[ad_1]

The reply might be pretty simple. It’d make sense to refinance non-public pupil loans when you can:

- Get a decrease rate of interest.

- Decrease your month-to-month funds (so you may deal with different debt).

- Benefit from one other lender’s favorable reimbursement phrases.

It may be that easy, as a result of not like refinancing your mortgage the place there are a ton of charges concerned, there aren’t any closing prices to refinance your pupil loans. You may even qualify for an awesome cash-back refinancing bonus.

That makes it simpler to determine whether or not to refinance non-public pupil loans as a result of there’s no offsetting expense or “break even” level that needs to be calculated. All financial savings movement proper again into your pocket.

Even when you simply refinanced six months in the past, it may be an awesome concept to take a contemporary take a look at refinancing, as a result of pupil mortgage charges are close to historic lows.

Advantages of refinancing non-public pupil loans

There are three fundamental advantages of refinancing non-public pupil loans:

1. Lower your expenses on curiosity

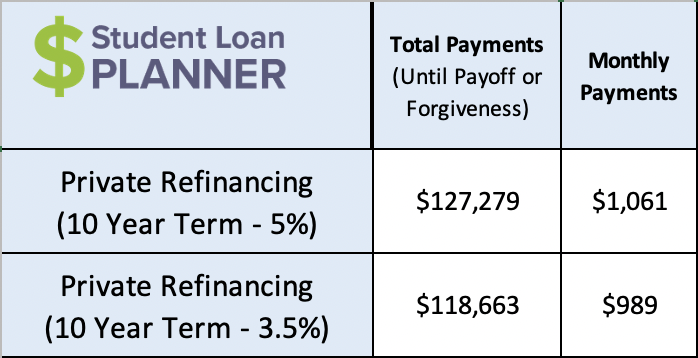

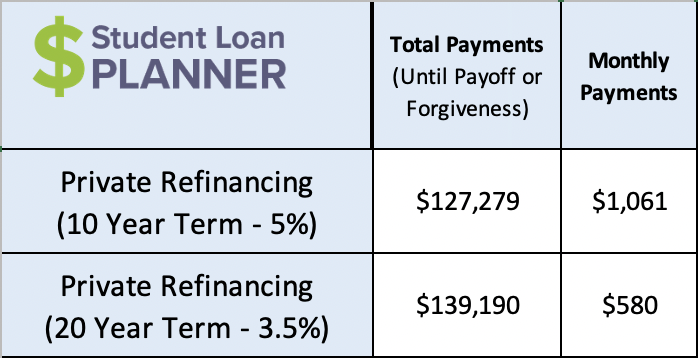

Let’s say that somebody has $100,000 in non-public pupil debt at 5% on a 10-year, fixed-interest charge. At this time, they’ve the chance to refinance to three.5%.

By refinancing, they’d save $8,616 in curiosity and are student-debt free in the identical timeframe. Wouldn’t you relatively have that extra cash in your checking account? It’s a no brainer.

2. Decrease your mortgage fee

Within the instance above, refinancing non-public pupil loans lowers the funds on their pupil mortgage debt by $72 per 30 days.

Now let’s say that it’s worthwhile to decrease your mortgage fee since you had a drop in revenue, wish to clear up bank card debt or construct up an emergency fund within the meantime.

How would the funds change if this 10-year mortgage was refinanced to twenty years?

Going out to a long run would decrease funds by almost $500 per 30 days even with the unique mortgage quantity being the identical.

Be aware: The purpose is to repay non-public pupil loans as shortly as doable, but when somebody wants short-term reduction, then an extended refinance time period is an efficient choice till they get again on their toes.

3. Change mortgage reimbursement phrases and circumstances

The first causes to refinance are rates of interest and fee quantities, however different components are additionally vital.

For instance, some lenders are providing a big quantity of forbearance — between 12 and 36 months. In case your present non-public lender doesn’t have this feature, then it would make sense to refinance to get these mortgage phrases. That is assuming you’re not sacrificing the price of pupil mortgage reimbursement.

One more reason is you probably have a variable rate of interest and it’s going to take you longer than three to 5 years to repay your mortgage.

Fastened rates of interest are higher the longer the time-frame you select. So, if it’s going to take you greater than 5 years to repay the steadiness of your non-public pupil loans, swap the variable charge for a hard and fast charge.

For the explanations above and extra, refinancing might be a good way to alter your reimbursement choices and get higher mortgage phrases.

Tips on how to refinance non-public pupil loans

As soon as you recognize that personal mortgage refinancing is best for you, then it’s time to try the completely different lenders on the market.

All of them may appear the identical, however some supply higher phrases in sure conditions.

Some lenders are higher for healthcare staff whereas some supply unemployment safety. Some lenders discover the very best charges by going via group banks and credit score unions, and a few reward debtors with a clear credit score report.

Evaluating your choices throughout a number of lenders is well worth the time. You by no means know if you are able to do higher until you verify with a couple of lenders.

Listed here are the steps to refinance non-public pupil loans:

- Begin by viewing today’s top refinancing lenders that Scholar Mortgage Planner companions with.

