[ad_1]

Let me begin by saying that I consider wholeheartedly in acupuncture. It helped me handle a knee damage extra successfully than going by bodily remedy for six months. I additionally get handled routinely to handle my again. So, I totally assist acupuncture college students pursuing this beneficial occupation.

Truthfully, I wasn’t even conscious of the burden of scholar mortgage debt for acupuncturists and what they face. That was till I had 5 consults within the final two months out of the blue.

After listening to their tales and performing some analysis, I’ve realized acupuncture scholar mortgage debt is an actual drawback. Many have six-figure acupuncture faculty mortgage debt, run their very own apply, and have needed to tackle bank card debt as their enterprise ramps up.

However there’s an attainable path to face their scholar loans, and eliminate it. I’ll present you a case research and get into find out how to repay acupuncture scholar loans under.

Pupil mortgage debt for acupuncturists in oriental drugs applications hovering as states require extra education

The apply of Acupuncture and Oriental Medication goes again millennia. However right here in the US, licensing and regulations are pretty new and range extensively from state to state.

In additional populated states like California and New York, a Masters in Acupuncture and Oriental Medication (MAOM) shouldn’t be sufficient. Acupuncturists who apply there most probably must pay for extra education to get their doctorate (DAOM).

New York requires 4050 hours of didactic and scientific coaching; 60 semester hours together with 9 semester hours of biosciences. California requires 3000 hours of research in curriculum pertaining to the apply of acupuncturist from an accredited faculty; 50 hours of constant training each two years; further hours of coaching in natural drugs and the passing of an natural drugs examination.

However in Pennsylvania, you don’t even want to finish a level. Acupuncture college students solely want two years of education and to go the NCCAOM examination.

Most practitioners get a high quality training and coaching from acupuncture applications like Pacific Faculty of Oriental Medication (PCOM), Oregon Faculty of Oriental Medication (OCOM), Emperor’s Faculty College of Conventional Oriental Medication, and others. However for the reason that state rules range extensively, there are many scammy acupuncture faculties who make the most of aspiring acupuncturists.

Fortuitously, I haven’t heard about too many individuals in that scenario, however I do know it exists.

Acupuncture college students pursue their ardour at any value

When somebody decides to get their Masters or Doctorate in Acupuncture in Oriental Medication, the MAOM or DAOM, chances are high they’re not in it for the cash. Medical doctors of Acupuncture are caring people who need to heal individuals and assist them handle the bodily points (e.g. headache, accidents and illnesses) and emotional stressors (e.g. melancholy and anxiousness) of their lives.

There’s a big cost to pursue their passion. However the associated fee is so massive that it simply doesn’t register.

It’s type of like on the lookout for a home desiring to spend not more than $250,000. However you find yourself spending $290,000. On the floor, it doesn’t look like that rather more. However in actuality, the $40,000 distinction is a ton of cash. You would take 10 separate $4,000 holidays, fund your IRA for seven years, or purchase two $20,000 vehicles for money. While you body it like that, it’s a lot simpler to see the distinction in value and the importance of the choice.

I’m certain that many acupuncture college students know the associated fee and it’s value it to pursue a satisfying profession.

Constructing an acupuncture apply takes time

Operating a enterprise is difficult for anybody, and acupuncturists aren’t any completely different.

If beginning a apply in New York or California (and in most locations for that matter), a licensed acupuncturist isn’t paid their full fee beginning out. Typically, they must resort to Groupon reductions to get individuals within the door. Many acupuncturists begin out making $20,000 to $30,000 their first yr out of college.

It’s powerful to make ends meet early on. So, carrying some bank card debt is the norm on high of six-figure scholar mortgage debt.

Enterprise picks up after just a few years once they begin getting recurring enterprise from their referral community together with sufferers, the VA, docs, chiropractors, counselors, and therapists, and so forth.

Subsequent is all about dealing with the rising scholar mortgage debt however it’s powerful to have a look at.

