![Should You Care About Types of Credit? [Infographic]](https://198businesscreditnews.com/wp-content/uploads/2022/05/credit-mix-200.png)

[ad_1]

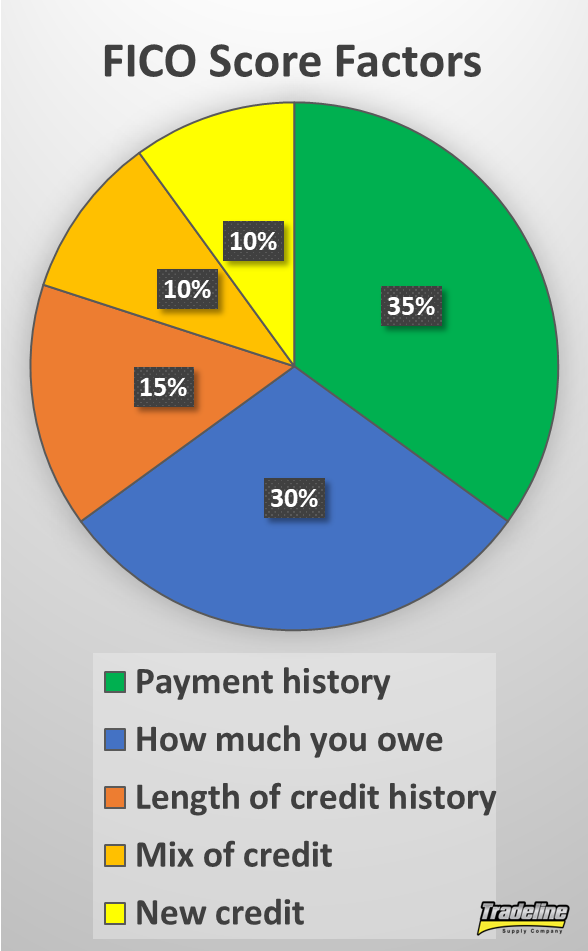

Credit score combine, additionally referred to as mixture of credit score, is likely one of the elements that your credit score rating takes into consideration. It is likely one of the least vital elements, weighing in at 10% of a FICO rating.

Nevertheless, it’s nonetheless vital to contemplate when constructing credit score, particularly if you wish to get the absolute best credit score rating.

Try our infographic on credit score combine and kinds of credit score, then get all the main points within the article beneath.

![Credit Mix - Types of Credit Accounts [Infographic]](https://tradelinesupply.com/wp-content/uploads/2020/02/Credit-Mix-Types-of-Credit-Accounts-final.jpg)

Credit score combine is comprised of 4 kinds of credit score: revolving credit score, cost playing cards, service credit score, and installment credit score.

What Is “Credit score Combine” or “Mixture of Credit score”?

Mixture of credit score contains 10% of a FICO rating.

Your credit score combine is the range of kinds of credit score accounts in your credit score report.

Having various kinds of credit score accounts in good standing in your credit score file demonstrates that you should use credit score responsibly. Lenders ideally wish to see that you’ve efficiently managed quite a lot of kinds of accounts.

Forms of Credit score Accounts

Relying on the way you outline the categories, there are 3-4 basic classes in relation to kinds of credit score.

In line with Experian, there are 4 kinds of credit score:

Revolving credit score is a type of credit score with which you’ll be able to “revolve” or carry a stability from month to month. You’re assigned a credit score restrict that you could cost as much as and also you make a fee every month. Curiosity will sometimes be charged in the event you carry a stability from month to month. Bank cards and features of credit score are the commonest kinds of revolving credit score accounts.

Cost playing cards are much like bank cards, besides the stability should be paid in full on the finish of each billing cycle. Since you don’t revolve a stability from month to month, you don’t pay any curiosity, however you often must pay an annual charge.

Cost playing cards shouldn’t have pre-set credit score limits, so the “credit score restrict” that reveals up in your credit score report is definitely the best quantity you’ve ever spent on the cardboard. Additionally, not all companies settle for cost playing cards, in distinction to bank cards, that are accepted at most companies.

Service credit score consists of accounts along with your service suppliers, akin to utilities, cellular phone service, and so forth. These are thought of credit score accounts as a result of the service is supplied earlier than you pay the invoice.

Accounts along with your utility suppliers are thought of service credit score.

Usually, service suppliers don’t report your fee historical past to the credit score bureaus, so the one time these accounts will have an effect on your credit score is in the event you default on a contract along with your service supplier and the account goes into collections. Nevertheless, new “different information” credit score scoring fashions are starting to include utility funds to be able to toughen those that could also be credit score invisible.