- Choose three to 5 lenders to get preliminary charges. Click on the hyperlinks via our web site and register with a brand new e-mail tackle to probably qualify for a cash-back bonus.

- Examine rates of interest and phrases throughout the lenders to see which gives you the bottom charges with versatile reimbursement phrases.

- Select a lender that offers you the very best phrases.

- Full the coed mortgage refinancing utility on-line.

- Obtain the ultimate supply and settle for it inside 30 days, if the supply is smart in your state of affairs.

- The brand new lender you chose will repay your previous lender. You’ll then begin making funds beneath your new mortgage phrases with the brand new lender.

Fast notice: Typically individuals get involved that taking a look at multiple firm will have an effect on your credit score rating, however that’s not true. These preliminary charges are “gentle” credit score pulls which doesn’t materially have an effect on your credit score rating regardless of what number of you do.

There’s additionally what’s known as “charge procuring” whenever you discover many choices over a 14 to 45 day interval. Throughout this window, a number of gentle credit score checks are counted as one in your credit score report.

It’s value it to take a look at as many as doable to ensure you safe the very best rates of interest and phrases.

Ought to I refinance my non-public pupil loans?

You need to discover refinancing your non-public pupil loans if you will get a greater rate of interest, want to regulate your required month-to-month fee, or lately had a pleasant leap in your credit score rating.

There’s no hurt in checking even when you refinanced six months in the past.

Keep in mind, there aren’t any closing prices so that you don’t should calculate a “break even” charge. If you will get even 0.25% decrease, it’s value it.

Simply do not forget that you probably have eight years to go and also you refinance to a contemporary 10-year time period, you’re resetting the clock which may find yourself costing you extra in curiosity. Even when the required fee is decrease on the refinance, put as a lot cash into it as you may (if doable) to get out of debt sooner and pay much less curiosity.

Keep in mind the 1st step: refinance your student loans via our web site. Our accomplice lenders account for the overwhelming majority of the coed mortgage refinancing market. Plus, we take decrease promoting charges from them to give you among the greatest cash-back bonuses on the market.

We would like you to save lots of as a lot cash as doable whenever you refinance your non-public pupil loans, so take a look at if you will get a greater charge and qualify for a bonus.

Refinance pupil loans, get a bonus in 2021

$1,000 BONUS1For 100k or extra. $200 for 50k to $99,999¹

$1,250 BONUS2For 250k+, tiered 300 to 500 bonus for 50k to 250k.2

$1,275 BONUS3For 150k+. Tiered 300 to 575 bonus for 50k to 149k.3

$1,000 BONUS4For $100k or extra. $200 for $50k to $99,9994

$1,050 BONUS5For 100k+. $300 bonus for 50k to 99k.5

$1,250 BONUS6For 100k+ or $350 for 5k to 100k.6

$1,250 BONUS7For 150k+. Tiered 100 to 400 bonus for 25k to 149k.7

Unsure what to do together with your pupil loans?

Take our 11 query quiz to get a customized advice of whether or not you must pursue PSLF, IDR forgiveness, or refinancing (together with the one lender we expect may provide the greatest charge).

1Earnest: $1,000 for $100K or extra, $200 for $50K to $99.999.99. For Earnest, when you refinance $100,000 or extra via this web site, $500 of the $1,000 money bonus is supplied straight by Scholar Mortgage Planner. Charge vary above contains non-compulsory 0.25% Auto Pay low costEarnest disclosures. 2Laurel Highway: If you happen to refinance greater than $250,000 via our hyperlink and Scholar Mortgage Planner receives credit score, a $500 money bonus can be supplied straight by Scholar Mortgage Planner. If you’re a member of knowledgeable affiliation, Laurel Highway may give you the selection of an rate of interest low cost or the $300, $500, or $750 money bonus talked about above. Affords from Laurel Highway can’t be mixed. Charge vary above contains non-compulsory 0.25% Auto Pay low cost. Laurel Road disclosures.3Elfi: If you happen to refinance over $150,000 via this web site, $500 of the money bonus listed above is supplied straight by Scholar Mortgage Planner. Elfi disclosure. 4Sofi: If you happen to refinance $100,000 or extra via this web site, $500 of the $1,000 money bonus is supplied straight by Scholar Mortgage Planner. Charge vary above contains non-compulsory 0.25% Auto Pay low cost. Sofi disclosures.5Commonbond: If you happen to refinance over $100,000 via this web site, $500 of the money bonus listed above is supplied straight by Scholar Mortgage Planner. Commonbond disclosure. 6Credible: If you happen to refinance over $100,000 via this web site, $500 of the money bonus listed above is supplied straight by Scholar Mortgage Planner. Credible disclosure.

7LendKey: If you happen to refinance over $150,000 via this web site, $500 of the money bonus listed above is supplied straight by Scholar Mortgage Planner. Charge vary above contains non-compulsory 0.25% Auto Pay low cost.

[ad_2]

Source link

{kind=link}