Pupil mortgage debt appears insurmountable

The acupuncturists I’ve labored with have a mean of $211,000 in scholar loans with a 7% rate of interest and earn about $40,000 to $60,000. If that is just like your scenario, you might be questioning will I ever have the ability to repay my scholar loans?

In the event that they had been to take an aggressive strategy by paying again their loans on the 10-year customary plan, their month-to-month cost can be $2,450 per 30 days. That works out to almost 75% of take-home pay and is a non-starter.

Many have already got bank card debt to go together with their scholar debt too.

When confronted with numbers like that, it’s pure for any particular person to retreat and keep away from it. Simply put it into deferment or forbearance and by no means face it till it’s important to.

If acupuncturists solely knew that there’s an inexpensive option to pay again their loans, they could have extra confidence to get a plan in place, however…

Pupil mortgage reimbursement is complicated

Doesn’t it really feel like scholar mortgage reimbursement is designed to be complicated?

Graduated, Prolonged, Commonplace, PAYE, REPAYE, IBR, Consolidation, Refinancing. Blech! All of this terminology is the least probably factor to make an acupuncture scholar really feel like they’ll take management of this case.

With massive debt, restricted earnings, and unreliable data, it’s no marvel acupuncturists keep away from dealing with their scholar loans.

Case research: An acupuncturist saves cash with a scholar mortgage plan

Lily completed her Masters of Acupuncture and Oriental Medication 5 years in the past and has spent the final three years working and constructing her personal apply.

She has $230,000 in scholar mortgage debt at 7%. Her earnings is $50,000 and is projected to develop to $70,000 over the following three years. She’s been on IBR (earnings primarily based reimbursement) for the final three years.

Lily is in a critical relationship however shouldn’t be planning to get married anytime quickly on account of her scholar loans.

So far as month-to-month funds go, Lily talked about that her scholar mortgage funds on IBR had been manageable and she or he may throw one other $300/month at them if she had too.

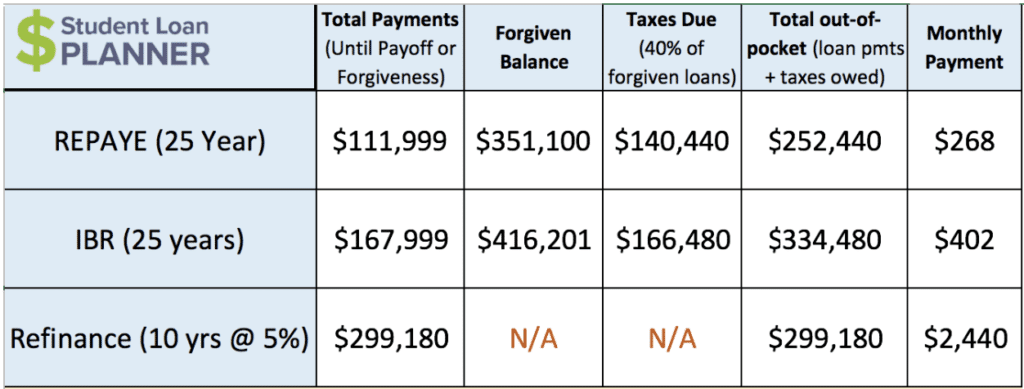

Let’s check out a few of her choices to refinance scholar loans:

First off, we will rule out refinancing as a result of hefty funds in comparison with Lily’s earnings.

She’s paying $402/month on IBR, however there’s no manner she will be able to decide to a $2,440 month-to-month cost for 10 years. She’s solely taking dwelling about $3,500/month.

