[ad_1]

I’ve suggested hundreds of debtors on the Public Service Mortgage Forgiveness (PSLF) program. I began doing this after my spouse had a horrible expertise with FedLoan Servicing. This information goes to point out you my high 40 tricks to maximize your advantages underneath the PSLF program.

I significantly want this listing of 40 suggestions existed again once we made all our errors. Additionally, open our new PSLF calculator up in a brand new tab so you possibly can see how a lot you would personally save.

Notice: The manager motion taken by President Biden October 6, 2021 is extraordinarily necessary for debtors. When you have Direct loans, you’ll want to submit an ECF type via studentaid.gov/pslf. When you have FFEL loans, you’ll want to consolidate first after which submit an ECF type. These actions must be taken by October 31, 2022 to obtain extra credit score in direction of the PSLF program. Moreover, all suspended funds between March 13, 2020 and January 31, 2022 rely in direction of PSLF as properly supplied you had been working at a qualifying non revenue or authorities employer full time.

The place issues went incorrect with PSLF for Us

The very first thing we didn’t know? Apparently, solely the Direct mortgage program loans qualify. Due to this, we misplaced 4 years of credit score whereas she labored in well being care at a not-for-profit hospital. Then, we filed the PSLF type and had her loans transferred to FedLoan Servicing.

Regardless of her funds for over three years on an IDR Plan (Earnings-Primarily based Compensation), half of her loans solely confirmed one month of cost credit score. We ran the numbers and reasonably than combat FedLoan Servicing any longer, we simply determined to refinance student loans and pay them again as quick as doable.

I don’t need anybody else to turn out to be a PSLF program horror story like us. I began Scholar Mortgage Planner® to assist shoppers with enormous pupil debt burdens provide you with a plan to pay again their loans and save each greenback doable all through the method. Try these 40 tips about PSLF to maximise your advantages underneath this system.

Public Service Mortgage Forgiveness – Some ways to economize

Public Service Mortgage Forgiveness program is all the time within the headlines. A pair years in the past, plenty of debtors on the American Bar Affiliation had been retroactively informed they didn’t qualify. The following panic and media protection from this lawsuit impressed me to put in writing this text.

Lately, the media made a ton of noise over the 99% rejection rate of federal pupil mortgage debtors for the PSLF program. Once more, there was panic over media protection with debtors questioning the validity of this system. However right here’s the factor: You should utilize PSLF to your benefit with the suitable methods.

You’ll need to turn out to be an skilled in Public Service Mortgage Forgiveness when you’ve got an obligation of over $50,000 in pupil debt so that you will be totally educated about this selection.

Our PSLF calculator may also help, too. Additionally, take into account listening to episode two of The Scholar Mortgage Planner® Podcast the place I’m going over intimately why this system isn’t damaged, regardless of what many within the media painting.

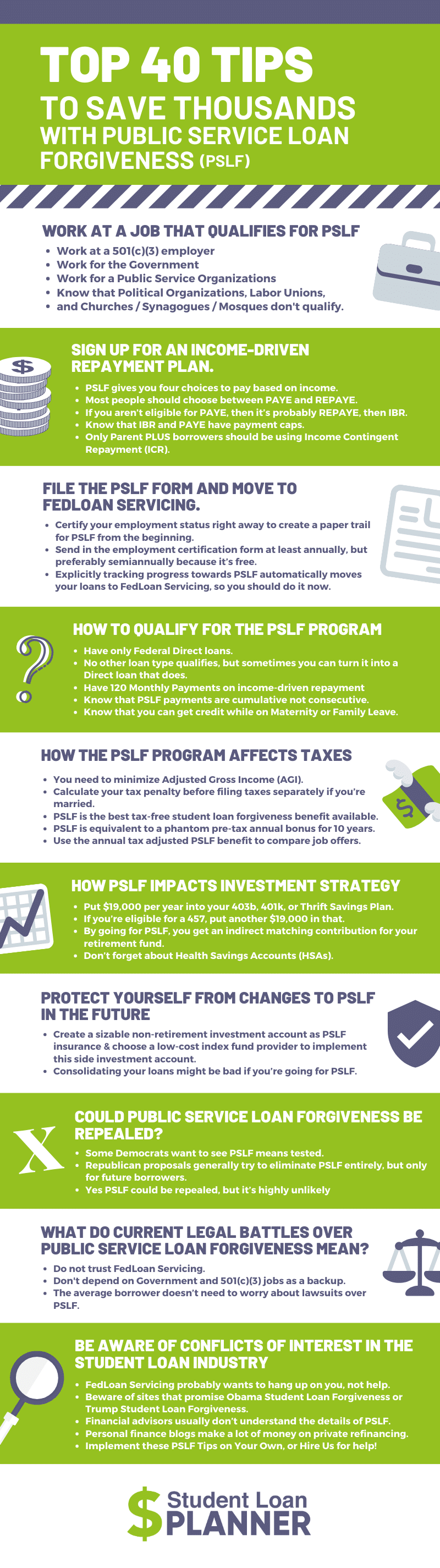

What jobs qualify for Public Service Mortgage Forgiveness?

1. Work at a 501(c)(3) employer? Good

That is the primary type of qualifying Public Service Mortgage Forgiveness job. Most docs and pharmacists qualify for PSLF via working at a 501c3 hospital. The federal government has an obligation to find out eligibility by who your employer is, not what sort of job you do.

A 501(c)(3) is a tax-exempt charity that might obtain a giant test from a wealthy individual who would get to deduct that donation from their taxes.

Assume main educational hospitals, the Crimson Cross, foundations, non-public not for revenue universities, and many others.

You possibly can actually search for in case your employer is a 501(c)(3) on-line by Googling a website like Guidestar with in depth not-for-profit listings.

