[ad_1]

I’ve more and more acquired emails from debtors of their 60s and even 70s who owe greater than six figures of pupil loans. They need to retire, however they assume they’ll by no means be capable of afford to. Some have even thought-about the chance that they are going to die with pupil loans.

Perhaps you’ve got a bunch of pupil mortgage debt and assume you’ll be taking it to the grave.

What’s loopy is in uncommon circumstances, is that in case you die with pupil debt it may provide help to to realize your monetary targets. You’ll be able to shield your loved ones with some extra planning that may mean you can stay the life you need regardless of how tousled your funds are.

Whereas understanding what occurs to pupil loans if you die is vital, no one below the age of fifty in good well being ought to dare to consider this technique. That is primarily for debtors who owed greater than they ever dreamed attainable whereas going into their golden years.

I notice how nuts the declare that dying with pupil debt may very well be okay sounds. Stick to me to see how sure debtors may give up their jobs and retire because of math.

What Occurs When You Die With Scholar Loans?

With federal pupil loans, the federal government forgives the debt fully. Your loved ones doesn’t want to fret about having to pay again that form of debt, even when it’s a whole lot of hundreds of {dollars}.

Personal pupil mortgage lenders nearly all the time forgive the debt too. The issue is that their promissory notes (the contract you signed if you agreed to the debt) usually don’t require them to grant a pupil mortgage discharge due to loss of life.

President Trump lately signed a invoice that vastly expands protections for personal pupil loans when the borrower or cosigner dies. I anticipate that for loans take out in 2019 and past, worrying about what’s within the mortgage contract received’t matter. When you die, your loved ones received’t be on the hook.

Till then, simply convey up the contract in your pc and press Ctrl+F and sort in some phrases involving loss of life, like “die, loss of life, forgiveness, forgiven, and many others.”

See what the lender says about dying with the debt. In the event that they don’t say something, ask their customer support reps what occurs in case you died earlier than the loans receives a commission off.

The fact is that no lender desires to indicate up within the information asking a widow or widower for cash they don’t have. Successfully, having your pupil loans forgiven as a consequence of loss of life is one thing you shouldn’t fear about. It is going to occur.

When you’re the sort that worries anyway, purchase a time period life insurance coverage plan for $20 to $40 a month. This will help shield your partner from inheriting pupil mortgage debt. I obtained $1 million in safety with Haven Life and you would get as a lot as $2 million. I recommend you’ve got no less than 8 instances your wage in protection when you have a household relying in your earnings.

The Two Sorts of Mortgage Forgiveness For Older Debtors

There are two methods to get loan forgiveness. One is thru the Public Service Loan Forgiveness (PSLF) program. The opposite is by paying for 20-25 years on an income-driven plan after which paying taxes on the forgiven stability on the finish.

With PSLF, it’s essential to pay for 10 years on an income-driven plan whereas working at a not for revenue or authorities employer. On the finish of the 10-year interval, the federal government writes off the remaining stability tax-free.

The issue is that PSLF requires full-time employment for a decade. When you’re already approaching retirement, that is likely to be one thing you’re not considering doing. One other complication is that you just won’t have qualifying loans.

Parent Plus loans have to be consolidated and paid on the ICR program to be eligible. You may have years of credit score working in the proper of employer however nonetheless not obtain the PSLF profit on this case. For Direct loans in your individual title, you’ll have extra reimbursement choices and can be extra prone to obtain credit score with out additional work.

Let’s say you need to get mortgage forgiveness however work within the non-public sector or will retire earlier than receiving 10 years’ credit score in the direction of PSLF.

When you’ve got no credit score in the direction of mortgage forgiveness and are coming into reimbursement for the primary time, then you definitely’ll have to pay based mostly in your earnings for 20 years on the Pay As You Earn (PAYE) program and 25 years on the Revised Pay As You Earn (REPAYE) or Earnings Contingent Reimbursement (ICR) program.

On the finish of that interval, the forgiven stability is taxable earnings. That scares lots of people who’re terrified by the prospect of receiving a six-figure tax invoice due multi functional yr.

Except you sadly have some well being situation the place you don’t anticipate to stay a very long time, it’s best to by no means take into consideration dying together with your debt as a method in case you’re below 50.