Installment credit score refers to a mortgage of a certain quantity that you simply pay again in common, mounted funds over a sure time period. Forms of installment loans embody automobile loans, mortgages, pupil loans, and so forth. Rates of interest on installment loans are sometimes—however not all the time—decrease than bank card rates of interest.

Examples of Revolving Credit score

As we touched on above, the 2 commonest kinds of revolving credit score are bank cards and features of credit score.

- Bank cards embody these issued by banks akin to Capital One, Financial institution of America, and Chase, in addition to retail retailer playing cards, which might sometimes solely be used at a specific retailer.

- Strains of credit score are much like bank cards in that you’ve entry to a set sum of money—your credit score restrict—that you could draw from. After you borrow cash out of your line of credit score, the stability begins accruing curiosity, and while you pay it again, that credit score is then obtainable once more so that you can use. That is why it’s thought of revolving credit score: you should use it many times so long as you retain paying it again.

A house fairness line of credit score (HELOC) is a revolving account that’s secured by your property.

Forms of Strains of Credit score

Strains of credit score could be both secured, which implies the borrower has supplied collateral to again the road of credit score in case of default, or unsecured, which means no collateral is required.

Past these basic classes, there are three major kinds of traces of credit score.

- A residence fairness line of credit score (HELOC) is a line of credit score secured by your fairness in your house, which is the distinction between the worth of your property and the quantity you continue to owe in your mortgage. Since your property fairness serves as collateral, in the event you default on a HELOC, you possibly can threat dropping your property to foreclosures.

- A private line of credit score is often unsecured, though typically you might be able to present collateral within the type of financial savings or investments.

- A enterprise line of credit score could also be secured or unsecured. They’re supplied by monetary establishments in addition to many business distributors.

Examples of Installment Loans

Forms of installment credit score embody:

- Auto loans

An auto mortgage is one kind of installment account.

- Mortgages

- Scholar loans

- Private loans

- Credit score-builder loans

- Residence fairness loans (to not be confused with a HELOC, which falls below revolving credit score)

The breakdown of account sorts outlined above is a simplified model of how credit score scoring methods truly categorize various kinds of accounts. In actuality, credit score scoring fashions might contemplate as many as 75+ account sorts.

As well as, every kind of account might have a special impact in your credit score.

How Does Credit score Combine Have an effect on Your FICO Rating?

As we talked about on the high of this text, credit score combine makes up about 10% of your FICO rating. With VantageScore, kind of credit score and credit score age are mixed into the identical class, which makes up roughly 21% of your VantageScore.

With each kinds of scores, credit score combine is a comparatively small portion of what determines a credit score rating, so having the right credit score combine shouldn’t be essentially important to be able to have good credit score. Nevertheless, it’s nonetheless an excellent factor to intention for, particularly if you wish to get a excellent 850 credit score rating or someplace near it.

As well as, the significance of credit score combine may very well be extra vital for those who have skinny credit score information, says credit score professional John Ulzheimer.

Revolving Credit score Holds Extra Weight Than Installment Credit score

Understand that not all credit score accounts have the identical affect in your credit score rating. Revolving accounts are weighed extra closely by credit score scoring fashions as a result of they’re a greater predictor of credit score threat than installment accounts.

Whereas each account sorts have an effect on your fee historical past, revolving debt has a a lot higher affect in your credit score utilization since you possibly can select how a lot of your credit score restrict to make the most of and pay again every month.

Since credit score utilization makes up a big portion of your credit score rating (30% for FICO scores and 20% for VantageScores), this provides revolving accounts numerous affect over your rating.

For an in-depth dialogue of this subject, see our article, “Are Revolving Accounts Extra Highly effective Than Installment Accounts?”

What Is a Good Credit score Combine?

FICO excessive rating achievers have a median of seven bank cards on their credit score experiences. Picture by Hloom on Flickr.

Relating to your credit score rating, an important factor is to exhibit that you’ve managed each revolving and installment accounts. Due to this fact, it’s greatest to have at the very least one kind of account of every kind.

For instance, you might need a bank card (revolving) and an auto mortgage or pupil mortgage (installment). Or, you possibly can have a mortgage (installment) and a HELOC (revolving). Any mixture of 1 revolving account and one installment account is an effective begin in your credit score combine.

FICO helps this concept, saying, “Having bank cards and installment loans with an excellent credit score historical past will increase your FICO Scores.”

FICO additionally says that individuals who have managed bank cards responsibly are higher off than shoppers that don’t have any bank cards, who could be seen as dangerous as a result of they haven’t demonstrated expertise in utilizing revolving credit score.