2. Work for the federal government? Superb

In case you work for an area, state, or federal authorities or authorities company, your work ought to qualify for the PSLF program.

In case you’re an assistant district lawyer, instructor, metropolis worker, professor at a public college, public well being official, and many others., you qualify.

Be sure you really work for the governmental employer immediately and never via an impartial contractor association. Additionally, don’t run for Congress pondering you possibly can reap the benefits of mortgage forgiveness. They explicitly excluded themselves from this profit.

3. Public service organizations – much less sure, and no person is aware of what it means

If I had been depending on the forgiveness of pupil loans for my monetary well being, the one employer I’d work for could be a 501(c)(3) or authorities.

The shape for Public Service Mortgage Forgiveness lists one other class of qualifying employment with a “not for revenue public service group.” It’s unclear why Congress included this class and what they meant by it. Maybe they needed to cowl employers who present service to the general public however are usually not 501(c)(3) or authorities.

There’s massive disagreement over what qualifies proper now. As you may need heard, the American Bar Association sued the Division of Training after their attorneys had been denied. Mainly, the legislation appears open to interpretation right here.

If I owed over $100,000, I’d solely work for an employer that undoubtedly certified for PSLF.

4. Some jobs don’t qualify

There are lots of people doing good work at not for earnings in these classes. Sadly, none of them qualify for Public Service Mortgage Forgiveness.

So in case you’re writing memos on the Republican or Democratic Nationwide Committee or reparing coverage briefs for the AFL-CIO, PSLF doesn’t apply.

Up to now, religion leaders in worship companies had been additionally ineligible for PSLF. Nevertheless, a 2020 policy change has opened the door for religion leaders to turn out to be eligible for PSLF beginning July 1, 2021. Extra particulars are attributable to be launched.

There’s additionally a loophole for folk working for tax-exempt faith-based ministries whose major work isn’t any type of proselytizing. Which means in case you’re the full-time prepare dinner on the Catholic soup kitchen you qualify, however in case you’re the priest, you don’t.

Join an Earnings-Pushed Compensation (IDR) plan

5. PSLF offers you 4 selections to pay primarily based on revenue

Listed here are your 4 compensation choices to qualify for a PSLF program.

All 4 applications ask you to pay a share of your revenue in direction of your pupil loans with a purpose to qualify. This explains why they’re referred to as income-driven repayment (IDR) plans. However don’t fear, we’ll make it easier to with the maths.

The p.c of your revenue required underneath every plan is 15%, 10%, 10%, and 20%.

Calculation primarily based on share of Annual Gross Earnings (AGI) minus 150% of the federal poverty line for your loved ones measurement

- Earnings-Primarily based Compensation (IBR)- 15%

- Pay As You Earn (PAYE)- 10%

- Revised Pay As You Earn (REPAYE)-10%

Calculation primarily based on share of AGI minus 100% of the federal poverty line for your loved ones measurement

- Earnings Contingent Compensation (ICR)- 20%

The proportion you might be requested to pay doesn’t change, irrespective of how excessive the overall steadiness is. Though some cost plans are capped with a most required cost.

For IBR, PAYE, and REPAYE, you get a deduction of 150% of the Federal Poverty Line earlier than they multiply by that respective share to find out the cost.

For ICR, they use 100% of the federal poverty line because the deduction. The one motive to make use of ICR is in case you’re going for PSLF with Parent PLUS loans.

6. Most individuals ought to select between PAYE and REPAYE

PAYE and REPAYE each ask you to pay 10% of your discretionary revenue to your pupil loans. Keep in mind that discretionary income is generally your AGI much less 150% of the poverty line.

In case you’re going for forgiveness, then clearly you need to pay as little as doable to maximise the quantity forgiven.

Selecting between PAYE and REPAYE is dependent upon your marital standing, joint revenue, and the way sure you might be that you just’ll pursue this system.

In case you’re single, unsure you need to do a PSLF program, and don’t make a ton of cash, I’d select REPAYE.

In case you are married, make a considerably totally different revenue out of your partner, and are pretty sure about pursuing Public Service Mortgage Forgiveness for the employment interval of 10 years, I’d select PAYE. Both plan is probably going a great resolution.

7. In case you aren’t eligible for PAYE, then it’s most likely REPAYE, then IBR

Some of us don’t meet PAYE eligibility necessities. In case you had loans earlier than 2007 or didn’t take out any loans after 2011, you then aren’t eligible.

The one motive to select IBR over REPAYE is if you’re married, otherwise you make a really excessive revenue and have already got a number of years of PSLF funds. In that case, it’d make sense to make use of IBR whereas submitting taxes individually or due to the Public Service Mortgage Forgiveness cap in funds.

There are additionally some rare situations for married borrowers dwelling in neighborhood property states equivalent to California and Texas who may be higher off utilizing IBR as a substitute of REPAYE. This is because of equal division of neighborhood revenue on federal returns in neighborhood property states. Nevertheless, most individuals going for PSLF needs to be utilizing PAYE. If that’s not an choice, then go along with REPAYE.

8. Don’t neglect that IBR and PAYE have cost caps even in case you’re a high-income earner

Once more, in case you’re single, unsure you need to do PSLF, and don’t make a ton of cash, I’d suggest selecting REPAYE. In case you are married, make a considerably larger or decrease revenue than your partner, and are pretty sure about pursuing PSLF for 10 years, I’d suggest selecting PAYE. Both plan is probably going a great resolution.

The impacts of incomes extra on an IBR plan

Manner too many excessive revenue professionals make an enormous mistake with PSLF when their incomes improve. They incorrectly consider that they won’t meet eligibility necessities for an revenue primarily based compensation program and refinance.