When you can afford to simply pay again your debt above 50, it’s best to. Most individuals above 50 stay lengthy, wholesome lives.

Going for PSLF is a simple technique that will require extending your working profession till you obtain the profit. That’s why I’m going to deal with the technique of paying your loans for 20-25 years as a result of it applies to everybody.

Loopholes for Dying with Scholar Debt

Loophole #1: You shouldn’t have to be employed to obtain credit score in the direction of the 20-25 yr mortgage forgiveness with the tax bomb. Meaning a retiree residing on Social Safety may pay a nominal quantity of $100-$200 a month and obtain credit score in the direction of mortgage forgiveness.

Loophole #2: The IRS has one thing referred to as an insolvency rule. The rule states that when you have forgiven debt that’s taxable earnings, you need to be solvent to be taxed. Meaning in case you owe extra in debt than you do in belongings, the debt will get wiped away tax-free.

Loophole #3: Would you somewhat be useless or need to take care of a tax cost plan with the IRS? Debtors of their 60s or 70s are certain as all of us are by actuarial tables. If there’s a 50/50 likelihood you’d need to pay a tax bomb and also you do find yourself residing that lengthy, you’ve received.

I’m not attempting to make you are feeling awkward or be frightened about your individual mortality. I need you to have the ability to afford to retire or work fewer hours even in case you owe greater than $100,000.

Who’s the “Die with Scholar Loans” Situation Finest For?

The “dying with debt” technique may make loads of sense for near-retirees with lower than $1 million in belongings who owe greater than $100,000 in pupil debt.

If that’s you, then you definitely’re not alone. About 30% of seniors haven’t any retirement financial savings, in line with the Authorities Accountability Workplace. Those who do have near $150,000 on common.

In line with Dept of Schooling information that we’ve interpreted, there are about 3.5 million Mother or father Plus debtors within the US. Many median age adults and seniors return to highschool themselves for profession transitions and take out Direct Federal Loans in their very own title.

Meaning there are probably a whole lot of hundreds of debtors on the market who’re of their 50s, 60s, or 70s who’ve six figures of pupil debt.

When you needed to borrow to fund schooling for your self or your youngsters, then which means it’s probably you’ve got lower than $1 million in belongings. Actually, nearly each single borrower with out a lot cost credit score to mortgage forgiveness, who desires to retire quickly, and is over age 60 may use the “die with debt” technique.

That might create huge losses for taxpayers within the federal pupil mortgage portfolio, however it might permit debtors to say their monetary safety again.

Why Math Says Many Scholar Mortgage Debtors Above 60 Received’t Pay Again Their Scholar Loans

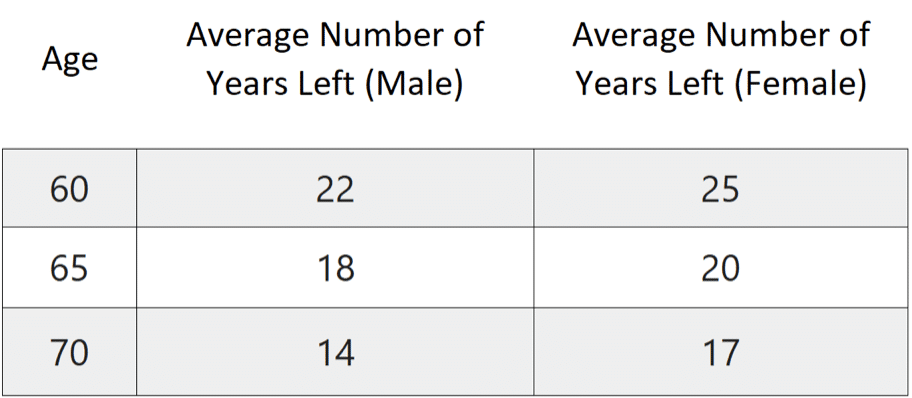

Right here’s what the Social Security Administration says in regards to the variety of years they anticipate you to stay at sure ages.

Supply: Social Safety

Discover that the Social Safety Administration expects the typical 60-year-old girl to have 25 years left on Earth. Assume there’s nothing particular in regards to the inhabitants who borrows for themselves or for his or her youngsters for faculty.

That might imply the typical feminine borrower with Mother or father PLUS loans over $100,000 and with low earnings would have a 50/50 likelihood of by no means needing to fret in regards to the pupil mortgage tax bomb that occurs at forgiveness.