Statistics present that top FICO rating achievers have a median of seven bank cards on their credit score experiences, which incorporates each open and closed accounts.

Individuals with credit score scores within the 800s additionally sometimes have installment loans akin to mortgages and auto loans, in response to Experian.

The full variety of accounts in your file might also play a job. FICO has indicated that these with excessive credit score scores can have 20+ credit score accounts of their credit score experiences.

How Many Credit score Playing cards Is Too Many?

Having too many bank card accounts might damage your credit score rating.

Understand that it’s potential to have too many accounts in your credit score file. In line with the FTC, having too many bank cards might have a destructive impact in your credit score rating, as might having loans from some kinds of firms.

There isn’t a hard-and-fast rule in relation to what number of bank cards is simply too many as a result of the affect of any given issue in your credit score rating is determined by what’s already in your credit score profile, says FICO.

Nevertheless, in determine 1 within the article “How Credit score Actions Influence FICO Scores,” the hypothetical shopper “Rachel,” who has 33 credit score accounts, has a decrease credit score rating than “Maria,” who has 21 accounts.

This would appear to suggest that at some quantity between 21 and 33 accounts, one’s credit score rating may start to undergo. Nevertheless, these two shoppers produce other variations of their credit score profiles, so the distinction of their credit score scores can’t be solely attributed to the variety of accounts of their information.

For extra info on this subject, try “What’s the ‘Proper’ Variety of Credit score Playing cards?” by John Ulzheimer and “Is There Such a Factor as Too A lot Credit score?”

Can Some Account Varieties Harm Your Credit score?

Sure kinds of loans in your credit score report might make you appear to be a extra dangerous shopper and subsequently might find yourself hurting your rating as an alternative of serving to.

Why? It’s all primarily based on statistics and who the credit score rating algorithms have deemed to be dangerous debtors.

Having a furnishings mortgage in your credit score profile might make you seem like a credit score threat and probably decrease your rating.

For instance, taking out a furnishings mortgage might truly drop your credit score rating. That’s as a result of furnishings loans are sometimes reported as “shopper finance loans,” that are sometimes reserved for debtors with low credit score who’re statistically extra prone to default on loans.

Due to this fact, having such a account in your credit score report may very well be considered as a destructive issue by lenders and credit score scoring algorithms.

Alternatively, the financing association could also be reported as revolving debt, which can seem almost maxed out till you make sufficient funds to get the stability to a decrease degree.

Bike loans are one other instance of this. Bike loans are dangerous investments to lenders since there’s a larger probability of the borrower not repaying the mortgage as a result of harm or loss of life and a better probability of the automobile being broken, which reduces its worth as collateral.

Since having a bike mortgage in your credit score report signifies a better credit score threat, such a account might additionally damage your credit score.

Payday and title loans, then again, are sometimes not reported to the credit score bureaus, so all these loans received’t depend towards your credit score combine or credit score rating—until, in fact, you default on a mortgage and it will get offered to a group company, who will then report it as a assortment account.

Conclusions on Credit score Combine

Since credit score combine makes up about 10% of your credit score rating, it’s useful to attempt to obtain a balanced mixture of credit score by protecting a number of revolving and installment accounts in good standing.

The most effective credit score combine ought to ideally embody a number of bank cards and at the very least one or two installment loans, akin to mortgages or auto loans.

Nevertheless, it’s additionally vital to notice that credit score combine is way much less vital than different credit score rating elements, akin to fee historical past, credit score utilization, and credit score age.

Reaching the right credit score combine might be not price obsessing over since you received’t robotically get a superb credit score rating simply by having the perfect mixture of accounts.

As well as, most individuals naturally accumulate various kinds of accounts over time, so it’s in all probability not essential to start out opening new accounts left and proper solely for the aim of increase your credit score combine. This technique might end in laborious inquiries and new accounts bringing your rating down within the brief time period, and gaining access to credit score you don’t want might additionally encourage additional spending.

Nevertheless, a method so as to add tradelines to the combination with out the dangers of opening a brand new major account is to change into an licensed consumer.

As with all credit-related choices, it’s as much as you to take your total monetary targets and priorities into consideration earlier than taking motion. You may resolve that you simply don’t want to fret an excessive amount of about enhancing your credit score combine, and that’s completely tremendous. Alternatively, enhancing your credit score combine can solely assist your credit score rating, and it’s one thing that it is best to take note of in the event you aspire to get an ideal 850 credit score rating.

[ad_2]

Source link

{kind=link}