I’ve seen this value debtors over $400,000 earlier than. In case you’ve already constructed up greater than 5 years of PSLF program credit score, be extraordinarily cautious earlier than refinancing. I’d extremely recommend getting a second opinion earlier than you do one thing irreversible like promote your mortgage to a non-public lender.

Fee caps to pay attention to

IBR and PAYE have a cap equal to the 10-12 months Normal Compensation Plan whenever you entered compensation for the primary time. REPAYE has no cost cap. Therefore, in case your mixed marital revenue is $500,000, however you owe $100,000, you would have a month-to-month cost quantity of round $1,000 on IBR or PAYE however you’d pay greater than 4 instances that underneath REPAYE.

When a decrease revenue partner marries the next revenue partner, you’ll want to watch out not to surrender on Public Service Mortgage Forgiveness when you would reap the benefits of compensation caps.

*Replace on FedLoan errors impacting excessive revenue earners

FedLoan has been messing up recently by sending out letters to high-income debtors telling them they’re not eligible to make funds primarily based on revenue. That causes panic and debtors will name and ask what to do now that they aren’t eligible.

The clueless telephone rep tells them to modify onto one thing else. That may be a mistake.

You by no means get kicked off of IBR or PAYE. You merely have your funds capped. Ignore the letter, and your funds needs to be capped. In the event that they aren’t, then you’ll want to escalate to a supervisor.

9. Nobody besides Guardian PLUS debtors needs to be utilizing Earnings Contingent Compensation (ICR)

This plan is the worst choice for somebody pursuing Public Service Mortgage Forgiveness. Earnings-Contingent Compensation requires you to pay 20% of your revenue with solely a 100% federal poverty line deduction.

Generally ICR exhibits up with the bottom cost on the federal compensation estimator. I can’t actually determine why, since in most each case I’ve seen (and I’ve seen hundreds), ICR exhibits up poorly for these with Direct Loans.

Keep in mind the aim is to pay as little as doable to maximise the mortgage forgiveness profit. If anybody is on ICR, please ship us an e mail at [email protected] and check out switching.

One enormous exception

When you have Guardian Plus loans, then your solely choice to obtain PSLF is to consolidate right into a Direct Consolidation mortgage. After that, you want 10 years of qualifying service whereas on ICR. That plan requires you to pay 20% of your discretionary revenue. Therefore, it most likely solely helps in case you owe greater than $50,000 of Guardian PLUS loans.

Know that when consolidating Guardian PLUS loans, you’ll want to maintain the loans separate from any in your personal title.

There’s an enormous hole within the variety of dad and mom eligible for Public Service Mortgage Forgiveness and people really receiving it. In case you’re working for a authorities or not for revenue employer and have Guardian Plus loans over $50,000, undoubtedly contact me.

I’ve labored with a number of shoppers who had been incorrectly positioned on ICR. Clearly, the folks they used for pupil mortgage assist didn’t know what they had been doing. In case you’re satisfied that ICR is the perfect plan out there and you’ve got Direct loans originated in your title solely, I need to write a weblog submit about you.

Submitting the Public Service Mortgage Forgiveness type and transferring to FedLoan Servicing

10. Certify your employment standing immediately to create a paper path for PSLF from the start

In case you’re going for the PSLF program, you need to get this course of began ASAP:

- Fill out the free Public Service Loan Forgiveness form. That is also called the Employment Certification Type (ECF).

- Ship it in and wait a pair months to listen to again.

- Don’t put this off. There may be every little thing to realize and nothing to lose besides a couple of hours of your time

I’ve heard tales that some mortgage servicers will inform debtors to go away their loans with them for the complete 10 years then apply with FedLoan. That’s horrible recommendation (and constitutes a transparent battle of curiosity).

In spite of everything, servicers solely receives a commission in case you go away your loans with them. If everybody who may qualify for PSLF utilized, the opposite servicers would lose tens of millions in income from servicing charges.

Why you’ll want to transfer to FedLoan ASAP

To offer the servicers the advantage of the doubt, I don’t assume that is some grand revenue hungry technique. I simply assume that almost all telephone reps give unhealthy recommendation generally. Transfer your loans over to FedLoan ASAP in case you plan to get PSLF since they’re the one servicer set as much as monitor PSLF program credit.

Must you simply surrender on Public Service Mortgage Forgiveness as a result of it’s laborious to get? Provided that your hourly wage is above $1,000. In that case, it may be irrational to spend your time coping with FedLoan.

Nevertheless, in case you owe over $50,000 and plan to work in a qualifying job anyway, it’d be a poor resolution to let bureaucratic incompetence get you down. Particularly when of us like us are right here to assist reply your questions within the feedback part beneath.

11. Ship within the employment certification type at the least yearly, however ideally semiannually as a result of it’s free

As soon as you start monitoring your progress in direction of the ten years wanted for pupil mortgage forgiveness, you’ll need an intensive, documented paper path. I anticipate quite a lot of of us could have bother on the finish of their 10-year employment verifying their standing. We lost three years of credit score in direction of PSLF due to FedLoan Servicing. Therefore, I maintain their competence in very low esteem.

To keep away from issues, ship within the ECF yearly on the minimal. FedLoan sucks and the PSLF program type is free, so ship it in each six months to create a stable paper path. It forces the parents monitoring the mortgage program to speak typically with you about your rising progress in direction of the 120 months wanted for mortgage forgiveness.

*Replace: FedLoan now permits you to full and add the Public Service Mortgage Forgiveness certification type on-line. Debtors inform me it’s a vastly higher choice than mailing within the paper type.