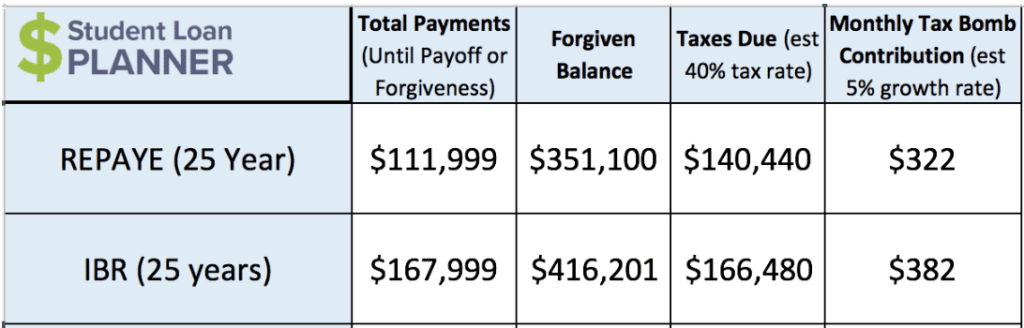

Apart from her month-to-month funds, her present path on IBR is trying very expensive in comparison with refinancing and REPAYE (revised pay as you earn). If we take a look at the full out of pocket value, IBR will value her $82,000 extra vs REPAYE.

Why is REPAYE a lot cheaper?

To begin with, IBR funds are 15% of “discretionary income” and REPAYE is 10%. That implies that Lily’s month-to-month funds on IBR ($402/month) are 50% greater than they’d be on REPAYE ($268/month).

Secondly, REPAYE will give Lily an curiosity subsidy which is able to decelerate her mortgage development in comparison with IBR. Sure, that’s proper, she’d have decrease mortgage funds and her mortgage would develop slower than it might too.

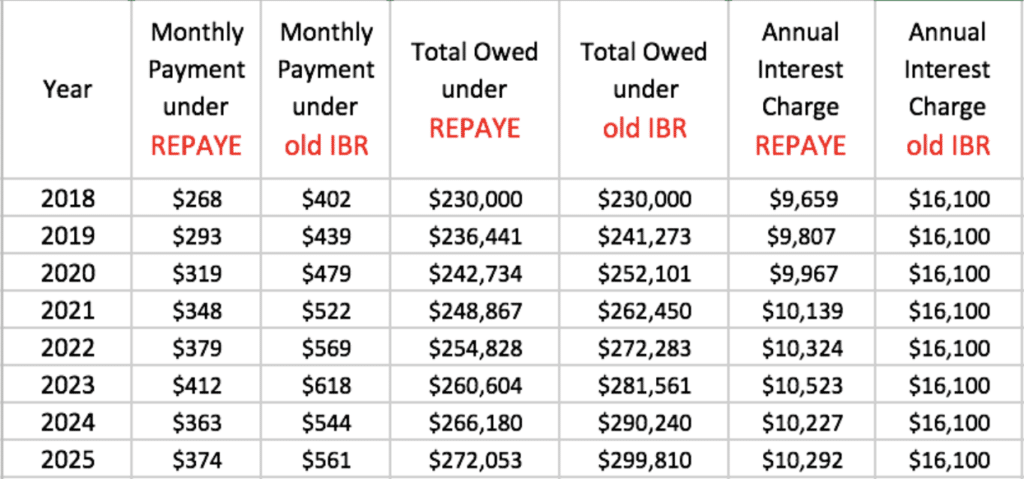

Let’s simply take a look at the following eight years to get the thought:

In case you take a look at the month-to-month cost columns, you’ll see that the IBR funds are 50% greater than REPAYE every year. Paying much less towards her loans would usually imply that her mortgage steadiness would develop quicker than IBR, however for those who take a look at the full owed columns, you’ll see that Lily’s mortgage steadiness is $272,053 on REPAYE after eight years as in comparison with $299,810 on IBR.

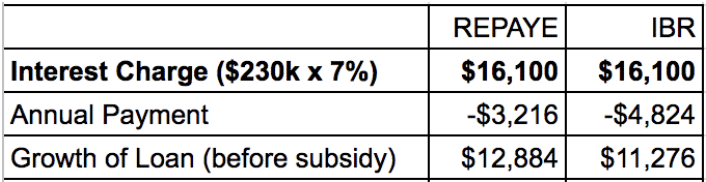

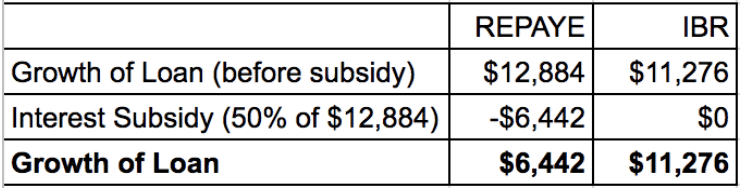

All of it has to do with the curiosity subsidy.