Discover that males stay fewer years than ladies. When you’re in your mid-60s, then males can anticipate to stay one other 18 years. Meaning nearly all of males at 65 who’ve pupil debt and whose funds based mostly on their earnings are low may anticipate to die nonetheless owing pupil debt.

When you stay longer than the Social Safety Administration expects, you shouldn’t fear about tax penalties.

Let’s swap to examples of how this “die with pupil loans” technique would work.

The 63-12 months-Previous Mother or father Plus Borrower with Three Children in Faculty

Let’s assume that Jim is a gross sales government at a small enterprise and would like to retire in two years. He despatched his three youngsters to non-public Catholic liberal arts colleges within the Northeast. All of them entered low paying careers, and there’s no method to switch the debt to the youngsters with out refinancing. Jim actually doesn’t need to put the burden on his youngsters in that method.

Jim additionally desperately desires to do away with the debt, however it’s all Mother or father Plus loans at $300,000 at a 7.5% rate of interest. Jim has no mortgage and about $200,000 saved in his 401k due to a divorce. He feels distressed that the one path ahead is to work till the coed loans are gone. He has no credit score in the direction of forgiveness but.

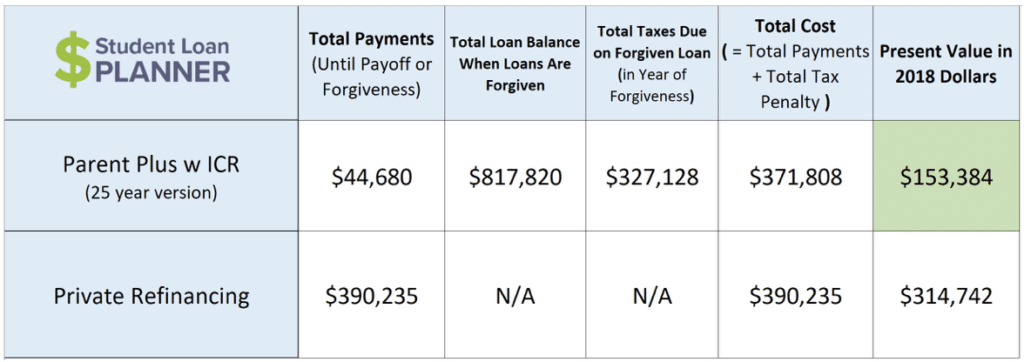

Jim decides to consolidate his Mother or father PLUS loans right into a Direct Consolidation mortgage to get entry to the ICR plan.

If he paid again the Mother or father Plus loans the old style method, he would want to pay about $3,200 a month for 10 years. Lastly, he’d be debt free and may even have some additional 401k financial savings to make use of in the direction of retirement.

The issue is that he must work till 73. What if he misplaced his job or burned out earlier than then?

Alternatively, I’ll recommend that Jim plans a radical technique the place he may doubtlessly die with the debt, however he’ll have a backup plan. Jim will work two extra years and delay Social Safety till age 70. The reason being that he would obtain a better profit than if he claimed it on the full retirement age.

As an alternative of taking Social Safety at age 66 and getting a good thing about $2,600, Jim will obtain a good thing about about $3,400 a month at 70. Jim will stay on his retirement financial savings till he hits age 70.

Since Jim’s taxable earnings is so low and he’s counting on Social Safety completely, his earnings for functions of pupil mortgage earnings contingent reimbursement can be near $0. His solely important funds on ICR come within the remaining 2 years he works. He may even be capable of keep away from these funds with a forbearance.

Discover that Jim solely pays about $44,000 on his Mother or father Plus loans. They develop from $300,000 to $817,000 over 25 years. He would then owe about $327,000 in taxes in a 40% tax bracket.

Right here’s the place actuality steps in although. Based mostly on Social Safety’s information, there’s a greater than 50% likelihood that Jim doesn’t stay till the tax bomb hits him at 88.

If it does, Jim’s liabilities will probably be better than his belongings, and the federal government would forgive the debt with out tax.

If it didn’t, then the associated fee in right this moment’s {dollars} can be half as a lot as if Jim paid all of it again. Jim may put away $600 a month in an index fund account to pay the tax invoice if he was that frightened about it.