12. Explicitly monitoring progress in direction of PSLF mechanically strikes your loans to FedLoan Servicing, so that you may as properly get it over with

Mortgage servicers are fairly unhealthy as a bunch. Sadly, the federal authorities gave a monopoly to FedLoan Servicing for managing accounts for debtors working in direction of Public Service Mortgage Forgiveness. Which means in case you’re pleased together with your mortgage servicer, you’ll lose that whenever you ship in your employment certification type.

The advantages of monitoring your progress towards PSLF sooner outweigh the inconveniences of a barely extra annoying mortgage servicer. No servicer is price having an inaccurate paper path when making use of for PSLF.

How do you qualify for the PSLF program?

13. You must have solely Federal Direct loans if you need them forgiven

In case you work at a qualifying employer however your software for Public Service Mortgage Forgiveness is rejected, the reason being most likely that you’ve got non-qualifying loans.

In case you took out loans in 2010 or earlier, you’ll want to pay further shut consideration to the kind of loans you even have. Most loans after 2010 will probably be made underneath the Federal Direct program. Loans from 2010 or earlier are probably on the previous FFEL program, which doesn’t qualify for PSLF. You possibly can repair this with a mortgage consolidation that converts every little thing right into a Direct Consolidation mortgage. Nevertheless, consolidation loans reset the PSLF cost time clock since legally, it’s a brand new mortgage.

Loans that qualify for forgiveness

There are literally 17 different types of federal pupil loans that qualify for PSLF. Most should be put right into a Direct Consolidation mortgage. Among the ones run via the Division of Well being and Human Providers don’t even present up on the NSLDS database. You must request that they manually get added. In that case, the brand new Direct mortgage would qualify for PSLF.

Right here’s a couple of kinds of loans that may very well be consolidated to fulfill eligibility necessities for PSLF that most individuals miss:

Examples of Well being Sources & Providers Administration loans that don’t present up on NSLDS:

- Nursing Scholar Loans

- Well being Training Help Loans (HEAL)

- Well being Professions Scholar Loans (HPSL)

- Loans for Deprived College students (LDS)

- Main Care Loans

Institutional loans that do present up on NSLDS that should be consolidated for a PSLF program

- Federal Perkins (should be manually included in consolidations)

In case you didn’t know that these loans may very well be made PSLF eligible, you may by chance view them as non-public loans and pay them off after they may very well be forgiven. One of many lifeless giveaways of potential PSLF eligible loans is a flat 5% rate of interest. Heartland ECSI oftens companies many of those type of loans.

One instance I had just lately was a pair with $25,000 of HPSL and $25,000 of Perkins that had been eligible for forgiveness, however provided that they consolidated them into Direct Mortgage standing.

Different doable forgiveness choices

Scholar loans might also be eligible for forgiveness via Total and Permanent Disability (TPD) Program. In case you turn out to be completely disabled whereas repaying your mortgage, your remaining steadiness will be forgiven via this program.

Eligibility necessities and compensation particulars differ from federal to non-public loans, however it’s an choice price contemplating if you end up not in a position to work attributable to disabilities.

Borrower protection to compensation could make you eligible for forgiveness in case you obtained deceptive data by your college. In case your college engaged in fraud or misconduct, you possibly can apply for forgiveness underneath this plan with a web based type.

14. All the things else doesn’t qualify, however generally you possibly can flip it right into a Direct mortgage that does qualify

Federal pupil loans on the Federal Household Training Mortgage program (FFEL) don’t qualify for PSLF. Neither do non-public loans, loans made to you by grandma, Well being Professions loans, Perkins loans, or some other type of mortgage.

When you have a Direct student loan, it’s going to say “Direct” within the title and can qualify for Public Service Mortgage Forgiveness.

If the mortgage description simply says “Stafford Unsubsidized loans” or “Perkins” with out “Direct” in the entrance of the title, it virtually definitely isn’t eligible for Public Service Mortgage Forgiveness.

Keep in mind that consolidation is a treatment for a lot of sorts of ineligible loans. You simply don’t get to hold over any credit score.

15. 120 Qualifying Month-to-month Funds on income-driven compensation, and no you possibly can’t rush it

You want 10 years of credit score in direction of the PSLF program to have all of your debt forgiven tax-free. The extra exact definition is you want 120 months of income-driven funds at a qualifying employer. These 120 qualifying month-to-month funds must be made month-to-month, and you’ll’t make further funds and pace up the clock.

Generally whenever you make further funds, it places your loans into paid ahead status. We regularly must work with of us on this state of affairs, so pay the minimal and no extra.

In 2020, the Trump administration enacted a stimulus invoice, which the Biden administration prolonged in 2021, that suspended funds from March 13, 2020, to January 31, 2022, on qualifying pupil loans. In case you had been working towards forgiveness on the time, the suspended funds will rely towards the 120 you want.

16. PSLF funds are cumulative, not consecutive

Fortunately, the 120 qualifying month-to-month funds don’t have to happen at one employer or consecutively. You would work three years at a not-for-profit then work within the non-public sector for a few years, after which work in authorities for seven years, after which you’d lastly qualify for PSLF. That characteristic encourages mobility of the labor power however solely throughout the non revenue organizations and the federal government sector.

Keep in mind that the PSLF program isn’t a cost plan. REPAYE, PAYE, and IBR are cost plans. You would proceed funds and transfer between part-time and full-time standing, all whereas slowly constructing credit score in direction of the ten years of full-time credit score wanted. In case you don’t find yourself qualifying for Public Service Mortgage Forgiveness, you would get the 20 to 25 12 months IDR forgiveness on the identical cost plan. In fact, in case you’re not doing PSLF, you’ll owe taxes on the forgiven steadiness.

With PSLF, you owe no taxes at forgiveness.