A mortgage will develop if the funds don’t cowl the curiosity cost on the mortgage. In Lily’s scenario, her curiosity cost for the yr can be $16,100 on different income-driven plans ($230,000 x 7% rate of interest).

With REPAYE, you’ll discover that the curiosity cost is about $6,500 much less ($9,659).

Right here’s the way it works:

Her mortgage ought to develop extra on REPAYE in comparison with IBR as a result of she’s paying $1,600 much less over the yr however the curiosity subsidy on REPAYE will lower the expansion of the mortgage in half.

Lily not solely saves $1,600 in mortgage funds for 2018 in comparison with IBR however the federal program kicks in $6,442 to cowl curiosity. That’s saves her $8,042 in 2018 alone.

Acupuncturists can get taxable scholar mortgage forgiveness

After Lily makes 25 whole years of funds on REPAYE or IBR, her mortgage steadiness might be forgiven. The forgiven steadiness might be taken as earnings on her tax return within the yr the loans are forgiven, so she’ll pay earnings taxes on that forgiven steadiness. We name it the tax bomb.

If we assume she’ll be taxed at 40%, then she’s projected to owe about $140,440 when the loans are forgiven.

That quantity is nothing to sneeze at however keep in mind that Lily has 22 extra years (since she’s already three years into this system) to save lots of up that cash. If she units apart $322/month for the following 22 years and earns a mean return of 5%, then she’ll have the cash to pay the taxes.

That’s a reasonably manageable quantity whenever you break it down that manner.

Plus, it suits in effectively together with her price range since she’ll be saving about $140/month in funds on REPAYE and she or he had capability to place an additional $300/month towards her loans. Somewhat than placing it towards her loans at this time, she will be able to save up for the taxes as a substitute.

Lily switches to REPAYE for projected financial savings of $82,000 vs IBR

Lily is projected to save lots of $56,000 in funds over the following 22 years on REPAYE and owe $26,000 much less in taxes when the loans are forgiven for a grand whole projected financial savings of $82,000. That’s virtually actual cash!

All she has to do is let her mortgage servicer know that she’d like to change from IBR to REPAYE. Only a fast name except she desires to do it on-line. She’ll additionally must arrange an account to begin saving for the tax bomb ideally with a low value, respected funding firm that may set her up with an acceptable technique.

If she has a speedy enhance in family earnings on account of her acupuncture clinic rising exponentially or getting married, then she’d need to re-evaluate and see if staying on REPAYE is the way in which to go at that time.

In the long run, the financial savings are simply a part of the profit. Now she has a transparent path to paying again her scholar loans and feels relieved to lastly perceive her path and motion steps.

How acupuncture college students can get probably the most financial savings paying again scholar loans

Acupuncturists can discover a clear path to pay again their scholar loans, even with restricted profession alternatives. A path that might save them tens of hundreds of {dollars} out of pocket and work out find out how to handle their scholar loans to allow them to concentrate on the eagerness that drove them to acupuncture and oriental drugs within the first place.

Pupil Mortgage Planner® has accomplished over 5,785 student loan consults for purchasers advising on over $1.44 billion of scholar loans. We can assist you determine the optimum path and provide the motion steps to get it accomplished in only one hour.

Rob (the creator of this submit) works with debtors who owe between $200,000 to $400,000. He’s often the purpose particular person for our scholar mortgage debt for acupuncturists consults. Be at liberty to electronic mail him at [email protected]

Are scholar loans retaining you from pursuing your profession and monetary targets as an acupuncturist? Share your story within the feedback.

[ad_2]

Source link

{kind=link}