What is going to Jim do for nursing dwelling bills? A grimy little secret of America is that almost all of the center class depends on Medicaid to cowl these payments.

There can be important obstacles to doing this technique that will be primarily rooted in satisfaction. Jim in all probability by no means dreamed of himself as somebody who would want to depend on any authorities applications to have good choices financially in his life.

Nonetheless, his different is working for one more 10 years, 8 years previous his desired retirement date. That’s an enormous chunk of his life expectancy that he’s devoting to work that he’d in all probability somewhat not do.

Through the use of this dying with pupil debt technique, Jim may use these 8 years to journey, chill out, and luxuriate in household and associates as a substitute.

Sarah the 65-12 months-Previous Lawyer with Glorious Genes

Sarah went to legislation college through the recession as a result of she obtained laid off from her company advertising job. She all the time wished to strive one thing else, and Sarah has all the time thought she would retire at 70.

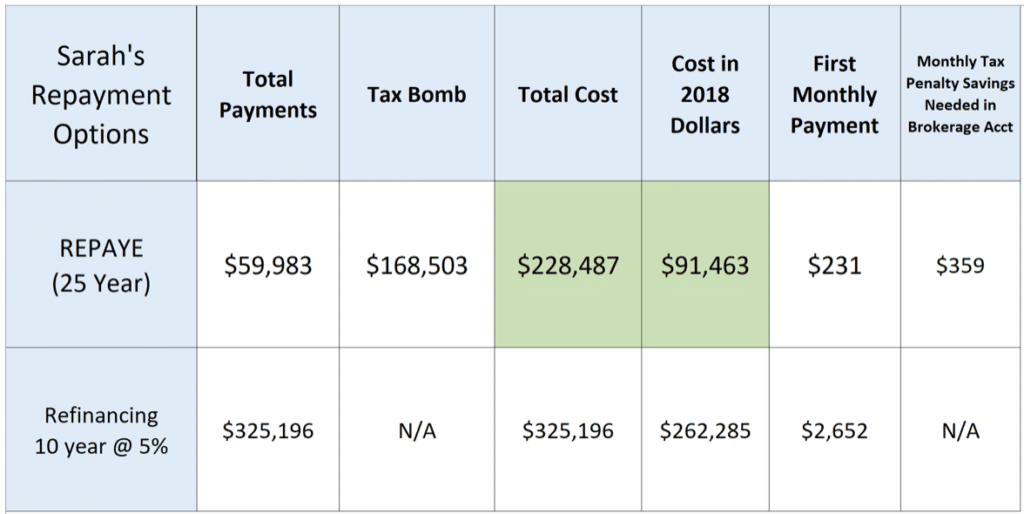

She has made some decisions she needs she may take again with forbearance and deferment. She solely has two years of credit score towards mortgage forgiveness on the Revised Pay As You Earn (REPAYE) plan for her Direct federal loans in consequence. Sarah’s debt is $250,000 at a 7% rate of interest.

Sarah earns $70,000 a yr and can make about $40,000 a yr in retirement from a mixture of retirement earnings and Social Safety. Sarah owns her $250,000 home. We’ll assume Sarah saves the max of $24,500 a yr in retirement. Most ladies in her household stay previous 90.

Sarah may be very involved that she received’t be capable of retire in any respect due to her big legislation college debt. Right here’s what the price of REPAYE vs paying all of it again appears like for Sarah.

Discover that Sarah would solely need to pay about $60,000 till 2041 since she already has two years of credit score.

We’re assuming that Sarah lives previous 90 and that she would want to determine the tax bomb at that age.

Even when she needed to pay the $168,000 taxes abruptly, her value in right this moment’s {dollars} can be about $91,000 vs $262,000 in right this moment’s {dollars} if she refinanced.

When you’re Sarah, which possibility do you select? Paying 50% of your take-home pay to your loans and work one other 10 years? Or do you retire in 5 years then roll the cube together with your life expectancy and gamble on the coed mortgage guidelines?

I view it as extremely unlikely that the IRS comes after a 90-year-old girl for a tax invoice if she doesn’t have the belongings to pay stated invoice.

Is Dying with Your Scholar Loans a Horrible Thought, and Is It Immoral?

I might by no means recommend to anybody that they use this technique on objective if they’ve sufficient time to plan in any other case.

