable–rate mortgages’ (ARMs’) decrease charges during the last decade or so. However you must be clear they give you the results you want.

Deferring scholar mortgage funds might set you again

There are circumstances through which it is a legit concern. Supposing you’re a brand new physician recent out of medical faculty and your scholar loans are nonetheless of their grace interval.

Many doctor mortgage mortgage applications ignore your scholar mortgage debt. So you can borrow large. However the one approach to carry on high of your month-to-month mortgage funds is to forbear in your scholar mortgage funds throughout your residency.

And which means you’ll be accumulating curiosity on these loans in addition to paying curiosity in your mortgage. This could possibly be costly in the long term.

Purchase now or save an even bigger down fee?

In case you wait till you’ve got a 20% down fee saved, you’ll pay manner much less in curiosity over the lifetime of your mortgage. That’s indeniable.

By the identical logic, when you wait till you’ve saved 100% of the acquisition value, you received’t pay any curiosity. However what you will have paid is a pile of hire.

One consideration ought to play a job in your choice to save lots of up or purchase now. And that’s what’s occurring to house costs within the place you need to purchase.

If actual property costs are rising sharply (and also you suppose they’ll proceed to take action), you might need to purchase as quickly as doable utilizing a low–down–payment mortgage or doctor mortgage program. That manner, you’ll profit from inflation.

But when actual property costs are stagnant or falling, you might achieve little from performing rapidly. It’s worthwhile to weigh your choices. And you may afford to do this at your leisure.

Don’t overlook to comparability store

By all means, take a look at the mortgage lenders providing particular house loans for physicians. However don’t make these lenders your solely choices.

Completely different lenders supply very totally different mortgage charges and offers. And the identical lender can supply considerably higher or worse worth at totally different occasions and to debtors with solely barely totally different profiles.

In case you, as a doctor, are shopping for a dearer house than most, you stand to save lots of much more by charge buying.

Federal regulator the Consumer Financial Protection Bureau (CFPB) reckons, ” … failing to comparability store for a mortgage prices the typical homebuyer roughly $300 per 12 months and plenty of 1000’s of {dollars} over the lifetime of the mortgage.”

And that’s a median. In case you, as a doctor, are shopping for a dearer house than most, your losses stand to be even larger.

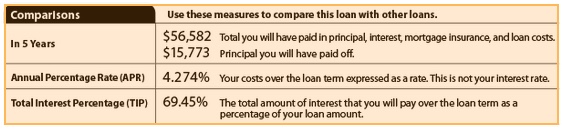

Use your Mortgage Estimates

The simple approach to assess the totally different offers you’re provided is to make aspect–by–aspect comparisons of Loan Estimates from a minimum of 4 totally different lenders. These at the moment are standardized with the identical info and format. So it’s straightforward to check them.

Particularly, take a look at web page three, the place you’ll discover what you’ll have paid after 5 years. Right here’s a pattern, from the CFPB’s web site:

Alternate options to doctor mortgage applications

Simply since you qualify for a seemingly beneficiant program, doesn’t routinely make it your greatest wager.

Typical mortgage loans, accessible to all, might find yourself being your most reasonably priced possibility when rates of interest and charges are tallied up.

Typical and authorities–backed loans

| Typical mortgage (30-year mounted charge) | % (% APR) |

| Typical mortgage (15-year mounted charge) | % (% APR) |

| FHA mortgage (30-year mounted charge) | % (% APR) |

| FHA mortgage (15-year mounted charge) | % (% APR) |

| Va loans (30-year mounted charge) | % (% APR) |

| Va mortgage (15-year mounted charge) | % (% APR) |

*Rates of interest and annual share charges for pattern functions solely. Common charges assume 0% down and a 740 credit score rating. See our full mortgage VA charge assumptions here.

Conforming and jumbo loans

If you have already got your 20% down fee, you’re free to buy any kind of mortgage.

And you might discover that your strong funds and creditworthiness can get you a deal that’s pretty much as good or higher than any provided by physician house loans.

That could be very true when you’re buying within the jumbo loan market – for properties over the conforming mortgage restrict of $. The extra you spend on the house, the extra you’ll pay in curiosity. So that you need to scrutinize your choices additional rigorously.

You’ll want to take into account all of your choices, analysis probably the most promising, and act decisively.

Doctor loans FAQ

Whereas particular mortgage phrases will fluctuate by mortgage program and lender, many mortgage loans, together with doctor loans, haven’t any early–compensation penalty, which implies you may refinance at any level. Refinancing a doctor mortgage right into a decrease charge typical mortgage might make sense as each your earnings and residential fairness enhance and your debt–to–earnings ratio decreases.

Each financial institution could have its personal algorithm and disclosures, however eligible debtors might take out as many doctor loans as they like. Some lenders even permit two doctor loans on the identical time when house owners are shifting from one main residence to a different. Take into account that doctor house loans are typically just for proprietor–occupied properties and never an funding property.

Physician loans are typically not underwritten with a set charge, however you might discover a lender that gives one. You’ll most certainly discover that the majority physician mortgages are adjustable–charge loans, which implies month-to-month mortgage funds will fluctuate over the lifetime of the mortgage.

Charges depend upon a variety of elements, together with the lender and the kind of mortgage. For probably the most half, doctor loans sometimes carry increased charges due to the decrease down fee necessities – or no cash down in any respect – and waived personal mortgage insurance coverage. Mortgage charges change day by day; so charge buying is essential to getting a great deal.

At present’s low charges

Doctor loans could also be a priceless possibility for eligible debtors, however it’s essential to buy your mortgage round to get one of the best deal to your monetary circumstances.

The knowledge contained on The Mortgage Stories web site is for informational functions solely and isn’t an commercial for merchandise provided by Full Beaker. The views and opinions expressed herein are these of the creator and don’t mirror the coverage or place of Full Beaker, its officers, mum or dad, or associates.

[ad_2]

Source link

{kind=link}