17. You can get credit score whereas on maternity go away or different household go away

Below the phrases of the Public Service Mortgage Forgiveness program, you possibly can take as much as three months of go away out of your job per 12 months. The technical time period is the Household and Medical Depart Act (FMLA). In case you’re taking time away out of your job, ask your HR individual if that qualifies as FMLA go away. If it does, you then’ll need to proceed income-driven funds as it’s going to minimize down the time wanted till your loans are gone. Please don’t use forbearance or deferment.

How the Public Service Mortgage Forgiveness program impacts taxes

18. It’s good to decrease Adjusted Gross Earnings (AGI)

Your income-driven repayments rely upon how a lot cash you make for tax functions. Reduce your taxable revenue with pre-tax contributions to get extra PSLF forgiveness. The best method to do that is to max out all pre-tax accounts. In case you’re married, you can too have you ever partner do the identical. This can decrease your AGI as a joint financial unit. The commonest pre-tax accounts I’m referencing are the 401k and Well being Financial savings Account.

Right here’s an inventory of extra account varieties that cut back your AGI for PSLF:

- 403b

- 401k

- HSA

- 457 (can do along with 403b)

- Solo 401k (for any revenue earned whereas facet hustling)

- Conventional IRA (can normally solely deduct if no retirement plan is obtainable. Can use spousal IRA if partner doesn’t work)

When you have greater than a $3,000 loss on investments, you possibly can write that off towards atypical revenue. There are different write offs as properly out there for actual property investing that I’ve seen debtors make the most of if they’ve facet hustles or different enterprise revenue exterior their most important job.

19. Calculate your tax penalty earlier than submitting taxes individually in case you’re married

When you have a partner with a excessive revenue and little or no pupil loans, you may be tempted to file taxes individually. This topics you to a tax penalty usually. As an alternative of doing this, a borrower may swap to a different income-driven compensation plan. Moreover, they may max their pre-tax accounts. This swap and save technique typically eliminates the necessity to file individually.

Nevertheless, generally filing separately gives you huge savings. Be certain that to run the numbers your self or rent somebody like us to determine if it’s price it.

When you have loans and your partner doesn’t, submitting separate may prevent vital cash. Nevertheless, it’s best to virtually by no means file taxes individually in case you each have vital federal pupil loans. I need to make an observation that probably the most frequent and costly errors we see is debtors submitting with the incorrect tax standing as married {couples}.

That’s considered one of our robust fits helps you resolve what submitting standing is greatest to your pupil loans. Your CPA is more likely to be clueless about this. We’ll provide the precise information and inquiries to ask so you possibly can determine which selection is healthier. In some instances, you possibly can even amend returns to get a reimbursement in case you made a submitting mistake. We’ll warn you if we expect that’s one thing you’ll want to discuss together with your CPA.

20. Public Service Mortgage Forgiveness is the best tax-free pupil mortgage forgiveness profit out there at this time

Keep in mind that not like non-public sector IDR pupil mortgage forgiveness, the PSLF program is a tax-free profit. Non-public sector staff with massive loans should save for the long run tax penalty. In distinction, not-for-profit or authorities staff don’t must cowl this further value.

Many debtors love the concept of working for 10 years and being completely completed with out the fear of a giant lump sum cost to the IRS. I sympathize.

You want a PSLF facet account the place you place cash right into a brokerage. That’s to be sure you have asset progress when you’re ready round for mortgage forgiveness. Nevertheless, you very probably will get to maintain this cash when you obtain PSLF.

21. PSLF program is equal to a phantom pre-tax annual bonus for 10 years

When you have $250,000 in med college loans and would pay again $300,000 with non-public lender refinancing, however solely $100,000 with PSLF, then that’s a $200,000 profit over 10 years. Regulate this profit for taxes at a excessive marginal fee equivalent to 40%. After the adjustment, you’ve saved over $330,000 in pre-tax compensation over that 10 12 months interval, or $33,000 per 12 months.

It is best to add this pre tax wage equal to any compensation you earn for a qualifying job to check it to a place within the non-public sector. For instance, within the case above in case you earned $200,000 at a 501c3 hospital, you’d add $33,000. That $233,000 wage is what you’d have to earn within the non-public sector only for these two jobs to be equal financially.

In lots of instances, the non revenue or authorities job has higher hours and/or advantages. So that you may have to earn considerably extra within the non-public sector to make the 2 jobs at a break even degree.

22. Use the annual tax adjusted Public Service Mortgage Forgiveness profit to check job presents

When evaluating alternatives in the private and non-private sector, it’s necessary to regulate for the oblique PSLF program bonus for taxes so you possibly can evaluate job presents. Take a med pupil with the $330,000 pre-tax Public Service Mortgage Forgiveness bonus from tip #21. That’s price $33,000 per 12 months over 10 years. Add the yearly worth of PSLF into annual wage earlier than evaluating them to their non-public sector counterparts.

For decrease incomes jobs, I discover the bonus can generally be higher than a borrower’s total wage. Clearly PSLF is essential in that case. For higher-earning positions like Large Legislation associates or excessive incomes medical specialties, you’re typically higher giving up the PSLF program for higher revenue and refinancing with non-public lenders.

After serving to hundreds of debtors, I’ve discovered Public Service Mortgage Forgiveness isn’t ok to pursue a public service job except you’d do this anyway. Debtors and not using a ardour for public service ought to work in the next paying position to maximise their revenue.

How PSLF impacts funding technique

23. Put $19,500 per 12 months into your 403b, 401k, or Thrift Financial savings Plan

In case you’re an worker, max out your conventional pre-tax retirement account. The present max for 2021 is $19,500. For many public sector or not for revenue staff, you’ll use a 403b. For federal staff, the Thrift Financial savings Plan (TSP) is the account to make use of. Generally you may even have a 401k and nonetheless be in a qualifying job.

