[ad_1]

Does refinancing all the time begin your mortgage over?

The quick reply is, sure. If you refinance, you’re changing your previous mortgage with a model new one. Which means you successfully begin the mortgage over.

However it’s nonetheless attainable to refinance with out restarting your mortgage time period at 30 years.

With a little bit little bit of savvy, you may reap the benefits of immediately’s historic low mortgage rates and shorten the variety of years remaining in your mortgage.

Listed below are a number of choices to contemplate to refinance your mortgage with out beginning over.

Verify your refinance eligibility. Start here. (Nov 12th, 2021)

On this article (Skip to…)

Refinance with out extending your mortgage

As a home-owner, your mortgage is your alternative. There’s no rule that claims you have to make use of a 30-year fixed-rate mortgage.

And in the event you do select a 30-year mortgage, you’re not obligated to maintain it the complete time period.

You’re free to refinance or use different methods to shorten your reimbursement interval — and save quite a bit on curiosity funds.

That stated, lenders additionally received’t customise the time period to go well with the borrower. So you could not discover a new mortgage with the identical finish date as your prior mortgage.

For instance, let’s say you locked in a 30-year mortgage that’s now 5 ½ years previous and also you’d prefer to refinance for a greater charge. You’ll be able to’t get a brand new mortgage for twenty-four ½ years to line up together with your unique 30 12 months mortgage. Because of this truth, you’ll both have to increase your mortgage time period or change to a brand new, shorter time period if you refinance.

Fortunately, there are many mortgage phrases out there underneath 30 years, so it’s normally attainable to refinance with out beginning utterly over.

Refinance to a shorter mortgage time period

Essentially the most simple method is refinancing your mortgage right into a shorter mortgage time period and thus dashing up amoritization.

In case your starting mortgage was a 30-year mortgage, for instance, you may refinance right into a mortgage lasting 20 years or 15 years as a substitute.

Decreasing the variety of years in your mortgage will “speed up” your amortization, and pay your mortgage off faster.

For instance, say your present mortgage stability is $300,000.

- Your present mortgage has a 30-year time period and 4.0% rate of interest

- You refinance right into a 15-year time period with a 2.5% rate of interest

- Your month-to-month principal and curiosity fee goes from $1,432 to $2000

- That’s an additional $568 per thirty days

- However you save $257,760 in complete curiosity funds

Funds on a 10-, 15-, or 20-year mortgage are all the time larger than funds on a 30-year mortgage.

However immediately’s refinance charges are so low that funds for a shorter mortgage time period have grow to be rather more reasonably priced than in earlier years.

So earlier than you dismiss the thought of a refinance to a shorter time period, try what your fee could be at immediately’s charges and see if it is sensible for you.

Verify your refinance eligibility. Start here. (Nov 12th, 2021)

Prepay your mortgage as a substitute of refinancing

For a lot of householders, the upper month-to-month price of a shorter mortgage time period isn’t within the finances.

That is why some householders skip the refinance and choose to “prepay” their mortgage as a substitute. You don’t get entry to new, decrease charges, however you’re taking higher management of your mortgage.

Prepaying your mortgage means to ship “further” funds to your lender every month, which chips away on the quantity you owe sooner than your amortization schedule prescribes.

For instance:

- In case your mortgage fee is $1,750 per thirty days;

- And also you ship $2,000 to your lender every month as a substitute;

- You cut back the quantity owed in your mortgage by $250 each month. This may trigger your mortgage to achieve its “finish date” sooner.

The extra you prepay, the more cash you’ll save.

The best choice: “Refinance-to-prepay” in your mortgage

There’s a 3rd approach to cut back your mortgage curiosity and shorten your mortgage time period. It’s referred to as “refinance-to-prepay”.

Refinance-to-prepay is strictly what it seems like — you refinance your mortgage to a decrease charge, then prepay (make further funds) in your new mortgage.

With refinance-to-prepay, you get entry to present mortgage charges, and a faster amortization schedule.

Right here’s the way to execute this technique:

- Refinance to a decrease charge in your similar mortgage program (e.g. 30-year fastened)

- This may end in a decrease month-to-month fee

- Apply your complete month-to-month financial savings to your new mortgage month-to-month as “further fee”

- Hold doing this till your mortgage is paid in full

The refinance-to-prepay system works as a result of, though your mortgage charge is decrease, you’re making the identical fee to the financial institution every month.

You’re paying much less curiosity due to your decrease charge and you’re sending bonus principal month-to-month.

If you refinance-to-prepay, your mortgage will “restart” to 30 years, however you’ll in the end pay it off sooner than had you by no means refinanced in any respect.