I might additionally recommend a modification to the title of this technique. It’s the “Die with Scholar Loans or Reside and Cope with the IRS” technique.

When you stay and need to take care of the IRS if you get the tax invoice from the forgiven stability, you win. When you’re useless, you haven’t received however you don’t have to fret in regards to the debt affecting your loved ones.

Think about the optics of the IRS attempting to gather taxes from aged individuals with out substantial belongings. When you’ve got tens of millions in retirement financial savings they’ll get their cash. Nonetheless, in case you’re a typical middle-class American, on the very worst they’d arrange a cost plan.

Almost definitely, they’d write off the debt and you’ll be counting on Medicaid to pay for Social Safety bills anyway.

Profiting from the loopholes within the pupil mortgage system shouldn’t be immoral any greater than using the tax code to legally pay as little as attainable in taxes.

When you dislike the system lawmakers created and assume folks shouldn’t be in a position to do the technique that I outlined, name your consultant and allow them to know that.

If you’re one of many a whole lot of hundreds if not tens of millions of debtors over 60 with pupil loans, you propose to stay on Social Safety, you’ve got lower than $1 million in belongings, and also you’d somewhat roll the cube so you possibly can retire earlier than your mid-70s, this technique may very well be for you.

We focus on making custom plans for borrowers in six figures of student debt . We care completely about getting the bottom value for debtors and serving to you determine easy methods to obtain what you need to in life if you owe greater than $100,000 of pupil debt. When you’re considering extra data about this service, contact us so that you don’t have to determine this needlessly complicated system alone.

Refinance pupil loans, get a bonus in 2021

$1,000 BONUS1For 100k or extra. $200 for 50k to $99,999¹

$1,250 BONUS2For 250k+, tiered 300 to 500 bonus for 50k to 250k.2

$1,275 BONUS3For 150k+. Tiered 300 to 575 bonus for 50k to 149k.3

$1,000 BONUS4For $100k or extra. $200 for $50k to $99,9994

$1,050 BONUS5For 100k+. $300 bonus for 50k to 99k.5

$1,250 BONUS6For 100k+ or $350 for 5k to 100k.6

$1,250 BONUS7For 150k+. Tiered 100 to 400 bonus for 25k to 149k.7

Undecided what to do together with your pupil loans?

Take our 11 query quiz to get a customized advice of whether or not it’s best to pursue PSLF, IDR forgiveness, or refinancing (together with the one lender we expect may provide the finest charge).

1Earnest: $1,000 for $100K or extra, $200 for $50K to $99.999.99. For Earnest, in case you refinance $100,000 or extra by means of this web site, $500 of the $1,000 money bonus is offered straight by Scholar Mortgage Planner. Price vary above consists of non-compulsory 0.25% Auto Pay low costEarnest disclosures. 2Laurel Highway: When you refinance greater than $250,000 by means of our hyperlink and Scholar Mortgage Planner receives credit score, a $500 money bonus will probably be offered straight by Scholar Mortgage Planner. If you’re a member of an expert affiliation, Laurel Highway may give you the selection of an rate of interest low cost or the $300, $500, or $750 money bonus talked about above. Provides from Laurel Highway can’t be mixed. Price vary above consists of non-compulsory 0.25% Auto Pay low cost. Laurel Road disclosures.3Elfi: When you refinance over $150,000 by means of this web site, $500 of the money bonus listed above is offered straight by Scholar Mortgage Planner. Elfi disclosure. 4Sofi: When you refinance $100,000 or extra by means of this web site, $500 of the $1,000 money bonus is offered straight by Scholar Mortgage Planner. Price vary above consists of non-compulsory 0.25% Auto Pay low cost. Sofi disclosures.5Commonbond: When you refinance over $100,000 by means of this web site, $500 of the money bonus listed above is offered straight by Scholar Mortgage Planner. Commonbond disclosure. 6Credible: When you refinance over $100,000 by means of this web site, $500 of the money bonus listed above is offered straight by Scholar Mortgage Planner. Credible disclosure.

7LendKey: When you refinance over $150,000 by means of this web site, $500 of the money bonus listed above is offered straight by Scholar Mortgage Planner. Price vary above consists of non-compulsory 0.25% Auto Pay low cost.

[ad_2]

Source link

{kind=link}