I recommend selecting index funds with rock-bottom bills of 0.2% per 12 months or much less. Take into account placing in 120 minus your age in inventory index funds and the remaining in a bond index fund. So in case you’re 30, you’d put 90% in shares and 10% in bonds. For the inventory funds, I’d recommend a 50/50 break up between one thing like US Whole Inventory Index Fund and Worldwide Whole Inventory Index Fund. Two Vanguard funds that correspond to those choices are VTSAX and VTIAX.

When you have an choice like a goal retirement fund, I’d maintain issues easy and simply go along with that.

24. In case you’re eligible for a 457, put one other $19,500 in that:

I’ve had shoppers who labored as staff at a state or municipal employer or hospital system that had each a 457 and a 403b. In that case, you possibly can put as much as $19,500 per 12 months in each accounts. That’s a max of $39,000 in pre-tax revenue you possibly can take away out of your AGI. That quantities to $3,900 in financial savings per 12 months for these pursuing Public Service Mortgage Forgiveness utilizing PAYE or REPAYE.

In case your partner has entry to a 403b and 457, you would have her or him max their account as properly. That’ll prevent cash in case you file collectively.

The best sum of money you possibly can put into pretax investments as an worker married to a different worker with the identical eligibility is $39,000 instances 2 + $7,000 to your well being financial savings account. Actually in case you can afford to contribute $84,000 a 12 months pre tax, you may be very properly off sooner or later.

In case you don’t have entry to all these accounts, don’t sweat. Concentrate on maxing what you possibly can and placing the surplus in a brokerage account for basic functions.

25. By going for PSLF, you get an oblique matching contribution to your retirement

Most individuals save of their retirement accounts as a result of they obtain an employer match. Nevertheless, that match doesn’t go any larger in the event that they select to contribute extra. In distinction, the Public Service Mortgage Forgiveness match is 10 cents on each $1 of contributions all the way in which as much as the utmost.

What I imply is that these contributions cut back your taxable revenue, which reduces the required Public Service Mortgage Forgiveness funds since REPAYE, IBR, and PAYE require much less in month-to-month funds with decrease taxable revenue. The federal government doesn’t immediately contribute cash to your retirement account in case you contribute the max pre-tax quantity. Relatively, it simply takes much less out of your pocket in obligatory pupil mortgage funds.

26. Don’t neglect about Well being Financial savings Accounts (HSAs)

They’ll additionally cut back AGI: In case you’re single, you possibly can contribute $3,500 to an HSA. Married folks can contribute $7,000 to the household HSA. If there aren’t already sufficient causes to like a triple tax-exempt account like an HSA, you additionally obtain an oblique match from the federal authorities of 10 cents for each greenback contributed. To make the maths simple, say you place in $5,000 to an HSA for your loved ones and your revenue after changes for the federal poverty line is $100,000.

PAYE or REPAYE would require yearly funds of $10,000 in direction of your federal pupil loans. After saving $5,000 in an HSA, your revenue is $95,000 and it’s important to pay $9,500 in your pupil loans. Since you ultimately get forgiveness tax-free, this steadiness doesn’t matter so HSAs are pure financial savings.

This may be one of many coolest and most neglected areas the place somebody going for Public Service Mortgage Forgiveness can lower your expenses.

Shield Your self from Modifications to Public Service Mortgage Forgiveness within the Future

27. Create a large non-retirement funding account as PSLF insurance coverage

Even those that categorical doubt in regards to the PSLF program should acknowledge the massive probability that this system won’t be repealed for many who presently have excellent pupil debt. Which means you shouldn’t be paying further for loans that may be forgiven.

Nevertheless, many purchasers of mine categorical deep concern about carrying six figures of debt. They fear this burden may ultimately come again to hang-out them. You possibly can remedy this fear.

Place these financial savings in a taxable mutual fund or brokerage account. Over time you’ll construct financial savings at a quicker fee than inflation. Assume for a second Public Service Mortgage Forgiveness repeal does occur. You’d be capable to money within the financial savings and begin paying down the debt aggressively.

28. Select a low-cost index fund supplier to implement this facet funding account

Be certain that your funding account fees lower than 0.5% per 12 months in complete charges for funding bills and recommendation. Low charges have a robust wealth-building impact.

I recommend Vanguard for do-it-yourself buyers. Most Vanguard buyers pay between 0.05% and 0.2% per 12 months in charges (I get $0 in case you click on on that hyperlink and arrange an account).

For people who need refined portfolio and funding administration and don’t like the concept of investing themselves, I recommend Betterment (referral hyperlink). In case you arrange an account via that hyperlink, you get a month to 1 12 months managed free.

Most Betterment prospects can pay between 0.25% to 0.40% per 12 months complete. Since they use largely Vanguard funds, their payment is actually 0.25% per 12 months over the price of Vanguard.

Select the suitable investing account for you

It actually comes right down to how a lot you need to be concerned in managing your investments. Each locations will go away you hundreds of {dollars} richer in the long run in comparison with going with a typical funding firm that fees at the least 5 instances extra.

Realistically, 0.25% of a small sum of money is a really small payment. You would attempt them out to learn the way they make investments after which cancel sooner or later in case you resolve you realize sufficient to handle your personal investments.

29. Consolidating your loans may very well be a harmful step in case you’re going for PSLF

There are a ton of fly-by-night pupil mortgage consolidation factories and even legislation companies on the web that cost gobs of cash to finish pupil mortgage consolidation kinds as their one-size-fits-all resolution. That may very well be a horrible resolution. Present loans have Public Service Mortgage Forgiveness within the promissory be aware. There are two causes somebody going for the PSLF program ought to consolidate their loans.