Right here’s a real-life instance of how refinance-to-prepay works.

- Your present mortgage stability is $400,000

- You refinance from the 75% mortgage charge you took two years in the past, to a zero-closing price 2.75% mortgage charge

- After the refinance, your fee shall be about $220 much less per thirty days

Merely take these $220 financial savings and ship it to your lender every month alongside together with your common fee.

Should you stick with it, your new 30-year mortgage will repay in 25 years.

That is 3 years sooner than in the event you hadn’t refinanced in any respect (because you had been already two years into your mortgage time period).

And people 5 years of creating “no funds” prevent about $54,000 in curiosity.

Even with closing prices, the maths works out. You’re spending a little bit, and saving quite a bit.

Verify your refinance eligibility. Start here. (Nov 12th, 2021)

In want of funds: Money-out refinance

It’s not secret actual property costs have been going up.

If you wish to faucet into the house fairness you’ve amassed lately to fund a rework or to repay excessive APR bank card debt, then a cash-out refinance mortgage could also be an excellent choice to pursue.

A cash-out refinance replaces your present residence mortgage with a bigger one, providing you with the surplus money to finish your goal.

Relying on how a lot rates of interest have modified since your prior mortgage, a cash-out refinance could not essentially add to your month-to-month mortgage funds.

Understanding your mortgage reimbursement schedule

Should you’ve ever checked out your mortgage assertion after a couple of years and thought, “I haven’t paid this factor down a bit!”, you’re witnessing the consequences of amortization.

Amortization is the fee schedule by which your mortgage stability goes from its beginning stability to $0 over time.

The scale of your principal and curiosity parts change every month primarily based on this schedule. And sadly, amortization all the time favors the financial institution.

Which means the early years of a mortgage require giant curiosity funds, and embrace little or no mortgage payback.

Solely when you’ve held the mortgage a considerable period of time do you begin paying extra towards your stability every month than towards curiosity.

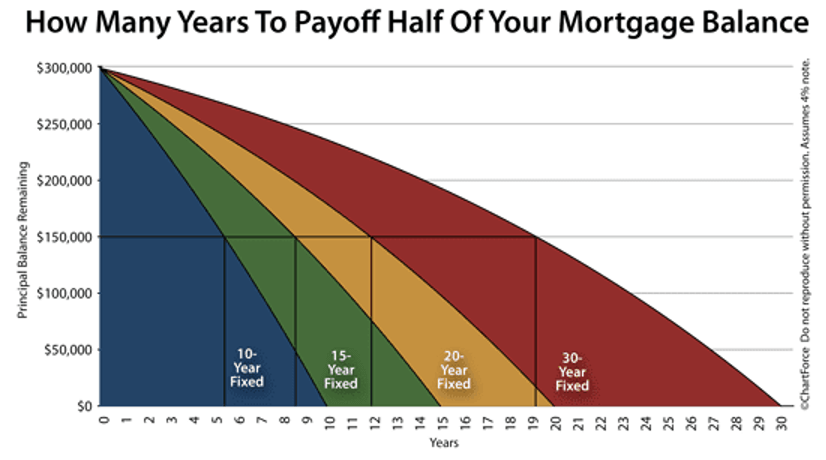

For instance: Should you had been to borrow $300,000 from the financial institution at a mortgage charge of 4 %, after 10 years, right here is how a lot you’ll nonetheless owe:

- A 15-year mortgage would have $119,000 remaining, or 40% of the unique mortgage

- A 20-year mortgage would have $180,000 remaining, or 60% of the unique mortgage

- A 30-year mortgage would have $235,000 remaining, or 78% of the unique mortgage

With the 15-year residence mortgage, your mortgage is greater than midway paid. With the 30-year mortgage, you’ve barely made a dent.

This is without doubt one of the the explanation why householders are more and more favoring 15-year refinances over 30-year ones.

Fortunately, immediately’s charges are low sufficient to make 15-year mortgages accessible for a lot of householders who couldn’t afford them earlier than.

And, even when a refinance doesn’t make sense for you, you may take your amortization schedule into your personal fingers by prepaying in your mortgage. This cuts down in your mortgage time period and might result in massive curiosity financial savings in the long term.

Immediately’s refinance charges

Refinance charges are at historic lows.

There are hundreds of thousands of U.S. householders with mortgages “within the cash.” Should you refinance, you might be able to do it with out extending your mortgage. And you can save your self tens of hundreds in the long term.

Examine immediately’s charges to see what you can save.

[ad_2]

Source link

{kind=link}