- You will have non-Direct loans that don’t qualify for PSLF. These non-Direct loans embrace FFEL, Well being Professions, Perkins loans, and a few others.

- If debtors need to begin qualifying PSLF funds quicker, they may consolidate proper after commencement. By consolidating the day after you graduate, you possibly can shorten the traditional grace interval.

Don’t consolidate loans for which you’ve already made PSLF qualifying funds.

Doing this can remove any present progress in direction of forgiveness.

Might Public Service Mortgage Forgiveness be repealed?

30. Some Democrats need to see PSLF means examined

That is the only most practical menace to this system’s use by present debtors. That is very true for people with six-figure pupil debt burdens. President Obama proposed a $57,500 Public Service Mortgage Forgiveness cap in 2015 as a max profit. That was roughly the max quantity an undergrad may borrow on the time.

The administration responded to the disproportionate profit that the PSLF program supplies to high-income earners. In fact, that proposal didn’t move attributable to opposition from Congressional Democrats.

Nevertheless, I’d count on means testing to return again into the dialog ultimately, however just for future debtors. The first menace for folks utilizing PSLF is means testing, not repeal. If a $300,000 borrower doesn’t obtain tax-free pupil mortgage forgiveness in 10 years, that’s most likely going to be the rationale.

To be clear, I feel the danger of that’s 5% to 10%, since Public Service Mortgage Forgiveness has proven that it has bipartisan assist.

31. Republican proposals typically attempt to remove PSLF completely, however just for future debtors

People who don’t presently have loans excellent are all the time in peril of not having PSLF as an choice. When you begin a graduate program although, you need to be allowed to proceed borrowing loans that will probably be eligible for PSLF as long as your promissory be aware contains point out of this system.

With break up management of White Home and Congress, it’s anyone’s guess as to what’s going to occur with the following spherical of pupil mortgage reform.

Grad college students simply beginning their applications in fall 2020 may need some professional worries, however will most likely be protected. Debtors with present loans and people about to complete college have little or no to fret about. Any Republican plan for repeal ought to grandfather them right into a PSLF program.

Replace on tried laws

The Republicans have tried to move the PROSPER ACT, which might eliminate PSLF. It could grandfather in anybody who’s already graduated or enrolled at school on that date. That program is successfully lifeless.

Home Democrats tried to pass The Aim Higher Act, which might defend and develop PSLF for future generations. That proposal is simply a gap salvo.

Senator Lamar Alexander chairs the Senate HELP Committee answerable for pupil loans. I’d count on he and future chairs will defend this system and that the ultimate compromise laws will look much more just like the Goal Greater Act as a substitute of the PROSPER Act.

32. Sure PSLF may very well be repealed, however it’s extremely unlikely

Might the PSLF program be repealed? Sure, it may. Nevertheless, Public Service Mortgage Forgiveness has a various and highly effective set of backers. We now have the absurdly excessive value of grad college to thank for that. Due to this fact, the possibility that present debtors who have already got loans don’t obtain PSLF in any respect is unlikely. That is primarily attributable to political causes.

There would even be an enormous variety of lawsuits. There’s an excellent argument that PSLF is a contract between debtors and the federal authorities that may’t be damaged.

The PSLF program will trigger labor market distortions which are but to be realized. It additionally creates an enormous disparity between non-public and public sector staff. For these causes, I do count on that the PSLF program’s days are numbered. Nevertheless, I’d put the chances that present debtors don’t obtain the complete profit at 10% or much less. That quantity contains the danger posed by means testing PSLF.

What do present authorized Battles over Public Service Mortgage Forgiveness imply?

33. Don’t belief FedLoan Servicing

The Division of Training actually harm some attorneys on the American Bar Affiliation after they overruled FedLoan Servicing that the ABA certified for mortgage forgiveness. The attorneys misplaced two to 5 years of credit score in direction of Public Service Mortgage Forgiveness due to the error. These attorneys are presently suing FedLoans, arguing that FedLoan rulings needs to be binding as an agent of the federal authorities.

Whatever the outcomes of that swimsuit, you clearly should not trust FedLoan Servicing. Confirm your personal standing your self for Public Service Mortgage Forgiveness and be sure you’re taking the suitable steps.

Replace: The lawsuit resulted in a judgment by the DC court docket of appeals that the federal government and FedLoan acted in an “arbitrary and capricious method.” Three of the 4 affected debtors will most likely get credit score for his or her PSLF service. Additional proof as to how sturdy this program is.

34. Pay attention to authorities and 501(c)(3) job openings as a backup employment plan

As I discussed earlier, the Public Service Mortgage Forgiveness employment certification type explicitly lists all 501(c)(3) organizations and native, state, and federal authorities employers as qualifying for the PSLF program.

In case you’re working at a not-for-profit employer that’s not the federal government or a 501(c)(3), maintain monitor of doable job openings in case FedLoan Servicing pulls the rug out from underneath you and voids your progress in direction of PSLF.

35. The typical borrower doesn’t want to fret about lawsuits over PSLF

The media likes to blow issues out of proportion. That’s precisely what occurred for my part over the newest string of PSLF program lawsuits. Take note of the coverage that issues, like whether or not present debtors will probably be grandfathered in or if the federal government will impose a means-test on the PSLF profit.

Comply with the ideas on this article. In case you do, fear rather a lot much less about what the media says.

Right here’s a couple of tales I’ve seen trigger large numbers of hysteria laden emails to be despatched to my inbox over the previous few years:

- “Authorities Lies About PSLF Eligibility for Public Curiosity Attorneys”

- “PSLF Has 99% Rejection Price”

- “New Republican Proposal Would Repeal PSLF”

Is there any marvel debtors don’t belief this program? Ignore the noise and keep centered.

Bear in mind of conflicts of curiosity within the pupil mortgage business

36. FedLoan Servicing most likely desires to hold up on you, not assist

The federal authorities gave FedLoan Servicing the unique rights to handle the PSLF program borrower accounts, in order that they don’t have any incentive that can assist you. Put yourselves within the footwear of their executives. They earn a flat payment with no penalty for poor efficiency and no bonus for nice customer support. Therefore, FedLoan desires to maintain staffing prices down at their name heart.

Therefore, brief telephone calls imply decrease prices and extra revenue. Don’t ever let a rep from a pupil mortgage servicer rush you off the telephone. Moreover, if somebody offers you odd data, name again. Converse to as many reps as you’ll want to till you discover one which sounds competent.

If you’ll want to attraction your cost rely, know that it’ll take at the least six months. Name again semiannually to trace progress, and know that your rely must be right whenever you’re lastly eligible, not at this time. Which means it’s not price shedding sleep over.

I just lately found a secret telephone quantity there that it’s best to name in case you’re having a ton of bother: (717) 720-7605. A few of my readers who’ve used that FedLoan telephone quantity as a substitute of the generic one report getting their issues mounted in days as a substitute of months.

37. Beware of web sites that promise Obama pupil mortgage forgiveness or Trump pupil mortgage forgiveness.

There are a ton of web sites and corporations within the pupil mortgage world that simply need your cash. In case you discover a vaguely federal authorities trying web site with phrases “doc preparation service” and overvalued language about Trump or Obama Mortgage Forgiveness, don’t work with them.

These of us sport the system to rank for prime search quantity key phrases. They rent folks off Craigslist and pay steep commissions, and their reply for each downside is pupil mortgage consolidation.

I’ve seen folks lose over $80,000 when loans acquired consolidated that already had eligibility for forgiveness.

Furthermore, the payment for this service is ceaselessly over $1,000. Essentially the most we cost is $595, and we really create a customized plan. The truth is, we don’t even do any doc preparation as a result of it’s simple to do by yourself and that’s not the place worth creation occurs. That comes from having a transparent plan supplied by a CFA or CFP® skilled.

There are respected corporations and web sites on the market that cost far decrease, clear charges. Moreover, they assist optimize federal pupil loans with a rigorous, custom-made evaluation. (Hopefully, after studying this, you are feeling that method about Scholar Mortgage Planner®). Don’t pay two to 10 instances as a lot cash for a junk service.

38. Monetary advisors normally don’t perceive the main points of Public Service Mortgage Forgiveness

There are some exceptions to this rule, equivalent to fiduciary Registered Funding Advisors who focus on particular professions. Nevertheless, as a basic rule, financials advisors don’t know the intricate details of how these mortgage forgiveness applications work. A very good advisor ought to admit what they don’t know. She or he would steer you to sources that may make it easier to.

If the advisor doesn’t know methods to mannequin tax submitting methods and clarify what your month-to-month cost will probably be, then you’ll want to look elsewhere for help. Monetary advisors are generalists. Even the extremely educated ones may make 5 pupil mortgage plans in a month. We simply do greater than twenty instances that.

“Price solely fiduciary” doesn’t imply skilled recommendation in all areas. Working with us, you’ll most likely pay rather a lot much less and get higher recommendation as a result of all we cope with is pupil mortgage debt.

39. Private finance blogs make some huge cash on non-public refinancing

Private finance blogs make a ton of money from referral bonuses when folks refinance their larger training pupil loans via affiliate hyperlinks. That features this website. Nevertheless, we give a majority of our fee again to the borrower with money again bonuses between $300 to $1,275. I would like Scholar Mortgage Planner® to be often called having the very best degree of integrity in the complete pupil mortgage universe.

Don’t refinance in case you qualify for the PSLF program. You’ll completely lose that choice. Fortunately, I’ve a enterprise case for going into excessive element about PSLF. In spite of everything, I consult with borrowers on methods to maximize the worth of this system.

Nevertheless, different web sites take a hands-off strategy. Their sole income supply is from refinancing partnerships.

Even when they’re moral, they’ll all the time have an unconscious bias in direction of non-public refinancing lenders. In case you’re on monitor for Public Service Mortgage Forgiveness, you’ll lose that profit eternally in case you refinance just because a buddy stated it’s best to do it, otherwise you noticed the Superbowl advert. Assume earlier than you click on.

40. Implement these Public Service Mortgage Forgiveness suggestions by yourself, or rent us for pupil mortgage assist

You’ve made it to the tip of my high 40 suggestions. Clearly, you’re going to be in much better form than your friends. Many will save hundreds of {dollars} from the following pointers.

Name FedLoan Servicing now and implement these greatest practices immediately. In case you’ve benefited tremendously from this text, please share this submit with a buddy or remark with questions beneath.

Possibly you skimmed this and are overwhelmed with the main points, otherwise you’d reasonably rent any individual to research your loans for you. We’ve suggested hundreds of debtors such as you. There’s a great probability I’ll catch one thing that even probably the most diligent individual may miss. Learn how to hire us and let’s see how a lot cash we may save in your pupil loans.

Tell us your questions, we’re right here to assist

In case you simply need to share what you’re going via, use the contact button or feedback part beneath and let me know your considerations. I based Scholar Mortgage Planner® to make your life simpler, prevent extra money, and offer you again hours of time which may’ve wasted worrying about methods to pay again your pupil loans.

If you’d like our strongest PSLF calculator, enter your title and e mail beneath and we’ll ship you over a duplicate you possibly can obtain and use.

[ad_2]

Source link

{kind=link}